This guide has been written to assist local planning authorities publish their Infrastructure Funding Statement (IFS). This is an August 2023 edition which has taken account of practice over the three years since they were made a statutory requirement .

This guide

This guide has been written to assist local planning authorities publish an Infrastructure Funding Statement (IFS). It was produced with the help of colleagues from the Department for Levelling Up, Housing and Communities (DLUHC) and has been informed over time by engagement with local authority practitioners.

This version of the guide has been updated to reflect lessons learnt from the first three years of IFS preparation and publication covering the financial years 2019/20, 2020/21 and 2021/22. We will continue to issue updates to this guide as we collectively learn more – or indeed to replace it in due course with new guidance to explain the infrastructure levy that has been introduced through the Levelling Up and Regeneration Bill with government consulting on the detailed design of the levy in March 2023. Whatever happens next, we are confident that the principles of transparency and accountability around the collection and spending of developer contributions are here to stay.

What is an Infrastructure Funding Statement (IFS)? Do I have to prepare one?

An IFS is a document that must be published each year by a “contribution receiving authority”. A contribution receiving authority is any authority which issues a Community Infrastructure Levy (CIL) liability notice or receives money or in-kind works from a Section 106 agreement. This means almost all local planning authorities need to produce one, including county councils. Counties that enter into a section 106 agreement as a signatory must report the agreement in an IFS. It is also good practice for counties to account in the IFS for funds passed to them by districts. Where parishes receive a proportion of CIL they need to produce a report for each financial year in which they receive CIL receipts too.

Authorities that charge CIL have had to produce a report on receipts and expenditure since the regulations were introduced in 2010, but the requirement to report on section 106 was introduced in 2019. The legislation requires local planning authorities to publish their “combined” IFS covering both CIL and section 106 contributions on or before the 31st December of each year and for it to include information on the preceding financial year. The first IFS information covered the period 1st April 2019 to 31st March 2020 with the requirement to publish the IFS on or before 31st December 2020. The information that must be provided is set out in Schedule 2 of the CIL regulations 2010 (as amended) and relates to all the activity in the relevant financial year as well as requiring information on unspent money collected in previous years. This meant for the first IFS some local planning authorities were required to perform a “stock take” of obligations from lots of old agreements to establish whether they relate to unspent funds that need to be reported. Updating this information should have become easier when reporting for future years IFS.

What should be included in an IFS?

There are three components to an IFS. Annex 1 includes a table that lists out the components to the IFS and whether they are a “must include” or “should include”.

1. The CIL regulations 2010 (as amended)

The first is a mandatory requirement as set out in the CIL Regulations 2010 (as amended). Regulation 121A requires the contribution receiving authority to publish an IFS which includes:

- The infrastructure projects or types the authority intends will be, or may be, funded at least in part by CIL

- A CIL report

- A planning obligations (Section 106) report

Schedule 2 sets out the detailed information that should be included in the reports and also includes an option to report on Section 278 agreements for highways works.

2. Planning practice guidance

The second set of requirements are non-mandatory but are encouraged through planning practice guidance. Government guidance also includes recommendations on publishing more detailed developer contributions data in a set of tables at a level of individual transactions. This provides for transparency and accountability at the level of individual obligations. Some software systems offer the facility to export compliant tables very simply. Councils without these systems – e.g. those using a simple spreadsheet or home-made database – are encouraged to translate their data into the standard format recommended by DLUHC.

3. Promotion of delivery through planning obligations

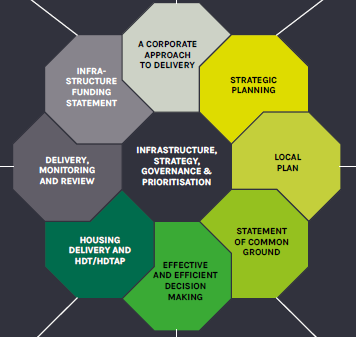

Lastly there is an opportunity to use the IFS to showcase how the council is developing and delivering an infrastructure strategy. Telling the whole story might mean that some projects from a different regulatory or funding regime should also be included. This might also support the development of infrastructure delivery strategies which have been outlined as a potential new requirement through the Levelling Up and Regeneration Bill. It is important that local planning authorities showcase what infrastructure they are delivering to support development in their area to help stakeholders and communities understand.

Types of IFS

It would be easy to see IFS reporting as a burden and just another regulatory requirement. We think they are an excellent way to demonstrate capable governance and effective delivery. For support and top tips on best practice for good governance of developer contributions see our guidance on “Improving the governance of developer contributions” and our associated self-assessment tool

For some councils (those who do not charge a CIL) the IFS may have been the first public statement on infrastructure delivery via developer contributions. It is important that authorities decide collaboratively on what sort of job they want the IFS to do, and this may be influenced by how much time and effort they want to spend on it. For example:

- A “bare bones” but compliant IFS might be 2 or 3 pages long and provide totals and high-level themes and categories in an infrastructure plan (although authorities are encouraged to do more);

- A basic IFS might be broken out by ward and detail schemes already underway in an accessible way. It will contain a narrative to explain the numbers;

- A “full” IFS will have photographs and details relevant to businesses and communities showcasing what developer contributions have helped to deliver. It will set out existing infrastructure priorities and give details of how new schemes and ideas will be considered. It will contain messages from councillors who set the vision and make choices on projects.

As with all council documents it is for them to decide an appropriate level of “sign off” before publication. We have heard a wide variety of approaches – everything from no process at all right up to full council or even Mayoral agreement. For some local planning authorities, section 106 agreements have been very much a technical and legalistic subject dealt with in the planning department. The direction of travel is to continue to strengthen councils’ roles as infrastructure providers and make infrastructure planning much more transparent. This inevitably means more corporate and political responsibility and ownership to ensure successful delivery of projects.

The wider role of the IFS

The thinking and organisation required to make a good IFS serves a broader benefit. One of the biggest risks for councils taking developer contributions is that there is a reputation of them leaving funds unspent even after many years. This raises questions of whether the contributions were genuinely needed, and creates doubt that councils are reliable custodians of the money. In turn, this places a burden on councils who receive many Freedom of Information requests. This can be avoided by establishing some clear governance processes and principles that explain how an infrastructure strategy leads to allocation and delivery on projects that support development in an area. Publishing sufficient detail in the IFS and supporting tables to avoid the cost of answering individual FOI and EIR is one strong argument for publishing the additional data.

In 2020 PAS published a guide for senior leaders called “Start with the spend in mind”. This sets out in a series of fact sheets on the choices facing senior officers and councillors and how the various parts of the planning system reinforce each other when used well.

Building on this we have also published detailed guidance aimed at helping councils improve their governance of developer contributions and better support collaborative infrastructure planning and delivery. This was informed by individual workshops with around 40 councils where we undertook health-checks of their governance processes. This involved working with officers and Members across councils who are involved in negotiating, monitoring, allocating and spending developer contributions. This work has helped us to develop a self-assessment toolkit for councils to undertake their own health-checks of their end-to-end processes. We strongly advocate the use of these resources to help ensure effective governance arrangements are in place and that this area of work has the appropriate level of corporate attention and resource.

We strongly encourage councils to use the IFS as a form of promotion. In part this flows from a study commissioned by DLUHC that found that the public had not made a link between developer contributions and the delivery of affordable housing, community facilities and the like. Improving the communication may help influence the public’s attitude towards development. Set against that is the need to manage expectations – many councils have quite large sums of money recorded in their IFS but they are already allocated to large and long-term infrastructure projects like roads and schools. The funds are not being “sat on” but instead accrued for large scale expensive projects and they are not therefore available to other bids. The IFS is an opportunity to present cases like this in a clear and transparent way.

IFS reporting is a snapshot

An annual publication, especially if including the transaction level detail, is going to be a snapshot of a moment in time. Care should be taken to describe infrastructure priorities in such a way that does not close down opportunities or make everything seem locked and unable to change.

We heard from officers that there was a worry that the IFS would not be complete with every detail, and indeed it is the nature of some obligations that they take time to resolve into an agreed figure. In almost every case the correct course of action was to take the opportunity to use the IFS to explain the context and the intention, and to accept that it is in the nature of infrastructure planning that things change. This is most obvious when councils consult and engage their communities on their priorities.

There is also good practice starting to emerge in two areas crucial to the long-term success of good infrastructure planning:

- Engagement across local government boundaries - we have seen some excellent practice where county and district councils were spending time keeping each other informed on both emerging priorities but also the delivery of schemes where money was being passed to counties as a delivery partner.

- Finding a political route – in the past some planners have been wary of letting councillors make decisions on infrastructure schemes for fear that they could favour their own ward or try to generate some kind of electoral advantage. We heard from Sevenoaks who have introduced a member-led panel who allocate CIL and have a structured bidding process. They also have a dashboard so communities can self-serve details on which applications have generated payments and how much is available for them to spend.

We have spent some time considering the proposals for a new infrastructure levy as part of the Levelling Up and Regeneration Bill and how that might change things for councils. Importantly this would increase the requirement for proper and transparent infrastructure planning and delivery, so time spent getting the principles right now would not be wasted.

IFS and statements about the future

There has always been a concern that there is a significant difference between the “reporting the facts” part of an IFS (e.g. balances received) and making statements about likely future receipts and infrastructure priorities. In our view this should not restrict the willingness of local authorities to set out how funds might be used in the future or what might be received, providing that appropriate caveats are made clear.

The government’s guidance on CIL suggests a narrative that sets out how developer contributions will be used to deliver plan policies, including projects or types of infrastructure. This recognises the statement’s opportunity to communicate and reinforce a model of delivery rather than a new and binding commitment. Where there is a degree of confidence about future income that can be shared too.

Pulling together to make an IFS

The production of an accurate IFS requires coordination between many different authorities and agencies. Some, like districts and parishes, will have inherited a variety of work practices. Others, may not be familiar with “reporting back” and explaining what has happened to the infrastructure funds.

It is probable that many statements will have some estimates and best guesses, and this will continue until the planning system updates its underpinning processes with automation and digital standards. Until then it might be prudent to agree a condition with delivery partners that project funding is contingent on a requirement to report back on progress towards delivery.

Each collecting authority will have its own context and partners, but we have put together the following checklist:

| Partner | Information to consider / role in developing IFS |

|---|---|

| Infrastructure providers |

|

| Leadership team (Officers and Members) |

|

| Planning |

|

| Spending departments |

|

| Partner authorities e.g. County, GLA |

|

| Local councils including Parish and Town Councils |

|

Format and design of your IFS

It is for each council to decide the format and design of their published IFS whilst ensuring that all of the legislative requirements are met. Below are some examples of IFS that we think present this information well. We have also published separately at Annex 2 of this guide a sample IFS with ideas on how the information can be presented. Annex B of this template provides a checklist of the information that is required through legislation. We would strongly urge that all councils populate this table and include it in their IFS either as an executive summary or as an appendix to the main document. This will aid transparency of information as well as help you to ensure that all of the necessary information has been included.

Accessibility

Public sector organisations have a legal duty to make sure all their digital content and products meet the accessibility regulations. Accessibility, simply put, is the degree to which a system or service is available to as many people as possible. You should work with your digital and communications teams at your local authority at the earliest opportunity to ensure that your IFS meets the accessibility requirements when published.

Publishing your IFS

You must be able to upload your IFS to your local planning authority’s website to make it publicly available. Make sure the URL for where your IFS is hosted is persistent (a web address that will not change over time). If your website does not have a page on developer contributions, you or someone in the web team will need to create one.

When you upload the files you should keep your older files online – it’s important to retain a history of all developer contribution files.

Each council will have a website structure and pre-existing network of corporate reports and publications. Please email the web address of your IFS to DLUHC at [email protected] to confirm that you have published your IFS. This will also allow them to collate all IFS data to produce a national picture of developer contributions.

Lessons from previous years IFS publications

Improved collaboration – officers have reported greater collaboration and working relationships with other areas of the council who hold information that is required for inclusion in the IFS. This might for example include funding allocated but not spent for affordable housing, or monies spent on specific projects. The IFS has helped councils to improve their processes and data collection between different service areas.

More efficient data collection - officers have reported that pulling together information for the IFS was much easier and more efficient in the second year. This is because historic information had been compiled for year one and as such year two was focussed on proportionate updates. With clear arrangements in place for collection of this data the development of the IFS should become more streamlined each year.

Schemes of delegation – ensure that you are clear on the route for approving your IFS for publication. This will be specific to your council and it is important that you factor in enough time for decision making cycles to meet the publication deadline of 31 December each year for the previous financial reporting year.

Format of financial information – many councils ledger financial credits on their systems as a minus sum against demands which are shown as positive. This has meant where information has been directly taken from financial records that some councils have presented receipts in their IFS as negative sums. Be careful and make sure that you are presenting accurate information as this is a public document and should be clear and transparent for public information. Work with your finance colleagues to make sure that figures are understandable and clearly presented.

Examples of IFS we like

The guidance from DLUHC is mostly concerned with the data specifications, not what the document should look like. It is for each collection authority to decide, and this should be based on a common-sense assessment of the work required, value to the reader and corporate brand. Here are three examples of IFS that we think are particularly good.

Overview of preparing and publishing data on developer contributions

The following section provides guidance on preparing and publishing the underlying data that informs the infrastructure funding statement.

The previous version of this guidance note built on the Government’s guidance ‘Publish your developer contributions data’. However, they have now moved away from recommending the use of the CSV file approach as a method of capturing this information. This method was never mandatory, but Government at the time considered that it might be helpful, particularly for those who do not have an automated system to record data or do not use a third-party provider which is able to prepare the data in a suitable format. For those local planning authorities that do wish to continue to use this approach we have archived the earlier version of this guidance and it is included as Annex 3 to this guide.

Advice on the legislative requirements for producing your infrastructure funding statement is included at Annex 1.

Gathering information

The first step is to gather the relevant information on section 106 agreements and CIL demand notices and receipts. You do not need to record section 106 agreements where the proceeds have been ‘spent’ in previous years. However, you should record historic agreements where sums have been paid by developers in previous years where those sums have not yet been spent.

It is recognised that the first year (2019/20) was probably the most difficult because of the amount of information you may have needed to collect and record, although CIL authorities will already have been doing this for CIL receipts and spend. Going forward, regular recording of data will make reporting in future much easier and this has been the experience for councils when producing their second and third IFS for the financial years 2020/21 and 2021/22.

Definitions for recording the intended purpose of developer contributions

Paragraph 179 of the planning practice guidance on CIL provides a list of infrastructure categories/purposes that should be used for headline figures. These will be reviewed over time to see if they are appropriate and cover the main types of infrastructure delivered through developer contributions. Local authorities should decide for themselves which category to use to record an item of infrastructure. Definitions have been provided below for guidance.

It is recognised that there is overlap between some of the categories. For example, a sum might be used to extend an area of open space to enable it to be used for sport. As open land, it could contribute towards flood management and may, through (for example) tree planting at the edges provide additional green infrastructure. For the purpose of recording the intended purpose of the contribution, it should be recorded under the main intended purpose. In this example, it is likely to be recorded under ‘Open space and leisure’.

The regulations require the infrastructure funding statement to include a summary of the individual items of infrastructure that are provided through developer contributions and the amount spent on each. The categories listed in the planning practice guidance should be used to provide a broad breakdown of infrastructure types. However, you might want to be more explicit in your infrastructure funding statement. For example, if a section 106 payment is used to fund a roundabout, you will probably want to record it as a roundabout in your infrastructure funding statement rather than under the generic term ‘transport and travel’.

Summary of data requirements for Section 106 planning obligations

Planning obligations have to be linked to the particular development they relate to. It should therefore be possible to monitor and report the individual stages in the process from signing a planning agreement, through receiving contributions, allocating to a specific obligation for delivery and when monies are spent.

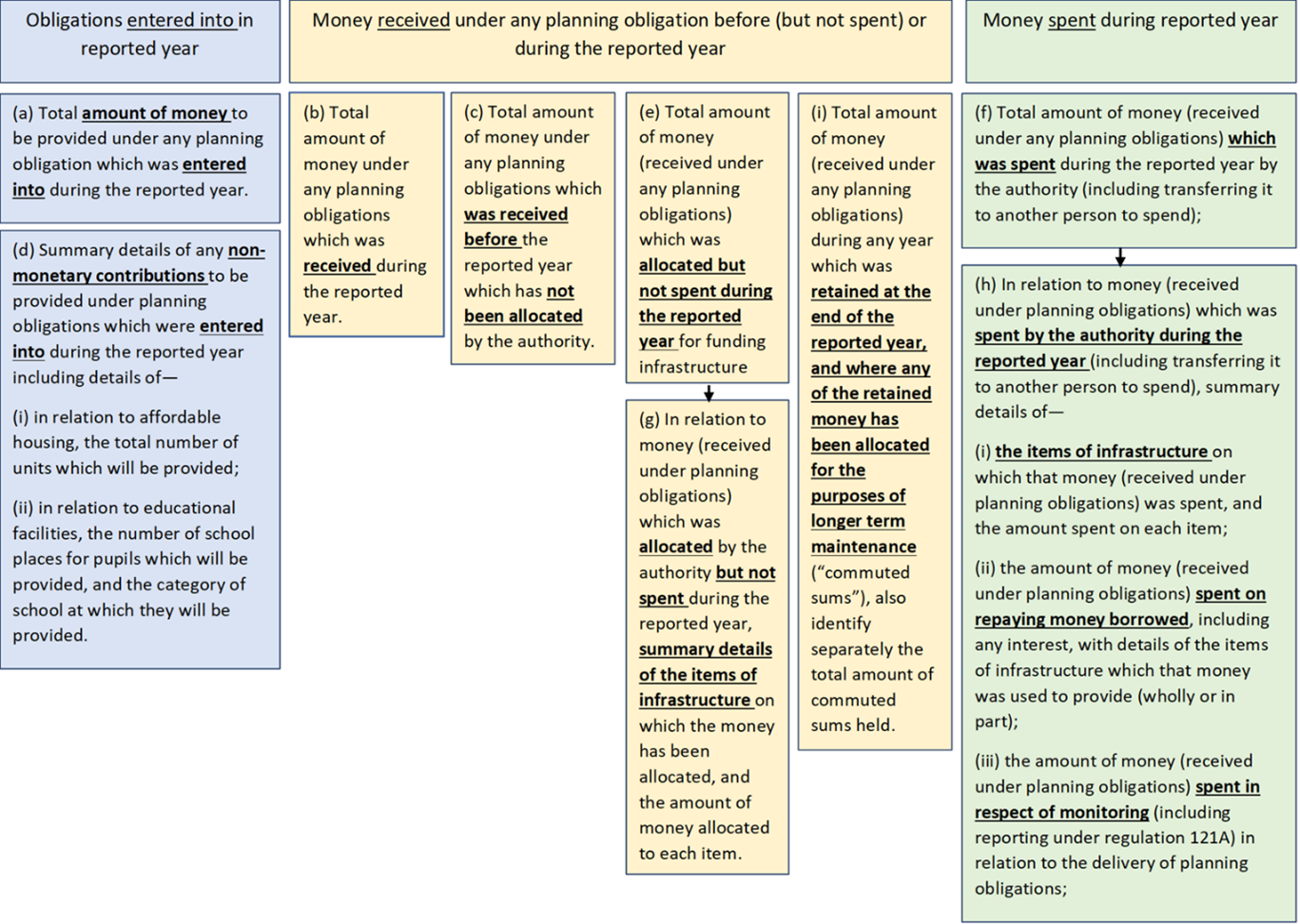

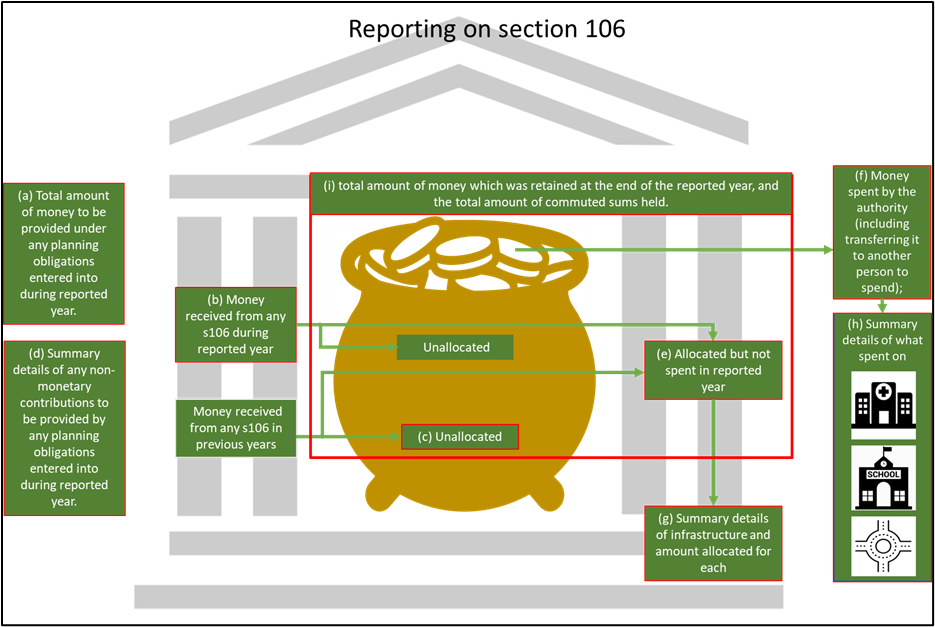

Figure 3 provides a breakdown of the information on section 106 planning obligations which must be included in your infrastructure funding statement as set out in Schedule 2 to the Regulations. Figure 4 provides a more diagrammatic representation of the information requirements.

The main focus of the IFS is what has happened in the reported year. There are four main categories of data:

- Obligations that have been entered into in the reported year;

- Money that has been received in any year but not spent;

- Monies that have been allocated but not spent during the reported year;

- Money that has been spent during the reported year.

Note that historic planning obligations only need to be reported where money has been received in the reported or in previous years but has not yet been spent.

The section 106 report can also include summary details of any funding or provision of infrastructure which is to be provided through a highway agreement under section 278 of the Highways Act 1980 which was entered into during the reported year (see paragraph 4 of Schedule 2 to the Regulations).

Identifying categories of Section 106 planning obligation

For section 106 planning obligations, the intended purpose of the contribution should be identified using the following categories. Brief definitions are provided below, but local authorities are best placed to decide which category to use and to use the infrastructure funding statement to provide more detail.

| Category | Definition |

|---|---|

| Affordable housing | Affordable housing is defined in the glossary of the NPPF as: housing for sale or rent, for those whose needs are not met by the market (including housing that provides a subsidised route to home ownership and/or is for essential local workers). It includes: Affordable housing for rent; Discounted market sales housing; and other affordable routes to home ownership. Qualifying conditions for each of these routes is set out in the National Planning Policy Framework’s glossary. Record the count of homes not value. |

| Bonds (held or repaid to developers) | These include financial securities which will need to be paid at certain trigger points during the development. |

| Community facilities | Community facilities can include the provision of buildings and spaces such as village halls, community centres, places of worship, meeting places and libraries. To avoid double counting, health and educational facilities should be recorded under their main categories. |

| Digital infrastructure | This includes electronic communications networks, such as next generation mobile technology (such as 5G) and full fibre broadband connections. It also includes radio and electronic communications masts, and the sites for such installations. |

| Education |

This should include all school phases aged 0-19 years, special educational needs (which could involve greater travel distances), and both temporary and permanent needs where relevant. For the purpose of reporting the provision of additional school places, the data on school places should be split into the following age groups: Primary; Secondary; Post-16; Other. |

| Flood and water management | This includes infrastructure with the purpose of managing the risk of flood and coastal erosion. This can include structural measures to reduce the likelihood and impact of floods, such as hard defences and flood relief works. It can also include soft defences such as green infrastructure (e.g. natural flood management and sustainable drainage systems). |

| Green infrastructure |

Green infrastructure is defined in the NPPF as “a network of multi-functional green and blue spaces and other natural features, urban and rural, which is capable of delivering a wide range of environmental, economic, health and wellbeing benefits for nature, climate, local and wider communities and prosperity”. Green infrastructure can embrace a range of spaces and assets that provide environmental and wider benefits. It can, for example, include parks, playing fields, other areas of open space, woodland, allotments, private gardens, sustainable drainage features, green roofs and walls, street trees and ‘blue infrastructure’ such as streams, ponds, canals and other water bodies. It includes the provision of Suitable Alternative Natural Greenspace (SANG) which is provided to avoid or mitigate the impact of increased human activity on certain habitats and species in protected areas. |

| Health | This includes facilities needed for primary, secondary and tertiary care. |

| Highways | This relates to agreements entered into under section 278 of the Highways Act 1980. |

| Land | This includes land which is provided instead of money. |

| Open space and leisure | Open space is defined in the NPPF as “All open space of public value, including not just land, but also areas of water (such as rivers, canals, lakes and reservoirs) which offer important opportunities for sport and recreation and can act as a visual amenity”. This category can also include formal sports pitches, open areas within a development, linear corridors and country parks. |

| Section 106 monitoring charges | Authorities can charge a monitoring fee through section 106 planning obligations, to cover the cost of monitoring and reporting on the delivery of that section 106 obligation. Monitoring fees can be used to monitor and report on any type of planning obligation, for the lifetime of that obligation. Monitoring fees should not be sought retrospectively for historic agreements and they should not exceed the estimated cost of monitoring the obligation. They must be reported in the infrastructure funding statement. |

| Transport and travel | This includes measures to improve accessibility and safety for all modes of travel, particularly for alternatives to the car such as walking, cycling and public transport, and measures that deal with the anticipated transport impacts of the development such as new access roads, and roundabouts. |

| Other | Any infrastructure which does not fit in the categories above. You will be able to describe these in your infrastructure funding statement. DLUHC will review infrastructure types recorded under the ‘other’ category and may in the future expand this list of categories. |

Reporting on in-kind Section 106 planning obligations

For section 106 planning obligations you should report on the number of units to be provided as ‘in-kind contributions’ (e.g. number of school places, number of units of affordable housing). If the in-kind contribution includes items such as land, you should record this as the equivalent land value rather than the number of units.

Identifying planning obligations that have been “allocated”

The infrastructure funding statement (IFS) must set out the amount of future planning obligation expenditure where funds have been allocated. ‘Allocated’ can mean either (i) a decision has been made by the local authority to commit funds to a particular item of infrastructure or project and/or (ii) the funds have been passed to a team within the authority to spend. The regulations require you to provide summary details of the items of infrastructure on which the money has been allocated and the amount allocated to each item. It is recommended that you explain the exact status of sums that have been allocated but not spent in your IFS.

Recording planning obligations where delivery is uncertain

Where there is uncertainty about what will ultimately be delivered, it is recommended that the most likely outcome is recorded. This can be amended in future years, and if significant, explained in the free text sections of your infrastructure funding statement.

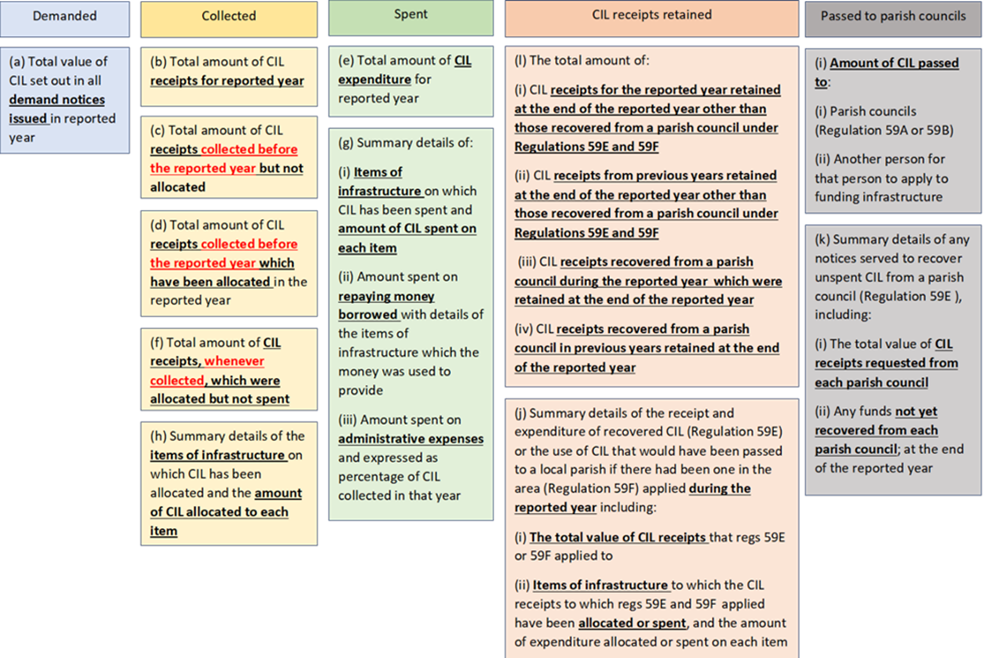

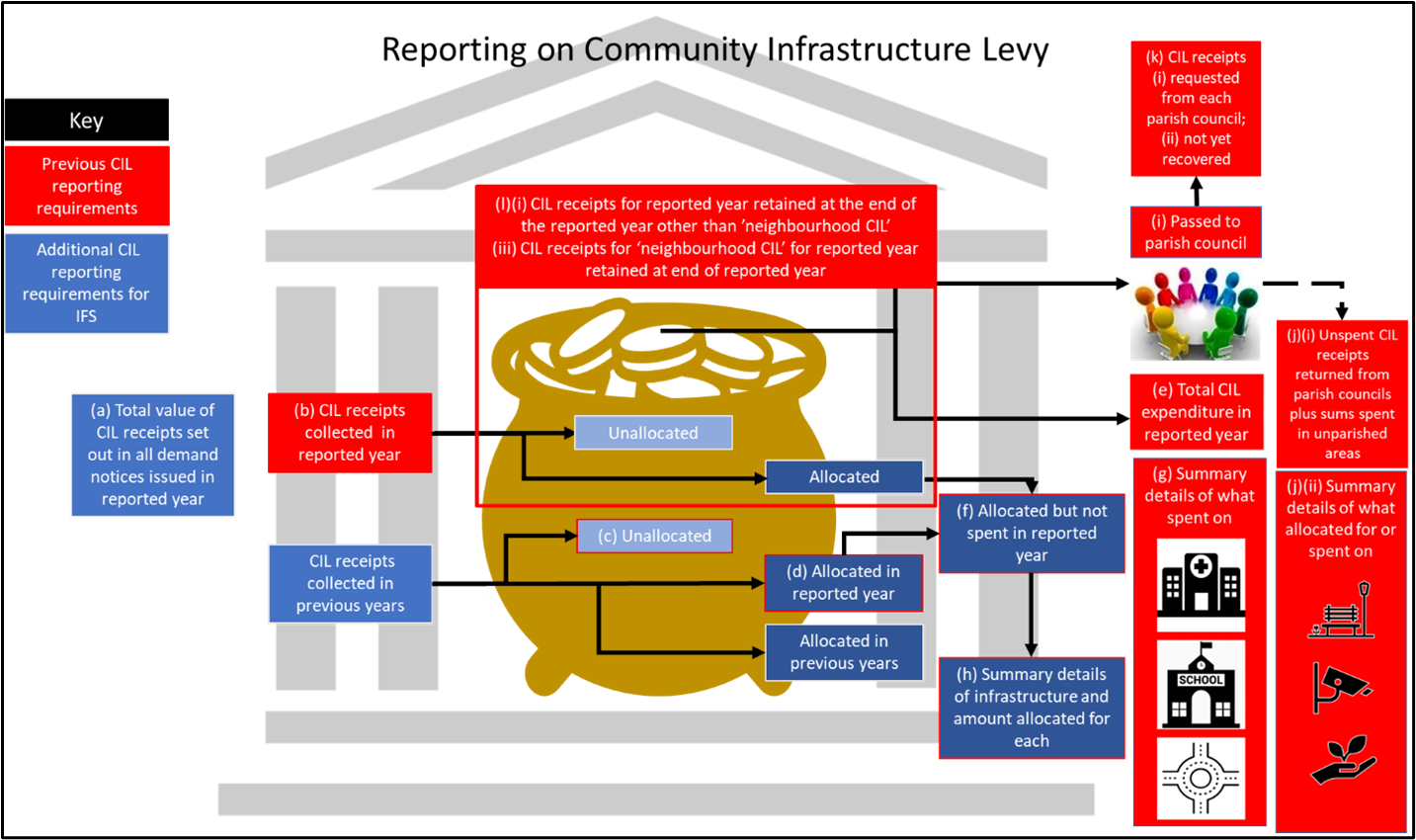

Summary of the data requirements for the Community Infrastructure Levy (CIL))

For CIL, the money received goes into a central ‘pot’, and monies from this pot are then allocated and spent on infrastructure. The allocation and spend is not normally attributable to individual planning permissions.

The focus is on what has happened in the reported year albeit you must also include data on funds collected in previous years but which were not spent at the start of the reporting year. There are five main categories of data to include in your infrastructure funding statement:

- Demanded: The total value of demand notices issued during the reported year.

- Collected: Including receipts for the reported year; receipts collected before the reported year which have been allocated in the reported year; receipts collected before the reported year which remain unallocated; total of all receipts that have been allocated in the reported year but not spent; and summary details of the infrastructure that CIL has been allocated to and the amount.

- Spent: Money spent during the reported year and what it was spent on; the amount of CIL spent on administrative expenses

- Retained: CIL receipts retained for the reported year and earlier years; CIL receipts and expenditure for areas that do not have Parish or Town Councils; and details of CIL receipts and expenditure of CIL recovered in the reported year and earlier years from Parish Councils.

- Passed over: Money passed to parish councils and other persons and details of recovered funds.

Figures 4 and 5 below illustrate the information on the Community Infrastructure Levy which should be included in your infrastructure funding statement.

Reporting on Mayoral CIL

London boroughs that collect CIL on behalf of the Mayor of London should identify these sums separately. The administrative cost of collecting CIL on behalf of the Mayor (4% of the total) should be included in the figure and not identified separately.

Reporting on in-kind CIL contributions

For CIL, the value of any acquired land or infrastructure payment should be recorded as the equivalent cash value as stated in the agreement made for that land or in respect of the infrastructure. You might want to record when these contributions are met either wholly or in part and you have the opportunity to explain in more detail in the free text in your infrastructure funding statement.

Recording CIL instalment payments and surcharges

You should record what money you have received and when. Instalment payments should therefore be recorded as each instalment is received. Similarly, any surcharges should be included within the total sum.

Annex 1 – A table of contents for the IFS

The tables are in two parts – those matters that “must” be in the report because they are required by regulations and others that “should” be in the report in guidance.

| Matters that must be included in the CIL report |

|---|

| Total value of CIL in demand notices for the reported year |

| Total amount of CIL receipts for the reported year |

| Total amount of CIL receipts collected before the reported year but which have not been allocated |

| Total amount of CIL receipts allocated in the reported year |

| Total amount of CIL expenditure for the reported year |

|

In relation to CIL expenditure for the reported year summary details of:

|

| In relation to receipts, whenever collected, which were allocated but not spent in the reported year summary details of the items of infrastructure on which CIL (including land payments) has been allocated and the amount of CIL allocated to each item. |

|

Amount of CIL passed to –

|

| Total amount of receipts in the reported year of CIL that has been recovered (Reg 59E) or used as the neighbourhood portion in areas without Parish Councils (Reg 59F). Summary details should be provided of the items of infrastructure that these have receipts been allocated to or spent on and the amount on each item. |

|

Summary details of notices served in the recovery of CIL (Reg 59E) including:

|

|

Excluding the neighbourhood portion (Reg 59E and 59F) the total amount of:

|

|

For the neighbourhood portion (Reg 59E and 59F) the total amount of:

|

| Matters that must be included in the Section 106 report | |

|---|---|

| Total amount of money secured through S106 during the reported year | |

| Total amount of money received through S106 during the reported year | |

| Total amount of S106 receipts collected before the reported year but which have not been allocated | |

| Total amount of S106 expenditure for the reported year (including transferring it to another person to spend) | |

|

In relation to S106 expenditure for the reported year summary details of:

|

|

| Total amount of S106 receipts which were allocated but not spent in the reported year for funding infrastructure and summary details of the items of infrastructure and the amount of money allocated to each item. | |

| Total amount of S106 received during any year which was retained at the end of the reported year for the purposes of longer-term maintenance (commuted sums). | |

|

Summary of non-monetary contributions secured during the reported year including:

|

| Matters encouraged to be in the IFS |

|---|

| Report on the delivery and provision of infrastructure |

| Estimated future income |

| Infrastructure projects or types of infrastructure that the authority intends to fund, either wholly or partly, by the levy and / or planning S106 obligations |

| Future spending priorities on infrastructure and affordable housing in line with up-to-date or emerging local plan policies |

| A written narrative in respect of the above to demonstrate how developer contributions will be used to deliver relevant strategic policies in the local plan, including infrastructure projects or types of infrastructure that will be delivered, when and where |

| To be used as a wider engagement tool and promotional tool |

| To be published with updated data and more frequently than the 31st December annual deadline |

| Matters encouraged to be included in the S106 report |

| Summary details of any funding or provision of infrastructure to be provided through a S278 highways agreement that has been secured during the reported year |

| Summary details of any funding or provision of infrastructure to be provided through a S278 highways agreement that has been received during the reported year |

Annex 2 - Sample IFS Template