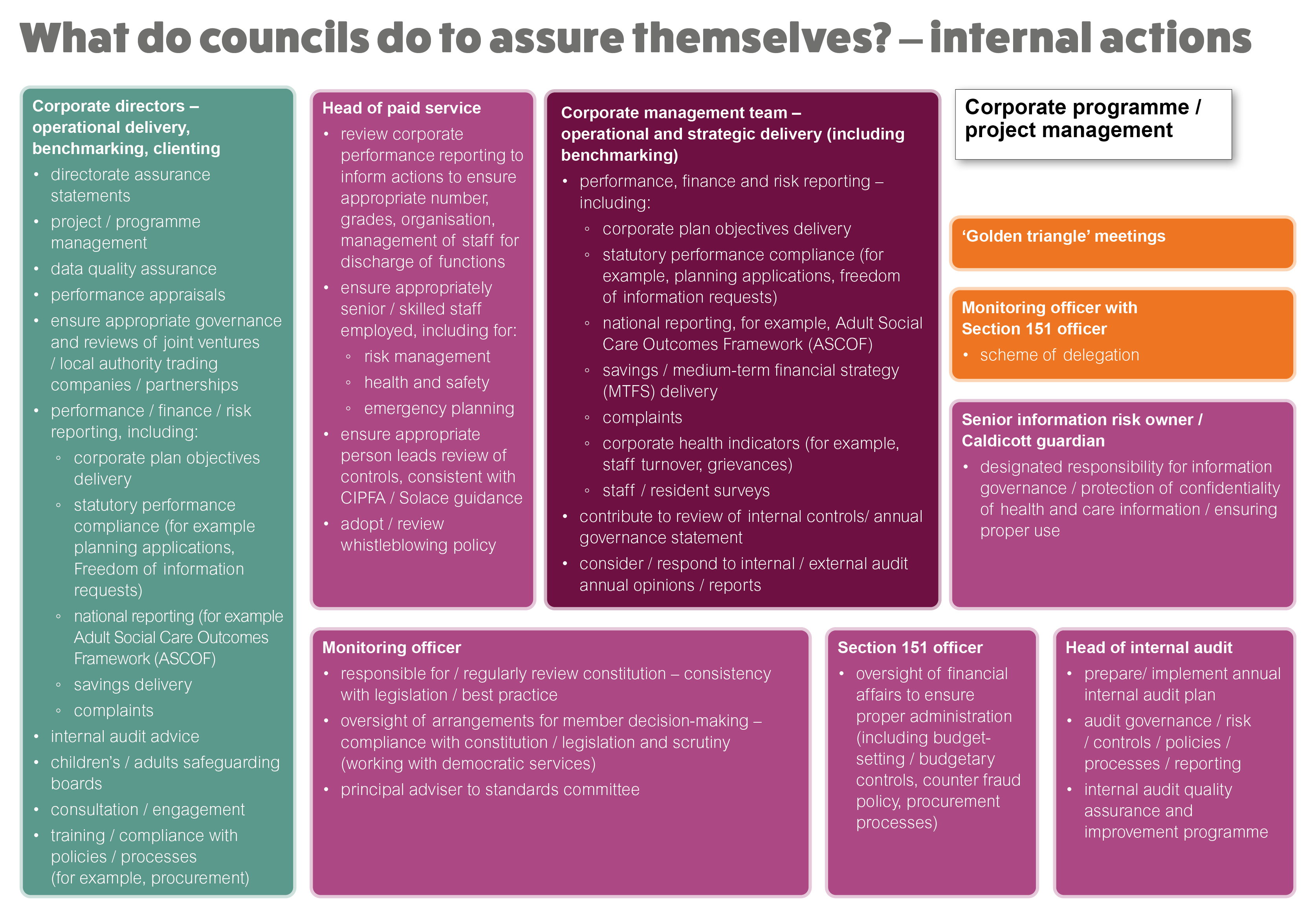

What do councils do to assure themselves (internal actions)?

Larger version of diagram mapping what councils do to assure themselves (see text version below)

{kind=link}

Corporate directors

Corporate directors seek assurance of operational delivery, benchmarking, clienting:

- directorate assurance statements

- project / programme management

- data quality assurance

- performance appraisals

- ensuring appropriate governance and reviews of joint ventures / local authority trading companies / partnerships

- performance / finance / risk reporting, including:

- corporate plan objectives delivery

- statutory performance compliance – for example, planning applications, freedom of information (FOI) requests

- national reporting – for example, the Adult Social Care Outcomes Framework (ASCOF)

- savings delivery

- complaints

- internal audit advice

- children’s / adults' safeguarding boards

- consultation / engagement

- training / compliance with policies / processes (for example, procurement).

Corporate programme / project management

Heads of paid service

Heads of paid service seek assurance through:

- reviewing corporate performance reporting to inform actions to ensure appropriate number, grades, organisation, management of staff for discharge of functions

- ensuring appropriately senior / skilled staff employed, including for:

- risk management

- health and safety

- emergency planning

- ensure appropriate person leads review of controls, consistent with CIPFA/ SOLACE guidance

- adopt / review whistleblowing policy.

Corporate management team

The corporate management team seeks assurance of operational and strategic delivery, including benchmarking) through:

- performance, finance and risk reporting, including:

- corporate plan objectives delivery

- statutory performance compliance, for example, planning applications, freedom of information (FOI) requests

- national reporting – for example, the Adult Social Care Outcomes Framework (ASCOF)

- savings / delivery of medium-term financial strategy (MTFS)

- complaints

- corporate health indicators (for example, staff turnover, grievances)

- staff/ resident surveys

- contributing to review of internal controls / annual governance statement

- considering and responding to internal / external audit annual opinions / reports.

'Golden triangle' meetings

Monitoring officers with Section 151 officers

Monitoring officers with Section 151 officers are responsible for:

- scheme of delegation.

Monitoring officers

Monitoring officers are responsible for:

- regularly reviewing constitution – consistency with legislation / best practice

- oversight of arrangements for member decision-making compliance with constitution / legislation and scrutiny (working with democratic services team)

- principal advisers to standards committee.

Section 151 officers

Section 151 officers have oversight of financial affairs to ensure proper administration, including budget-setting, budgetary controls, counter-fraud policy, procurement processes.

Heads of internal audit

Head of internal audit are responsible for:

- preparing and implementing annual internal audit plan

- audit governance, risk, controls, policies, processes, reporting

- internal audit, quality assurance and improvement programme.

Senior information risk owners and Caldicott guardians

Senior information risk owners and Caldicott guardians have designated responsibility for information governance, protection of confidentiality of health and care information, ensuring proper use.

What do councils do to assure themselves (actions by councillors and officers)?

Councillors and officers

Councillors and officers are responsible for:

- giving and receiving professional advice to inform decision-making

- regularly reviewing performance and risk (portfolio holders / directors)

- community safety partnership

- commissioning peer-led reviews from regional networks / professional bodies / Local Government Association (LGA)

- establishing a council Improvement board (where appropriate).

What do councils do to assure themselves (externally visible actions)?

Externally visible assurance actions include:

- executive / policy and resources committee reviews performance / finance / risk reporting on strategic delivery

- overview and scrutiny committee/s' actions

- appointments committee recommends to full council appointment of appropriately qualified statutory officers

- audit committee monitors / reviews controls, approves internal audit plan, reviews internal / external audit reports, has oversight of management responses, reviews own practice

- committee with delegated responsibility for governance reviews annual governance statement, oversees regular reviews of constitution

- standards committee reviews member code of conduct, arrangements for conduct complaint investigations, reviews monitoring officer’s annual report

- pensions committee is accountable to scheme members

- heads of paid service, Section 151 officer, monitoring officer, directors of children's services have individual duties to report to full council

- full council – responsible for Section 25 statement, reviewing scrutiny, publishing audit standards annual reports, holding scrutiny, audit, standards chairs to account, appointing statutory officers.

What do other bodies do to gain assurance about councils (not publicly visible actions)?

Actions that other (non-public) organisations do assure themselves include:

- grant-funding bodies – reporting requirements

- regional networks – benchmarking, challenge, support

- professional bodies – standards, qualifications, capability/ disciplinary, tools to support decision-making

- government departments – ad hoc requests

- Department of Levelling Up, Housing and Communities (DLUHC) officials – early engagement with challenged councils

- political parties – assurance / disciplinary processes.

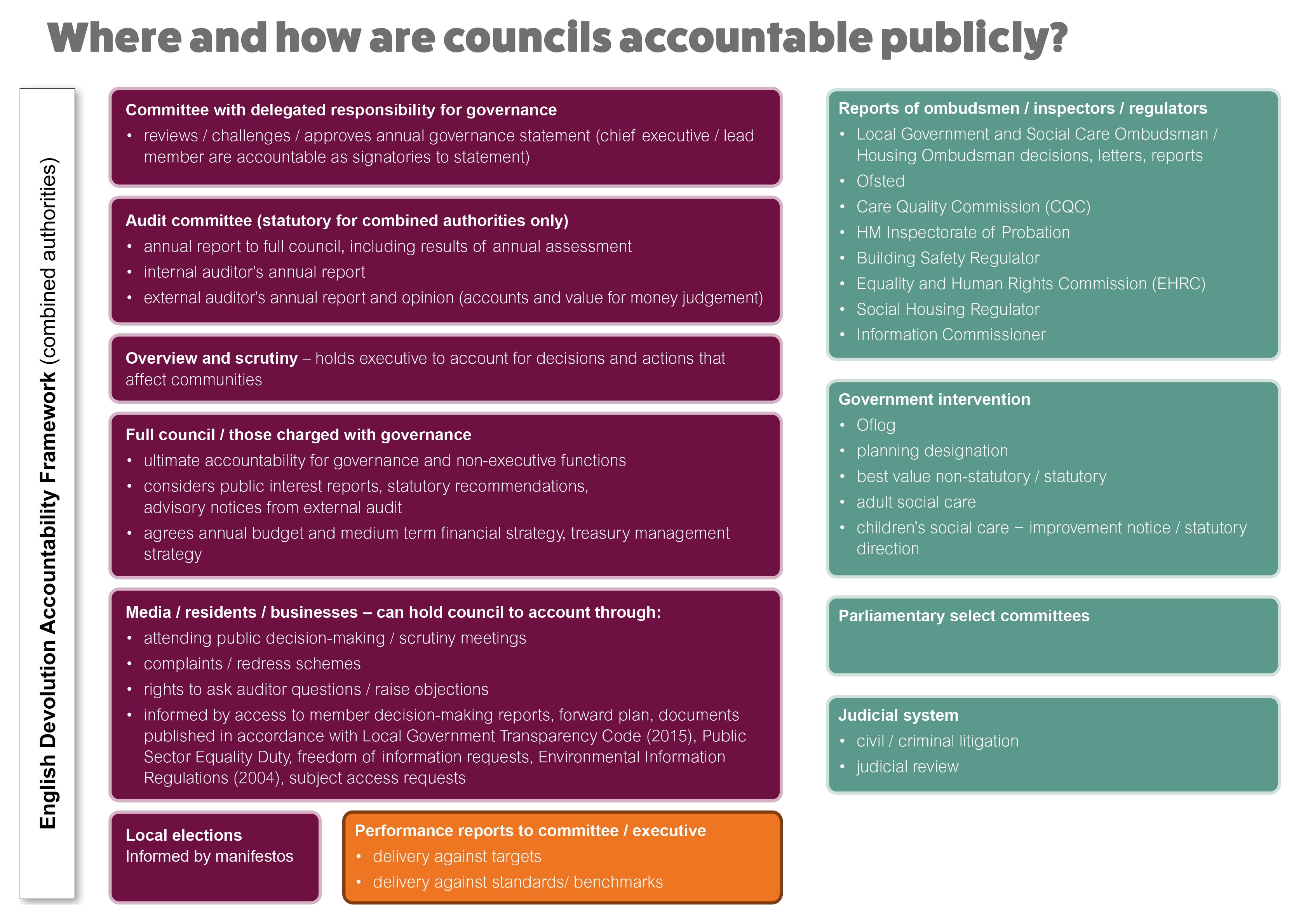

Where and how are councils accountable publicly?

Larger version of diagram mapping where and how councils are accountable publicly (see text version below)

{kind=link}

English Devolution Accountability Framework

The English Devolution Accountability Framework sets out assurance arrangements for combined authorities.

Committee with delegated responsibility for governance

The committee with delegated responsibility for governance reviews, challenges and approves the annual governance statement.

The chief executive and lead member (councillor) are accountable as signatories to the annual governance statement.

Audit committee

The audit committee, which is statutory for combined authorities only, is responsible for an annual report to full council, including results of annual assessment.

The committee considers:

- internal auditor’s annual report

- external auditor’s annual report and opinion (accounts and value-for-money judgement).

Overview and scrutiny

The overview and scrutiny function holds the executive to account for decisions and actions that affect communities.

Full council

Members of the full council are 'those charged with governance'. The full council:

- has ultimate accountability for governance and non-executive functions

- considers public interest reports, statutory recommendations, advisory notices from external audit

- agrees annual budget and medium-term financial strategy (MFTS) and treasury management strategy.

Media, residents and businesses

Media, residents and businesses can hold the council to account through:

- attending public decision-making / scrutiny meetings

- complaints / redress schemes

- rights to ask auditor questions / raise objections

- informed by access to member decision-making reports, forward plan, documents published in accordance with Local Government Transparency Code (2015), Public Sector Equality Duty, freedom of information (FOI) requests / environmental information regulations (EIRs) / subject access requests (SARs).

Local elections

Local elections are informed by manifestos.

Performance reports to committee / executive

Performance reports to committee / executive report on:

- delivery against targets

- delivery against standards / benchmarks.

Ombudsmen, inspectors and regulators

Ombudsmen, inspectors and regulators include:

- Local Government and Social Care Ombudsman / Housing Ombudsman decisions, letters, reports

- Ofsted

- Care Quality Commission (CQC)

- HMI Probation

- Building Safety Regulator

- Quality and Human Rights Commission (EHRC)

- Social Housing Regulator

- Information Commissioner.

Government intervention

Government intervention includes:

- Office for Local government (Oflog)

- planning designation

- best value – non-statutory / statutory

- adult social care

- children’s social care – improvement notice / statutory direction.

Parliamentary select committees

Parliamentary select committees may hold councils to account.

Judicial system

-

civil / criminal litigation

-

judicial review.

Take part in our consultation

We aim to map the various elements that provide assurance of the performance of local government and to demonstrate how they all fit together. We hope that this framework will be useful both for councils and the public.

We would be grateful if you would give us your thoughts on the current components of the improvement and assurance framework for local government by completing our survey.

Find out more about our work on the Improvement and assurance framework for local government.