Introduction and executive summary

The Chancellor is conducting the 2021 Spending Review in exceptional conditions. We are dealing with the impact of the COVID-19 pandemic on people, the economy and public finances. But this is also the time to be bold and ambitious about reshaping the direction of this country for years to come.

Councils have played a critical role throughout the last eighteen months, turning rapidly changing policy into practice on the ground. The experience of the pandemic demonstrates that local government is a trusted delivery partner for Whitehall, making sure that our joint response to this crisis recognised local needs and impacts across our diverse communities.

By central and local government working together, tens of thousands of rough sleepers and homeless people were helped off the streets, millions of our most vulnerable were shielded from the virus and over £20 billion in vital grants were provided to businesses forced to close or restrict their activities. Councils, with their directors of public health, have been at the centre of efforts to limit the spread of COVID-19 in all its variants and support our hugely successful vaccination programme. Throughout, councils learnt from and supported each other through sector-led improvement.

Due to rapid change brought in by COVID-19, for many people their local area matters more now than it ever did, and will continue to play a significant role as we move further into recovery. Some groups and communities have been adversely affected by the health, social and economic impacts of the pandemic and will need more help to recover, with some individuals needing support where they did not prior to the pandemic. For others, the issues they faced pre-pandemic – access to fast broadband, housing that is right for them and their families – have been amplified.

This means that the role councils play will have an even greater significance in the lives of people as we all reimagine what our post-pandemic lives look like. We need a collective effort to rebuild our economy, get people back to work, level up inequalities across the country and create new hope in our communities. Responding to the significant economic challenges ahead requires a renewed joint endeavour between local and national government as equal partners. Building back better means building back local.

The Government has set an ambitious target to level up the entire country and improve the lives of its citizens. The Prime Minister was clear that to make progress on levelling up we have to raise living standards, spread opportunity, improve our public services and restore people’s sense of pride in their community. All of these aims need the necessary funding, and councils to be empowered to help deliver on this shared commitment.

It is clear that the starting point for this new approach to our public services, a joint endeavour with national government, needs to be a re-think of public finances with a multi-year financial settlement providing local government with certainty over their medium-term finances; sufficiency of resources to tackle day-to-day pressures and the lasting impact of COVID-19; and that recognises the benefits of investment directed by those closest to the opportunities for shared prosperity.

To achieve this, the Spending Review will need to move away from the traditional drivers of departmental spending towards a degree of fiscal decentralisation in line with some of the world’s most productive economies. The economic challenges our communities are facing requires a bold response – place-based budgets which are in tune with the needs of the local economy. We need to re-think how we fund public services, not try to fit new and bold ideas into old frameworks.

This Spending Review presents an opportunity to reset public spending in a way that is fit for the future, flexible to allow for the delivery of local priorities, and empowers councils to achieve the ambition for our communities that central and local government share.

This submission is organised into six priority themes which set out how local government can act as the driver to our shared priorities, in addition to a series of departmental supplements with further suggestions on how local government can work with all parts of Whitehall to deliver policy.

These proposals include a mix of revenue funding, capital funding, freedoms and flexibilities as well as policy reform to relieve pressures on local government (for example, services to children with special educational needs and responsibilities.

Priority 1 – A strong and certain financial foundation

The Spending Review needs to provide councils with sufficient funding to meet cost pressures and pre-existing challenges, but is also an opportunity to enable councils to bring together the budgets of public services across a place to eliminate duplication of effort and drive savings to the public purse.

Key proposals include:

- A multi-year ‘core’ local government funding settlement which provides sufficient certainty and resources. Excluding the impact of COVID-19 and pre-existing challenges, such as pressures arising from the education of children with special educational needs and disabilities (SEND) or the pre-existing adult social care provider market, we estimate councils are facing cost pressures of £2.6 billion each year, comprising £1.1 billion for adult social care and £1.5 billion for other services, just to keep them at their 2019/20 level of quality and access.

- Our plan to allow councils to deliver further public spending efficiencies by joining up local services in a place and eliminating the fragmentation of funding.

- Our proposals to reform and improve local taxation, as well as using the business rates review as an opportunity to discuss how council funding can be further diversified through other forms of taxation.

Priority 2 – Adult social care and public health

The Government’s publication of ‘Build Back Better: Our plan for health and social care’ (the plan) was an important moment in the long-running debate about the future of adult social care and support. It has the potential to be an important first step in moving toward the changes that are needed to ensure people of all ages are best supported to live the life they want to lead. However, if the plan’s potential is to be realised, the Spending Review must deliver new national funding to stabilise the service. Public health services have shown their value during the pandemic and are key to tackling health inequalities. This is about securing the resources needed to deliver on existing priorities and responsibilities – both now and in the coming years. But it is not an end in itself; such investment will also secure the foundations for other activity we want to take forward now and in the future. These are set out in Priority 3, including our ambitions to narrow inequalities.

Key proposals include:

- A £1.5 billion injection of funding to stabilise the adult social care provider market, together with annual funding needed to meet the cost pressures covered above.

- Investing £900 million in the public health grant to return it to its 2015/16 level in real terms.

Priority 3 – Investing in communities and tackling health inequalities

The concept of levelling up is multi-faceted and will require investment in social as well as physical infrastructure. It is vital that central and local government work together on these multiple issues, in a unique mix in each local area, at the same time.

The Spending Review is an opportunity to put a fresh and innovative approach into action by introducing an unringfenced and ongoing Community Investment Fund, worth £1 billion in 2022/23 and increasing to £3 billion by 2024/25, so that councils can invest in supporting individuals and strengthening communities according to priorities in their local areas, including tackling health inequalities.

Priority 4 – Reaching net zero

Climate change is one of the most important issues facing the world today and councils are leading the way in helping the Government meet its ambition for net zero by 2050.

Key proposals include:

- A call for a new policy and fiscal framework, backed by crucial investment, to allow councils to help Government achieve its aim for the UK to become a net zero carbon economy in 30 years’ time.

- Measures to make sure that the ambitious waste and recycling reforms are introduced in a financially sustainable fashion.

Priority 5 – Education and children’s social care

Councils are ambitious about maximising the life chances of all children, regardless of their background. Equality of opportunity is a critical element of enabling levelling up and building thriving local areas.

Key proposals include:

- Measures to empower councils to build new schools in their areas, as well as the financial capital funding framework needed to support it.

- Dealing with pressures related to the education and care of children with SEND.

Priority 6 – Building back local economies

Councils want to work with Government on the economic recovery from COVID-19 as trusted partners, in particular through greater devolution and powers to steer resources to local economic priorities.

Key proposals include:

- Dedicated local growth funding through the Shared Prosperity Fund and other initiatives.

- An innovative, devolved approach to making sure that local residents have the right skills to match the work opportunities of the future.

- Measures to help councils secure affordable homes for all those who need it, including a housing stimulus package to deliver 100,000 homes each year and reform of the Housing Revenue Account system.

Priority 1 - A strong and certain financial foundation

Cost pressures

Recent Local Government Association (LGA) analysis estimates that the average increase in annual cost pressures facing councils is £2.6 billion per year to maintain services at their current level of access and quality, meaning that the same services will cost around £7.8 billion more to provide in three years’ time. Of this, £1.1 billion per year is related to adult social care (in addition to a pre-existing £1.5 billion provider market pressure), £0.6 billion to children’s social care and £0.9 billion to all other council services (excluding education and police/fire services).

This does not include any continued impact of COVID-19, for example the health impacts of ‘long COVID’, catching up on pent up demand in children’s social care, or the longer-term effects on sales, fees and charges or commercial income.

For all these pressures to be met through council tax alone, income from council tax would have to increase by 8 per cent each year, which is not sustainable. However, if no funding is found, councils would have to make savings worth the entirety of their spending on museums, sports facilities, swimming pools, libraries and parks – each year.

| 2021/22 | 2022/23 | 2023/24 | 2024/25 | Average annual increase | Change 21/22 to 24/25 | |

|---|---|---|---|---|---|---|

| Adult social care | 20.0 | 21.1 | 22.3 | 23.3 | 1.1 | 16.6% |

| Children's social care | 10.9 | 11.4 | 12.1 | 12.6 | 0.6 | 15.9% |

| Homelessness | 0.9 | 1.0 | 1.1 | 1.2 | 0.1 | 27.2% |

| All other services (excl. education, police and fire) | 20.1 | 20.9 | 22.1 | 22.6 | 0.8 | 12.5% |

| Total net expenditure (excl. education, police and fire) | 51.8 | 54.3 | 57.5 | 59.6 | 2.6 | 15.0% |

Other underlying pressures

As in previous years, no improvements to services are included – the £2.6 billion annual average cost pressures are related purely to increased demand and costs of providing the same services, rather than expanding access or increasing the quality of services which would come at additional cost. Underlying problems with services, such as the provider market pressure in adult social care or the remaining SEND service funding deficits held by councils, would stay at the same level as previously, without making it better or worse. Further funding injections would be required to deal with these challenges, or future pressures in these challenges, should they grow.

The following table shows this funding requirement including cost pressures:

| 2022/23 £bn |

2023/24 £bn |

2024/25 £bn |

|

|---|---|---|---|

| Cost pressures (average of £2.6bn per year as above) | 2.5 | 5.7 | 7.8 |

| Existing adult social care provider market pressures | 1.5 | 1.5 | 1.5 |

| Existing pressures on children's social care | 1.0 | 1.0 | 1.0 |

| Existing pressures on homelessness | 0.2 | 0.2 | 0.2 |

| Addressing the public health service underfunding | 0.9 | 0.9 | 0.9 |

| SEND deficits not met by funding | 0.6 | 0.6 | 0.6 |

| Total core revenue funding need | 6.7 | 9.9 | 12.0 |

While the list above covers key identifiable underlying pressures, it is important to note that there are other specific pressures and new burdens, the funding of which falls on core council resources and are more difficult to quantify. They are identified, where relevant, elsewhere in the submission.

Special educational needs and disabilities

The cost pressures set out previously exclude education, and in turn special educational needs and disabilities (SEND), owing to the difficulty in separating local government responsibilities and expenditure from other school and local education authority (LEA) expenditure. However, the ongoing financial impact of SEND must not be understated. The number of children and young people with Education, Health and Care Plans (EHCPs) has risen year on year for the past decade, with an 11 per cent rise in the last year alone. Although the future costs of SEND are difficult to pin down, research from ISOS commissioned by the LGA in 2018 shows that from 2015/16 to 2018/19 expenditure increased by 17 per cent across the 93 authorities which responded to a survey.

Government has provided additional funding for SEND of £250 million over 2018/19 and 2019/20, and £700 million in 2020/21. However, despite this additional funding, there remains an estimated funding gap of £0.6 billion by 2021.

Furthermore, these one-time cash injections, although welcome, have not been formally included in the baseline of the High Needs Block funding provided to councils, meaning that funding continues to further lag behind costs. Whilst annual increases in High Needs Block resources is welcomed, it does not go far enough to keep pace with demand. Moreover, there is uncertainty in the funding councils will receive, despite the trend in EHCP numbers, resulting in difficulty managing future risks from an already squeezed system.

COVID-19

Local government has coordinated and delivered the national government’s response to the COVID-19 pandemic at a local level. Working with national government, councils have drawn on strong local leadership coupled with exceptional commitment from councillors and council staff to protect the most vulnerable in our society and ensure vital services continue to be provided, showing what can be achieved when we work together towards a shared goal.

Central and local government have protected rough sleepers and homeless people, helped those defined as clinically extremely vulnerable (CEV) to shield to protect themselves from the virus, set up effective local virus tracing partnerships, supported businesses with vital grants, and helped distribute the largest vaccination programme in our history. Local government can be, and has been, trusted to deliver on national priorities.

For many people their local area matters now more than ever, with an emphasis on the value of green spaces, safe communities, and efficiently run public services. For some, the issues they faced pre-pandemic – access to fast broadband, appropriate housing – have been amplified. The role councils play will have a greater significance in the lives of people as we emerge into the post-pandemic era.

The pandemic has caused extraordinary financial costs to local government. Councils reported to Government, the financial impact of COVID-19 in 2020/21 was an estimated £9.5 billion (consisting of £6.8 billion of cost pressures and £2.7 billion of non-tax income losses). In addition, councils estimate £2.2 billion of lost local tax income. Central government has supported councils financially, with £8.5 billion of grants as well as compensation schemes for a proportion of lost sales, fees, and charges, and local tax income.

The effects of COVID-19 will be felt far beyond the end of the current phase of the pandemic.

- Economic vulnerability and the long-term health effects some people experience from COVID-19 will continue to hinder society’s full recovery.

- Council delivered adult social care and mental health services will play a pivotal role in supporting people.

- Children and young people have missed out on education, developmental milestones, and important life-events.

- The pandemic has exacerbated existing inequalities, leading to higher rates of coronavirus infections and death amongst the most disadvantaged people.

Councils are best placed to identify people in their local areas who need the most support, and what support is required. This will require substantial backing from Government to bolster the recovery from the pandemic and ensure people are supported in the long term.

Councils continue to be financially hit by the crisis, with costs and losses of income likely to continue. It is difficult to predict the uncertain nature of how the pandemic, and its legacy, will impact local government. We welcome the funding Government has provided to date and call on Government to continue to monitor the situation both in the short and long term, providing vital support when needed. If the Coronavirus mutates again, and we are faced with a virus that escapes our current vaccine programme, it will be extremely important to be able to stand up all of the response infrastructure we have built, allowing councils to step in as they have done to protect our vulnerable communities, contain the virus, and keep our local economies going.

Efficiency

It is important to recognise that one of the goals of the Spending Review will be to set a new path towards sustainability of the public finances after the impact of COVID-19. This requires looking at how the public sector spends money, and on what priorities.

Councils have delivered more than their fair share of the burden of putting public finances on a more sustainable footing over the past decade and stand ready to help Government with the task ahead.

- Prior to the pandemic, councils had already dealt with a £15 billion real terms reduction to core government funding between 2010 and 2020. They responded to this by being more efficient, streamlining services and finding new and innovative ways of operating while still delivering the vital services their residents rely on and value.

- By way of example, there are now 626 shared services arrangements, with councils sharing the cost of a number of different services. These changes have achieved £1.3 billion of cumulative efficiency savings – money which is being used to protect the delivery of valued public services to local communities. Council planning departments have cut spending by 46 per cent in real terms. Despite this, councils have improved efficiency in making planning decisions, increasing the rate of decisions on planning applications received by 2 per cent since 2015/16.

- The traditional means of delivering efficiencies within local government have been exhausted. LGA work undertaken prior to the pandemic showed that the vast majority of remaining variation in spending between councils on older people’s adult social care and children’s services – the two biggest service areas – was explained by factors outside the control of councils (78 per cent and 71 per cent respectively).

- Despite the sustained pressure on council finances and the fact that local government is close to exhausting all efficiencies, residents’ trust in local government decision making remains high – nearly three quarters of residents trust their local council most to make decisions about how services are provided in their local area, compared to only 17 per cent who trust central government more.

Building back whilst stabilising public finances needs a completely different approach which unlocks the capabilities of local government to deliver savings across the public sector, instead of looking at local government budgets as just another budget line.

Councils are ready to help the Government deliver further significant efficiencies to the public purse through the following measures:

- A renewed focus on prevention, backed by government investment. A sure-fire way to address existing and future demand for services such as social care, homelessness support and community safety is to invest in lower cost approaches which help strengthen people, communities and local infrastructure. However, with council budgets stretched, a challenge of this scale needs to be kickstarted with government investment. Our submission provides a rich set of such investment opportunities.

- Reducing the fragmentation of government funding. Research commissioned for the LGA found that in 2017/18, nearly 250 different grants were provided to local government. Half of these grants were worth £10 million or less nationally. At the same time, these grants are highly specific – 82 per cent of the grants are intended for a specific service area. Around a third of the grants are awarded on a competitive basis and there is a cost to every application councils make, whether or not successful. All of these factors mean that if fragmentation and the ringfencing of grants is reduced, the system of local government funding can provide much better value for the same amount of funding.

- Bringing budgets together in a place. The approach to tackling fragmented funding can go much further, by looking beyond just local government funding. We need to allocate money to places and not departmental silos. A shared financial and governance framework will mean that services can better align with local priorities and local duplication of efforts can be eliminated. This Spending Review should place emphasis on communities and place by introducing multi-department place-based budgets, explicitly built around the needs of diverse local communities using equality impact assessments.

- Supporting councils to make local self-financed investments to help transform services leading to savings or generated income. This is covered immediately below.

Certainty

In addition to sufficiency in funding levels, certainty to enable councils to plan appropriately is just as important.

Councils have received one-year funding envelopes for three years in a row now and this is an obstacle to councils to making innovative and meaningful decisions over financial planning, so hampering their financial sustainability. Councils may end up planning on the assumption that they will have less funding available to them than is actually the case, needlessly scaling back non-statutory services and making redundancies.

Government must commit to councils receiving a three-year Spending Review settlement, including as much information as possible, such as council tax referendum limits (if any). The NHS, defence and schools have been benefitting from longer term certainty and the same should apply to council services which are vital to the national recovery, even if all other departments receive a one-year Spending Review outcome.

An early, three-year local government finance settlement should translate the Spending Review outcome into individual council settlements. In recent years, local government finance settlements have been published in draft form very late in December, after the Department for Levelling Up, Housing and Communities’ stated target of 5 December. This target should be met.

The lack of certainty has been further exacerbated by the number of financial reforms which have been paused. Lack of information about whether and when these reforms will resume would mean that even if there was certainty over the overall total council funding sums for a number of years, this would not give individual councils the certainty they need for financial planning.

In this light, it would be extremely helpful to local government to receive confirmation of whether and when each of the planned local government finance reforms will be implemented as soon as possible. This includes the review of relative needs and resources (also called the Fair Funding Review), the business rates reset and the parameters of the new homes bonus.

Providing certainty on these issues would make a significant difference to council financial planning, and therefore public services, even without a Spending Review outcome. Councils could make decisions which provide better value for money for the taxpayer, by making longer term investments that deliver savings, if they had longer term certainty over funding. Of course, if or when financial reforms do go ahead, overall funding will need to be sufficient to facilitate them and to ensure no council sees its funding reduce.

Local taxation

Reforming council tax

Council tax increases, including the adult social care precept, are not a long-term solution to funding services. Increasing council tax raises different amounts of money in different parts of the country. On its own, council tax falls short of the sustainable long-term funding that is needed to improve the services our communities and local economies will need to recover from the pandemic. However, that does not mean that council tax cannot be improved even without fundamental reform. We would like to work with Government to make council tax more local:

- To strengthen the accountability of councils to their residents through the local election process, the council tax referendum limit should be abolished so councils and their communities can decide what increase in council tax is warranted to protect or improve local services. Ending referendum principles would also improve value for money – a referendum costing potentially up to £1 million would have to be organised to approve a council tax bill increase of as little as £1.15 per week. Failing that, the Government should consider ways to define the referendum limit which do not reward or penalise councils based on their past decisions. For example, the percentage-based limit could be replaced by a threshold which allows higher percentage increases to areas with lower council tax levels, similar to the £5 flexibility provided to shire district councils. In addition, the council tax levy paid to drainage boards should not be counted towards the cap on council tax rises. Any additional costs should not fall on council taxpayers.

- To make sure the tax system is fair to everyone according to local circumstances, councils should have the powers to vary all council tax discounts and eligibility criteria. Most discounts and exemptions are fixed nationally. A prime example is the single person discount, worth 25 per cent of the total bill and applied to all households where there is only one liable occupant, regardless of their ability to pay. This discount is currently worth £3 billion each year, covering around a third of all dwellings.

- To improve the build-out rates of homes with planning permission and reduce the number of stalled sites, councils should be able to charge developers or landowners full Band D council tax for every unbuilt development in these situations, as opposed to having to wait for the Valuation Office Agency (VOA) to list developments following their completion. LGA analysis suggests that over one million homes granted planning permission since 2010 have not yet been built. This is equivalent to three years’ worth of Government’s target number of homes to be delivered each year.

- As COVID-19 support measures, like the furlough scheme, end from September 2021 the local Council Tax Support (CTS) Covid Grant should be continued for the three years of the 2021 Spending Review, linked to changes in the number of predicted working age claimants, so councils can continue to help the most vulnerable council taxpayers.

- We would like to work with the Government to improve the generational fairness of local CTS by revisiting the pensioner element of local CTS to give councils more flexibility. However, this should not be accompanied by further reductions in government funding for CTS to avoid the experience of the 2010s.

Reforming business rates

As part of the Government’s Business Rates Review, the Government has acknowledged that business rates are an important source of revenue for local government and stated that the impact on the local government funding system will be an important consideration in reviewing the tax.

Property continues to provide a good basis for a local tax on business. Business rates are efficient to collect and have been relatively predictable and buoyant in recent years. However, the changing nature of business alongside the nature of demand pressures on councils means that we cannot look to business rates to form such a substantial part of local government funding in the future and alternative means of funding councils will be needed instead of, or as well as, a reformed business rates system.

Our proposals for reforming business rates include the following:

- If local authorities had more leeway on business rates relief, they would be able to help local and independent businesses in order to stimulate the local economy. This could be done by making large national reliefs, such as charitable and empty property relief, discretionary. It would also allow councils to incentivise other behaviours that match local and national economic priorities, for example providing reliefs for new or green investments.

- Many fundamental concepts have been set by case law and not by statute, leading to results which may seem puzzling to the public, such as the fact that large vacant sites may not pay business rates. Changes in the basis of liability are needed so that more is defined in statute.

- The complex framework of business rates exemptions needs to be reviewed. This includes, for example, agricultural exemptions where there are businesses which should normally be rated but just happen to be located on farms.

- Aggressive business rates avoidance continues to cost councils and central government more than £250 million each year. We call for the Government to tighten up on the abuse of reliefs along the same lines as have been introduced in Wales and Scotland.

- We will be replying to the consultation on more frequent revaluations which proposes a compliance regime for ratepayers at the same time as the move to three yearly revaluations. We consider that a similar compliance regime should apply to ratepayers in their dealings with local authorities.

- Local government should be able to set its own business rates multiplier, or at the very least be able to set a multiplier above and below the nationally set multiplier. Local authorities ought to have the power to vary multipliers by property value or property type. This would enable them, for example, to charge a higher multiplier to businesses, such as online warehouses, in order to support reliefs for other businesses.

Alternative and new sources of funding

The Government’s fundamental business rates review, which considers both reforms and alternatives to the tax, is an important opportunity to take a fresh look at the local government finance system as it is being stress-tested by the impact of the pandemic.

For example:

- The recent announcement of a health and social care levy follows our long-standing calls on the Government to make the case for national taxation increases, or new levies, to fund adult social care pressures. The announcements are covered in more detail in the next chapter.

- Taxation should be fair for both physical and online businesses. We welcome the fact that the Government is consulting on proposals for an online levy as part of the review, however the proceeds of such a levy should be retained by local government to diversify the local taxbase. We look forward to action on this when the review reports.

Overall, local government needs a funding system that raises sufficient resources for local priorities in a way that is fair for residents and gives local politicians the tools they need to be the leaders of their communities. It is therefore important that the tax system provides as much certainty as possible.

In the meantime, we are calling on the Government to publish a progress update on the review as part of Spending Review announcements.

Capital investment framework

Investing in infrastructure with capital spending will be crucial to delivering the social and economic recovery from the pandemic, delivering key government priorities on net zero, housing and regeneration, and making the public sector more efficient and able to deliver better value for money while providing key services for citizens.

Councils are best placed to deliver capital infrastructure to enable economic regeneration, housing and school improvements, service transformation and to support Government’s move towards net zero carbon emissions, if they are given the right financial freedoms, flexibilities and support.

The Government has recently published its ‘planned improvements’ for the local authority capital framework. We welcome the undertaking that any significant changes to the capital regime will be subject to individual consultations, and as yet the full detail of what the changes are and what they will mean is not yet clear. However, we will continue to make the case that any changes need to be proportionate and that the overall framework for capital finance should continue to allow local authorities wide freedoms to borrow and invest, without the need to seek prior approval from government, if councils are to be able to play their key role in delivering capital infrastructure.

Our submission contains many examples of where councils can play a key role in delivering priorities, such as fixing the nation’s roads and delivering economic regeneration, delivering high speed broadband and high-quality mobile connectivity everywhere, investment in housing (coupled with reform of Right to Buy), schools, transport infrastructure, as well as tackling environmental challenges including reforms to waste and recycling and carbon reduction.

Government grant funding of council capital programmes has reduced in recent years. Capital funding in 2019/20, the last year for which outturn figures were published, was £300 million lower than in 2014/15. If 2014/15 levels of grant had been maintained in the intervening years councils would have had an additional £2.3 billion to invest in local capital projects between 2014/15 and 2019/20. Such funding could help shore up local infrastructure – for example it could reduce the highways repairs backlog by a fifth, be used for local housing and regeneration, or put towards the provision of additional school places.

Where government capital grant funding is available, it is frequently fragmented and accompanied by bureaucratic and burdensome bidding processes. For example, there are at least 11 different capital funding streams for roads investment alone, each with their own arrangements, rules and allocation processes. Councils have frequently had to consider the risk of investing significant time and revenue resources that cannot be spared into long-winded processes that are not guaranteed to deliver any local benefits.

A further funding freedom can be delivered very simply, and at no cost, by making the flexible use of capital receipts arrangements permanent and available to fund all transformational and savings projects. Government first introduced this flexibility in 2015 and although extension of the scheme beyond 2022 was announced in the 2021 Budget, details of how the scheme will operate have not yet been confirmed. The Spending Review is the opportunity to make this permanent, adding certainty and removing the need for further review.

Priority 2 - Adult social care and public health

The 2021 Spending Review is an opportunity for the Government to lay down a clear statement of intent for moving towards a future model of care and support where people of all ages who need to draw on social care are treated equally, valued for their contribution, respected for their knowledge of what works best for them and supported to live the life they want to lead in the communities they know and love.

The recently published ‘Build Back Better: Our plan for health and social care’ (the plan) helpfully recognises that ‘social care is an integral part of our society and economy’. However, its proposals focus predominantly on the issue of protecting people from potential catastrophic care costs and selling their home to pay for care, with the bulk of the new levy’s allocation for social care likely to be spent on paying for associated charging reforms. The plan does not set out any detail on the level of funding needed overall. This is an important dimension of the reform debate, but it does not address immediate pressures, nor deliver any extra, better or different social care for people of all ages who have cause to draw on it. This is where the Spending Review must act. If it does not, the reforms set out in the Government’s plan run the risk of making the pressures facing adult social care considerably worse.

It is also an opportunity to properly recognise and reward the estimated 1.52 million people working in adult social care, whose dedication, commitment and personal sacrifice have been indelibly marked on our national conscience over the last 18 months. The plan potentially lays the groundwork for helpful measures to support the care workforce through earmarked funding of £500 million. However, it does not address the issue of care worker pay, which is so crucial for helping to tackle recruitment and retention problems in the care workforce

The Spending Review is an opportunity to solidify the foundations of the Government’s social care reform agenda and, in so doing, pave the way for redesigning the function, form and funding of social care. If done well, this could create one of the most powerful, positive and lasting legacies of the COVID-19 pandemic for people of all ages.

Adult social care – where we’ve come from

Adult social care is the largest directly controlled local government service by spending – making up more than a third of controllable spending – and continues to grow. The sustainability of all local government services, including many that support ‘wellbeing’ in its widest sense, therefore depends on securing a sustainable settlement for adult social care.

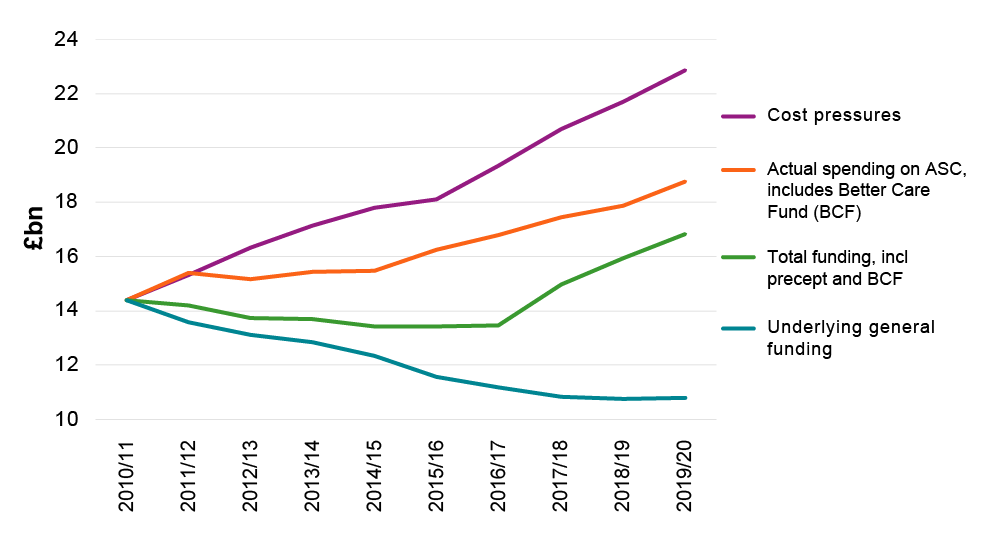

- Over the previous decade, adult social care costs rose by £8.5 billion to take account of rising demand and prices, while total funding, including the Better Care Fund (BCF) only grew by £2.4 billion. This left councils with a funding gap of £6.1 billion.

- Of this, £4.1 billion was met by making savings to adult social care services, whilst a further £2 billion was diverted from other council services, cutting them faster than otherwise would have been the case.

Chart 1: Adult social care costs and funding 2010/11 to 2019/20

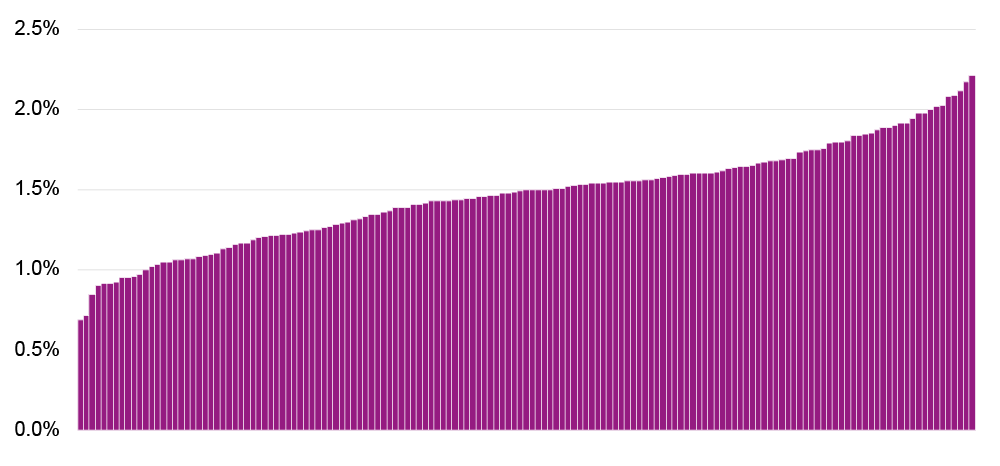

Even before the pandemic struck, adult social care was under significant pressure following years of inadequate funding and piecemeal, sticking plaster solutions. The reliance on the council tax social care precept has been a poor tax base to fund national entitlements under the 2014 Care Act. It is highly visible locally, but it has no relationship to need and the money raised has been insufficient to cover increasing costs. On average, a 1 per cent precept has added 1.45 per cent to net adult social care spending, but with a range of between 0.68 per cent and 2.21 per cent. This is why we were particularly disappointed that Government’s recent announcements provided no new immediate funding for social care and that its approach to tackling social care’s core pressures is through the continued use of council tax, the social care precept and long-term efficiencies. The Government must move away from this approach and inject genuinely new funding to tackle immediate pressures.

Chart 2: Percentage increase in adult social care budgets resulting from a 1 per cent increase in council tax across all authorities

Core cost pressures in adult social care

We stand ready to work with the Government, as part of the 2021 Spending Review and beyond, to make adult social care more resilient and financially sustainable. Only bold and ambitious measures can help deliver better outcomes and better-quality services for people of all ages who have cause to draw on social care and support to live their best life. We are deeply ambitious for the future of care and support and believe the Spending Review has a crucial role to play in stabilising the short-term and laying the ground for the ambitions set out in the Government’s plan and what will be set out in its forthcoming white paper on the future of care and support.

The issues currently facing adult social care are not new, but many have been exacerbated by the experience and consequences of the pandemic. They all have the potential to have a detrimental impact on people’s wellbeing and quality of life.

As a first step, we therefore need to urgently address immediate funding challenges to prevent further deterioration in the access to and quality of care. It was deeply disappointing that the Government’s plan provided nothing for social care in the short-term; the Spending Review must rectify this as a priority.

Analysis by the Institute for Fiscal Studies from September 2020 suggests an immediate injection of funding of at least £1.5 billion is needed to enable councils to provide short term stability and avoid serious risks to the adult social care provider sector as we continue to move beyond the pandemic.

For future years, the baseline for social care going forward must include the irreducible, demographic and other costs which councils have to accommodate in order to avoid building up further pressures in the future, currently estimated at an additional £1.1 billion per year as set out above.

These estimates exclude any continued impact of COVID-19 on adult social care providers. This burden has to be monitored alongside wider COVID-19 funding issues and dealt with separately through continued bespoke council COVID funding arrangements. This includes the difficult issue of mandating vaccination of the workforce in care homes and the potential negative consequences of this policy. For example, the Department of Health and Social Care’s best estimate of the impact of the policy (just for care workers working in Care Quality Commision-registered care homes) is that 40,000 workers (7 per cent of 570,000 such employees) may choose not to take up the vaccine before the end of the grace period in November. This has the potential to significantly exacerbate existing pressures on care homes, with consequences for care quality.

These pressures have created the significant challenges set out below, many of which have been exacerbated by the pandemic. The Government’s plan for social care may help address some of these but not in the short-term, with funding from the new levy not expected to reach social care until later in the three-year period. It is essential that the Spending Review fills this gap – without such action, the pre-existing challenges will worsen.

- Unpaid carers

An estimated 4.5 million additional people have become unpaid carers because of the pandemic. This is on top of the 9.1 million unpaid carers already caring before COVID-19.

Carers, who are mostly women (57 per cent), are more likely to suffer depression, anxiety and stress and nearly two-thirds of carers have a long-standing health condition.

Unpaid carers have been more affected by the pandemic compared to the general public on aspects of life including work, loneliness, household finances and access to groceries, medication and essentials.

Young carers have significantly lower levels of attainment at GCSE level and are more likely to not be in education, employment or training.

-

Providers

77 per cent of adult social care directors are concerned about the financial sustainability of some of their residential and nursing providers.

82 per cent are concerned about domiciliary and community care providers.

43 per cent of councils report that providers had closed, ceased trading or handed back council contracts in the last six months.

Care home occupancy levels are down compared to last year, threatening care home viability, particularly smaller independent care homes who lack the scale of larger operators to deal with occupancy reductions. -

Unmet need

Councils received 1.9 million requests for support from new clients in 2019/20, similar to the 1.91 million requests in 2018/19 and up from 1.84 million requests in 2017/18.

Just under 160,000 people are waiting for care reviews.

The LGA has previously estimated that £6 billion would be required to address unmet need across both older and working age adult social care cohorts. -

Prevention

73 per cent of directors consider investment in prevention as the second most important way to deliver savings (after developing asset-based and self-help approaches to reduce numbers of people receiving long-term care); 50 per cent of directors state they are less than confident about meeting their statutory prevention duties in 2021/22. -

Quality

Pockets of poor quality persist, with 3 per cent of care homes and 3 per cent of community social care services having never been rated better than ‘requires improvement’. -

Supporting the NHS

Sustainable funding of adult social care is crucial to the successful delivery of the Government’s objectives for integrated care systems (ICSs), the wider aims of its Health and Social Care Bill, and helping to clear the significant NHS backlog of elective care.

Long-term sustainability and reform

We recognise that protecting people from ‘catastrophic care costs’ and having to sell their home to pay for care is a Government commitment. The measures outlined in the Government’s recent plan are a potentially important first step in changing the way social care is paid for and funded, which we acknowledge is an important dimension of the reform debate. It is also helpful that the Government has looked beyond just this issue, outlining action on, for example, the workforce and supported housing. The Government’s commitment to publishing a new adult social care white paper by the end of the year is also welcome. However, while these are all potentially positive developments, we have serious concerns and question whether they make the kind of progress needed to help adult social care deliver for people. The following are our principal concerns, which are covered in more detail in our dedicated briefing on the Government’s plan:

The levy

- There is no additional funding for frontline social care from the estimated £36 billion to be raised by the new levy over the next three years. However, addressing the NHS backlog and freeing up hospital beds cannot be done without also fixing social care. The government needs to commit to a greater share of the Levy to go to frontline social care from the outset.

- Urgent clarity is needed on both the profile of the £5.4 billion allocated to adult social care reform over the coming three years, as well as what adult social care can expect to receive after this period and in subsequent years.

- Urgent clarity is also needed on the breakdown of the £5.4 billion given there are several significant commitments attached to it. Currently, the only known allocation is £500 million for measures to support the care workforce. We can neither confidently understand nor judge the sufficiency of the remaining £4.9 billion without knowing what level of funding each of the commitments will receive.

- Even without a sense of funding allocations, we are not convinced that the proposal to move to a fair rate of care (itself undetermined) will remedy the situation where self-funders pay significantly more for equivalent care than people funded at the council rate. We are even less convinced that the proposal will give providers sufficient funding to improve care quality or care worker pay.

- It is helpful that the plan makes clear that public sector employers will be compensated for their increases in higher National Insurance contributions so as to avoid a reduction in spending power. However, just in the realm of adult social care, councils routinely commission from a range of partners from the private, independent and voluntary sectors, all of whom will likely want, or expect, to see an increase in their fees to reflect their higher NI contributions. The plan says nothing about these relationships and potential associated costs, nor the Government’s expectations of councils on this issue. Our very initial analysis suggests that if councils were to cover this additional pressure, it would cost in the region of £100 million per year. This is just for adult social care; the cost pressures arising from commissioned activity across all council services would clearly be considerably higher. We need urgent clarity from Government on this important issue.

The adult social care workforce

Over the last 18 months, the adult social care workforce has demonstrated to the nation its enormous capacity for resilience, compassion and dedication. Front line care workers have helped keep our loved ones safe and done all they can to support their wellbeing in the most challenging of circumstances. Proper action on the care workforce must be a lasting legacy of the pandemic, starting with the Spending Review.

Adult social care is also a significant sector of the economy, worth more than £20 billion per year. This does not include the additional value that care and support generates from supporting people who receive services to be in work who would otherwise not be able to.

However,

- there is an estimated turnover rate in social care of 30.4 per cent (equivalent to approximately 430,000 leavers over the year) alongside a vacancy rate of 7.3 per cent (equivalent to approximately 112,000 vacancies at any one time)

- if the workforce grows proportionally to the number of people aged 75 and over in the population, then a 50 per cent increase (800,000 new jobs) will be required by 2035.

We need to have a sustainable social care workforce that is fit for the future, given the increasing demand for support as the population grows and ages, and as care moves closer to home, becomes more integrated, and new models emerge.

The Government’s announcement of a £500 million investment in measures to support the care workforce is clearly welcome. But if we are to meet this challenge and unlock opportunity, we need a coordinated commitment to the workforce, delivered through a workforce strategy or people plan, including action on pay. Alongside other national organisations, our vision for a future workforce strategy and its outcomes is:

- staff being recognised, valued and rewarded

- investment in training, qualifications and support

- clear career pathways and development opportunities

- the building and enhancement of social justice, equality, diversity and inclusion in the workforce

- effective workforce planning

- expansion of the workforce in roles which enable prevention and support the growth of innovative models of support.

The social care workforce must be developed in a manner equivalent to the NHS as part of a stable, sustainable solution to long-term funding problems and that this must involve ‘parity of esteem’ for social care staff with their NHS colleagues.

Any changes to pay and reward must be fully funded by central Government as there is no resource in the sector to meet the demands of this challenge. It will be important to assess the best form of comparison with the NHS on basic pay and resulting costs as overall costs could be in the region of £1 billion.

The Resolution Foundation have calculated that if a living wage for care workers was publicly funded, just under half (47 per cent) of public costs would be returned to the Exchequer through higher personal tax receipts and lower benefit payments.

Research and deliberation will be needed on coordination of other terms and conditions and the introduction of an effective mechanism for implementation and uprating. To achieve those aims with a reasonable degree of consensus across the sector, we continue to urge Government to commission an independent review to promptly review the existing pay levels in the sector and the mechanism for ensuring they support the recruitment and retention of the high-quality workforce the public requires.

Public health

Throughout the pandemic, public health services commissioned by local councils have worked quickly, efficiently, and creatively. Public health has used its experience in communications, behavioural insight and health campaigns to engage with local people to tackle outbreaks and maintain safety. Councils have been flexible and innovative in keeping health and wellbeing services running through the use of digital technology and have sought to tackle the impact of the pandemic on health inequalities.

Health is an essential part of the economic recovery and vice versa. Our report ‘Nobody left behind: Maximising the health benefits of an inclusive local economy’ makes clear the link between health and the local economy. For example, public health can play an important role in collating and interpreting relevant population-level data and supporting place-based partnerships in understanding and acting on the health impact of economic strategies. To make the most of this interrelationship between public health and the economy, councils need the resources to work in partnership with their voluntary and community sector (VCS) to provide low-level support to improve health, wellbeing, participation and resilience.

In addition to the potential of public health services to address health inequalities and support the economic recovery, there is a strong benefit for public finances as well. Money invested by Government in public health is helping to relieve pressure on other services like the NHS and the criminal justice system. Analysis shows that local authority public health funding is three to four times more cost-effective in improving health outcomes than money spent in the NHS.

The new Office for Health Improvement and Disparities (OHID) has an opportunity to enhance the focus on prevention. All parts of the public health system – including councils’ public health services – have a role to play in promoting healthier choices, preventing sickness and intervening early, to reduce the need for costly hospital treatment and social care. By embedding prevention as a core focus of its strategy, OHID will ensure the best outcomes are achieved for people.

Sustainable core funding

We know that one thing that marked England out as COVID-19 hit was our poor public health including our high rates of inequalities, of smoking, and of overweight people and obesity. The pandemic has demonstrated that prevention must not be sidelined. We need to tackle the 40 per cent of avoidable deaths which result from tobacco, obesity, inactivity and alcohol harm. Increases in the value and longevity of the public health grant are vital to improve these challenges.

The pressure on the public health workforce during the pandemic response has been unprecedented and has highlighted the need for investment in public health capacity at all levels. Government should develop a programme for ensuring sufficient public health professionals are trained and councils sufficiently funded to employ the necessary skilled workforce.

It was welcome to see the new Secretary of State for Health and Social care recognise the importance of tackling health inequalities which are preventing us from levelling up the country. Public health services are vital in achieving this aim – with greater, more consistent funding, alongside other local government services such as housing, sport and leisure provision and employment, councils can influence the future health and life chances of our communities.

Public health grant allocations have fallen in real terms from £4.2 billion in 2015/16 to £3.3 billion in 2021/22. On a per head basis that equates to a 24 per cent cut since initial allocations were made in 2015/16. (Health Foundation analysis). At a minimum, government should restore the grant to 2015/16 levels by investing an extra £900 million a year and then ensure that the grant keeps pace with growth in NHS England’s spend.

Rewiring behavioural incentives and raising revenue

Levies on alcohol, smoking and sugary products can discourage consumption of harmful products. The proceeds could help fund public health services in councils, so supporting the proposals above.

For example, the Government has announced its ambition for England to be smoke-free by 2030 and said it would consider proposals for revenue raising to pay for this through a ‘polluter pays’ approach. The LGA supports this proposal to raise income.

The ‘polluter pays’ levy would provide, at no cost to the public purse, the funding needed to eradicate the social and geographical inequalities in smoking and deliver a Smokefree 2030. The Smokefree 2030 Fund is also essential if the government is to achieve the ageing society mission to extend healthy life expectancy by five years by 2035.

The UK Soft Drinks Industry Levy was one of the first taxes explicitly designed to incentivise manufacturers of sugar sweetened beverages to reduce sugar content. Since its introduction in 2018, the levy has generated over £720 million for the Treasury.

In the three years since the soft drinks industry levy was introduced, manufacturers have cut the amount of sugar in their products while hundreds of millions of pounds have been raised in revenue. It is vital that future funds raised so far are invested in the best possible way to ensure that our children get the greatest start in life. In order to truly tackle our child obesity epidemic, the Smokefree 2030 fund and Soft Drinks Industry Levy revenue need to be devolved so that council public health teams can direct how this money is used, intervene earlier and do more to ensure that our children stay healthy, active and develop good eating habits, which they can continue into adulthood.

Best start in life

Early years support forms the basis for future healthy lives, but important services with proven effectiveness, such as support for the first years in life, have seen their funding reduce. Redeploying updated models of support, with enhanced digital offers and a focus on community assets, peer support and positive mental health in families, should be a priority.

The Leadsom Review into improving outcomes in the first 1001 days is an excellent opportunity to build on the support already offered by councils to ensure we are addressing health inequalities from the outset. Councils are keen to expand and improve their ‘Start for Life’ offer, as put forward by the review team, however many will struggle to increase and maintain support for new parents and infants without additional funding.

Whilst we agree that the First 1001 Days (zero to two) is a critical period in healthy child development, we will not break generational disadvantage and tackle health inequalities without taking a life-course and family-based approach to improving outcomes for disadvantaged children.

We would like to work with the Government on a children’s workforce strategy to support the development of a well-qualified, well-resourced workforce with the appropriate knowledge, skills and experience to work in a preventative way. This needs to be an integrated strategy between local authorities, health, education and community and voluntary sector partners, which links effectively with established programmes, such as Troubled Families, Sure Start and Family Hubs and puts the child’s journey at the centre. The workforce plan must be fully resourced.

Priority 3 - Investing communities and tackling health inequalities

As the Prime Minister and the new Secretary of State for Health and Social Care have recently highlighted, there are serious inequalities when it comes to health and life chances across England which affect, among other things, the economy in a reciprocal relationship. Local government is a key delivery partner in addressing these inequalities and enabling levelling up across the country. We have heard from different areas about the unique challenges they face. It is clear that the concept of levelling up is multi-faceted and will require investment in social as well as physical infrastructure and it is vital for central and local government to work together on these multiple issues, in a unique mix in each local area, at the same time.

As we have argued above, trying to manage multiple priorities at the same time has in the past led to a sprawling number of central government funding streams, all with their unique conditions, reporting requirements and distribution methods. This poses a serious risk of duplication and failure to achieve value for money, but also requires significant resource from an already depleted workforce. Indeed, addressing the multitude of priorities and issues we cover throughout this submission individually would contribute to fragmentation of funding even further.

We recognise that, in the current public finance context and with the need to achieve long term sustainability in our public spending commitments, it is unlikely that government will be able to fund all the preventative and early intervention proposals that we have put forward in the past as set out in table 3. However, we will not be able to level up communities if we do not make a start.

| Proposal | Sum, annual |

|---|---|

| Investing in adult social care prevention, innovation and equality of outcomes | £1 billion |

| A public health prevention transformation fund | £2 billion |

| Investing in early intervention in children's services | £1.7 billion |

| Total | £4.7 billion |

Our solution, therefore, is to start smaller and build community infrastructure over time in a way that allows local areas to target funding to their greatest local priorities.

The Spending Review is an opportunity to put a fresh and innovative approach into action by introducing an unringfenced and ongoing Community Investment Fund, worth £1 billion in 2022/23 and increasing to £3 billion by 2024/25, so that councils can invest in supporting individuals and strengthening communities according to priorities in their local areas.

This unringfenced fund could have a requirement that councils are clear with residents which schemes and initiatives are financed by the fund, similarly to how the source of funding for infrastructure spending has been advertised in the past. It is likely that much of the funding would be directed through the voluntary and community sector, though councils might directly deliver or look to local businesses to address some requirements. This could also build in local social value benefits.

Councils would be empowered to use this funding to start building back resilient communities and tackling health and social inequalities, for example by investing in the following areas:

Adult social care prevention and innovation

New and dedicated funding for each year of the Spending Review period could enable increased spend on prevention and innovation to help prevent or reduce the need for longer-term support. Local priorities might include:

- Enabling increased investment in preventative services including those provided by the voluntary sector to support people in their own homes and keep them engaged in their communities to avoid escalating need and more formal health and social care interventions. This would include supporting informal carers.

- Funding support for action on adult social care inequalities. The disproportionate impact of COVID-19 on some communities has exposed long endured patterns of inequality and discrimination. The proposed funding would allow councils to begin targeting specific action to address inequalities and poor outcomes for those people at greater risk.

- Investing in innovation and technologies to enhance outcomes. This could include assistive technology, predictive analytics and apps. This would also support bringing evidence-based but currently marginalised positive models of care and support into more mainstream use and could also be used to develop and rapidly test solutions to particularly challenging care problems.

As set out in the NHS plan and aspired to in the Care Act, a preventative model, rooted in local communities, would be better for people, reduce rising demand for social care over time and better for the NHS by preventing or delaying an individual’s attendance at hospital – making a saving to the public purse.

Public health

Public health services are vital to tackling the health inequalities which are preventing us from levelling up the country. With greater, more consistent funding for councils’ public health services, alongside other local government services such as housing, sport and leisure provision and employment, councils can influence the future health management and life chances of our communities.

Councils would have the option to use the Community Investment Fund to supplement spending from the public health grant so that they can offer a wider public health programme targeting particular local challenges. Our previous work shows that scaling up good practice examples from across England could be highly cost-effective, delivering a return of 90 per cent to the public purse through savings on services across the public sector.

Early intervention in children’s services

The Independent Review of Children’s Social Care has identified that ‘It is getting harder to meet children’s needs within the current system and if we don’t take urgent action to prevent this, costs will continue to rise and the situation of children will deteriorate. There is no situation in the current system where we will not need to spend more’.

Councils would have the option to use the Community Investment Fund to invest in the early intervention support that their local children and families need, so that we can make sure help is available when it’s first needed – not later down the line when the situation has reached crisis point. Councils could target funding according to local priorities which might range from early years support to families to crime prevention activity focused on young people.

The Case for Change published by the Independent Review of Children’s Social Care highlights a range of evidence on the impact of investment in preventative services, including:

- reduced spending on preventative and family services is associated with rising rates of adolescents entering care

- an additional 8,750 to 24,400 children in need than would have been expected had spending on preventative and family services remained at 2010/11 levels

- spend on early help is associated with better Ofsted inspection outcomes.

There is also clear evidence on the benefits of specific programmes of prevention and early help, for example:

- the Troubled Families programme reduced the proportion of children in care and reduced juvenile custodial sentences and convictions

- greater coverage of Sure Start centres led to a fall in hospitalisations of children up to the age of 11, saving the NHS £5 million per cohort of children

- reducing the attainment gap between disadvantaged pupils and their peers across the country to the same size as in London would deliver an overall economic benefit of around £12 billion over the lifetimes of those young people.

Local flexibility is key, allowing councils to meet the needs of local families and effectively integrating with existing provision in a place-based approach to prevention and universal support.

Mental health

Supporting people’s mental health and wellbeing underpins all aspects of the COVID-19 recovery. From reopening schools, to getting the country safely back to work, dealing with the economic and housing consequences of the pandemic, and supporting people who may have become lonely or socially isolated. The Centre for Mental Health estimates that 10 million people, including 1.5 million children and young people, will need support for their mental health as a direct result of the pandemic over the next three to five years with some population groups at higher risk than others.

The annual cost of mental health problems in England is estimated to be £119 billion, measured in terms of spending on health and the impacts on an individual’s work or education. Mental health problems cost UK employers £35 billion a year in sickness absence, reduced productivity and staff turnover. Three-quarters of mental health problems first emerge before the age of 25, so it makes sense economically to invest in mental health support for young people, as well as making a huge difference to people’s lives.

Improving people’s mental health has the potential to help public finances as well. Evidence-based parenting programmes, for example, are estimated to generate savings in public expenditure of nearly £3 for every pound spent over seven years, with the value of savings increasing significantly longer term.

Community learning

There are other purposes for which the Community Investment Fund could be used, for example, realising the wider social and health benefits associated with councils’ community learning activity (currently funded through the Adult Education Budget) to engage those that most need support to start or restart their journey back into employment and which also helps reduce loneliness and ill health, improves social integration and active citizenship. This is however closely connected to current reforms to adult education funding through a new Skills Fund which must not lose the wide-ranging benefits of community learning. Any use of the Community Investment Fund for this purpose would have to be additional to, as a minimum, local government continuing to receive receiving at least £220 million through the new Skills Fund for delivery of community learning within an enhanced and adequately funded council-run adult and community education service.

Priority 4 - Reaching net zero

The Government has legislated to reduce carbon emissions by 78 per cent by 2035, and to reach net zero by 2050. To achieve these goals, Government will need to build effective partnerships to broker deals across a range of sectors.

Locally, councils have existing relationships with a whole host of partners which they can use to help deliver the individual changes needed to meet the national target. The majority of councils have declared a climate emergency and already areas such as Yorkshire and Humber and Hertfordshire have climate change partnerships involving their local NHS bodies and other major partners to look at how they can collectively meet emissions’ targets.

Councils have also supported the electric vehicle industry by investing in on and off-street electric vehicle (EV) charging infrastructure – contributing to the 21,000 public charge-points across the UK. Birmingham City Council has brought the first Clean Air Zone into operation which by 2026, is estimated to reduce the number of asthmatic children showing bronchitis symptoms by 873 a year. It will also contribute towards Birmingham’s commitment to a 60 per cent reduction in carbon emissions by 2027. Given that it is the single largest source of emissions in this country, transport has a significant role to play in helping the country to reach its net zero targets.

To deliver significant progress on net zero it is going to be necessary to ask the public to make further behavioural changes. The public have already made some of the easier changes, such as swapping to reusable shopping bags/water bottles and getting better at recycling. But the next phase of behavioural change is going to need more commitment from the public as we look to swap our modes of transport and seriously review our own personal consumption. The Committee on Climate Change estimates that future reductions in emissions will rely on as much as 62 per cent of our individual choices and behaviours.

Although there are significant challenges ahead there are also many opportunities for national and local government to work together. Councils will work as partners with Government to tackle climate change, using their place-shaping role and drawing on their longstanding ability to collaborate and build cohesion with local partners and residents. Community capacity and cohesion issues will arise in the transition to net zero and it is only at the local level that these can be addressed.

If the UK is to remain a leading global example, Government needs to unlock councils’ full potential. It is clear that the transition to a net-zero carbon society will require substantial additional public and private financial resources.

The Government should work with councils and businesses to establish a national fiscal and policy framework for addressing the climate emergency.

This framework should outline responsibilities for the Government nationally – for example, aligning the regulatory system, including the planning system and national tax incentives – and the local responsibilities, together with a commitment to cooperate with local public sector bodies. There should be a process of engagement between central and local government and industry to enable councils to fulfil their role to translate a national framework into transformative local plans that deliver on this agenda and invest in solutions for a green recovery and future.

The framework must be underpinned by a long-term revenue and capital package to address climate change and meet the net zero target. Local government can work with central government to help identify the costs and how they can be funded.

Alongside the framework we need to pilot place-based approaches that will help us speed up the pace of action and achieve economies of scale. We need to be bold and let local areas lead the green recovery and give them to opportunity to test radical new approaches, such as devolving skills and powers funding and responsibilities to speed up the green recovery. This could include further funding for specific village, town and city wide pilots on EV charging coverage, local energy schemes and other initiatives.

Decarbonising housing

Decarbonising existing council housing will require significant investment. Analysis undertaken by Savills for the LGA before the pandemic (available on request) estimated that the additional investment costs to achieve net zero carbon in existing housing stock held within councils’ Housing Revenue Accounts (HRA) is almost £1 billion per year over a 30-year pattern of investment. This will have an impact on other council housing programmes and the ability to deliver statutory functions.

There is an opportunity, through decarbonising both our existing housing stock and new build homes, to help economic recovery whilst achieving the shared local and national government’s net zero target. Targeted policies can support both the construction sector and low-carbon and job creation in deprived areas, including those most impacted by the pandemic thus also supporting the Government’s levelling up agenda.

Giving councils the tools, powers, flexibilities and resources that they need to decarbonise heat in homes, including bringing forward the £3.8 billion capital Social Housing Decarbonisation Fund will help the rollout of an ambitious national retrofit programme across all tenures that will create jobs, support local economies, cut fuel bills, and help tackle fuel poverty.

Transport decarbonisation and Local Transport Plans

Councils have much to do over the coming years to work with Government to deliver the Transport Decarbonisation Plan and the local schemes that will be needed to move away from carbon dependent travel. Councils will be looking to:

- prepare Local Transport Plans that deliver against quantifiable local carbon reduction targets

- consolidate their work and prepare a pipeline of cycling, walking and bus prioritisation schemes along with other transport initiatives to meet local transport priorities, as well as national targets, such as 50 per cent of all urban journeys to be cycled or walked by 2030

- respond to demand for electric and zero-emission vehicles, with a focus on provision for charge points for those without off-street parking

- respond to future transport trends – such as the roll out of escooter rental schemes and regulation of private escooter ownership and ‘last mile’ freight/delivery consolidation schemes

- further integrate transport and spatial plans.

In order to undertake these activities and be effective partners of Government councils will require additional resources to invest in capacity and expertise to develop plans and ensure quality and value-for-money scheme delivery.

Funding each highways authority with an additional £2.1 million revenue support for the remainder of this Parliament and committing an additional £700,000 each year for the next Parliament will help ensure councils are able to co-deliver the Government’s ambitious Transport Decarbonisation Plan.

This additional amount will help by ensuring every highways and transport authority has the minimum resources they need to plan, consult, design, promote and deliver their local schemes in contribution to the national Transport Decarbonisation Plan. It will also consolidate any existing revenue funding, such as for producing Bus Improvement Plans.

Waste and recycling