The Care and Health Improvement Programme (CHIP) has published this information and user guide to accompany its dynamic Microsoft Excel tool – the Homecare Cost of Care Toolkit.

Glossary

Below, you will find an alphabetical list of terms alongside the definitions of them which have been used for the purposes of this publication:

care worker / carer

given the exact same meaning in this document and refer to the people that are employed by the provider to directly deliver care and support (the term ‘care worker’ is used most commonly throughout the document with occasional uses of the term ‘carer’)

costs – fixed

costs incurred by the provider regardless of the volume of care they deliver, including operational overheads such as rent, insurance, and so on

costs – variable

costs incurred by the provider which vary according to the volume of care they deliver, including care workers' direct contact pay, personal protective equipment (PPE) costs, training, sick pay and holiday pay

cost – unit

figure that includes all costs incurred in delivering a unit of care plus a figure for profit / surplus

commissioner

collective term referring to an organisation which commissions (or teams and individuals within that organisation which commission) homecare and support (in most cases, the commissioner will be a council, but it may also be a health organisation)

period

much of the information that needs to populated will relate to a specific time period, typically a financial year (the important factor is that the period chosen is agreed upon by commissioners and providers and is correctly used within the tool)

price / fee / rate

figure the commissioner pays a care provider for the delivery of a unit of care (this may be informed by the completion of the toolkit but will also be based on other information and local circumstances)

provider

collective term referring to an organisation that delivers homecare and support

service user / client / person receiving care and support

person who receives homecare and support delivered by the provider (these terms all have exactly the same meaning)

travel

journey (and associated time, distance and related costs) between two fixed points; typically, the homes of two people in receipt of care and support

user

person who inputs information into the toolkit

1.1. Background to the Homecare Cost of Care Toolkit

The Care and Health Improvement Programme (CHIP) – jointly delivered through the Association of Directors of Adult Social Care (ADASS) and the Local Government Association (LGA) – commissioned ARCC-HR Ltd, in April 2021, to develop and deliver the Homecare Cost of Care Toolkit.

It is recognised that setting an appropriate price for care is made challenging without a robust and accurate approach, agreed between commissioners and providers to establishing the costs involved in delivering care. With the Homecare Cost of Care Toolkit and this accompanying guidance, we aim to support commissioners and providers undertaking cost of care work, without mandating or specifying the exact focus, criteria or requirements.

The intended purpose of the toolkit is to support improvements in the level and quality of information about the costs of delivering home-based care and support. The expected benefits are:

- supporting commissioners and providers to obtain a shared understanding of actual costs of delivering homecare in the local area

- supporting commissioners understanding of the complexities inherent in the homecare market in relation to the way care providers operate, their structure and the costs associated with providing care – this is expected to inform and support fee-setting exercises, market viability and market-shaping

- enabling commissioners and providers to access, free of charge, information that accurately deals with all factors that influence providers costs, including volume

- recognising existing and potential future legislative requirements.

The main purpose of this document is to guide commissioners and providers on how to practically use the Homecare Cost of Care Toolkit.

1.2. Toolkit structure and functionality

The Homecare Cost of Care Toolkit is constructed in three parts:

Part A – Standard (Cost+) Worksheet

Part A of the toolkit – the Standard (Cost+) Worksheet – utilises a traditional unit costing approach and will help users understand the individual operating costs and variances that make up the cost of homecare, whilst adding additional flexibility and costs that may not usually be considered. The toolkit includes, as far as practical, all expected cost lines that homecare providers incur in delivering services. While additional cost lines may exist within individual homecare providers, feedback from extensive engagement with stakeholders, including care providers, has arrived at those that are included in the toolkit. This part of the toolkit also includes additional blank lines to allow the user to add cost lines that are not already included but should be factored into any cost of care exercise.

Overview of Part A – Standard (Cost+) Worksheet

- Unit price

- Profit / surplus

- Business overheads

- Other wage-related on-costs

- Direct care and related staff costs (related to the delivery of core hours)

- Core hours / volume

Part B – Sensitivity Analysis Worksheet

Part B of the toolkit – the Sensitivity Analysis Worksheet – can be used to generate 'what if' scenarios to see, at-a-glance, the impact of changing costs, volumes and price points on the profitability of the provider / branch / market as a whole. It utilises the cost of care information populated in Part A, alongside an easy-to-use slider interface. This can be used to ‘scenario-test’ various changes to current commissioning arrangements (for example, volume of care delivered) and provider circumstances (for example, rate paid to care workers) to see the impact the change has on provider sustainability. There are many uses for this, for instance, a commissioner could easily establish the rate they would have to pay a provider for that provider to then pay their staff a specific hourly rate.

Part C – Data Output Worksheet

Where information is correctly input into the toolkit, a unit cost figure will be produced that accurately reflects the relationships between the various data fields and the reality of how homecare is commissioning and provided. This is only possible because of the structure of the toolkit and the formulae within it. These have been locked to ensure they remain robust and accurate and cannot be amended in any way that could undermine the toolkit.

It is recognised that users may want to use the information in the toolkit in different ways and, for this reason, Part C – the Data Output Worksheet – has been created. This worksheet will automatically be populated with key information from Part A – the Standard (Cost+) Worksheet. Unlike the Standard (Cost+) Worksheet (Part A), the Data Output Worksheet (Part C), and the information within it, can be amended and copied and pasted elsewhere to allow for further analysis.

1.3. Calculating a unit rate per care hour

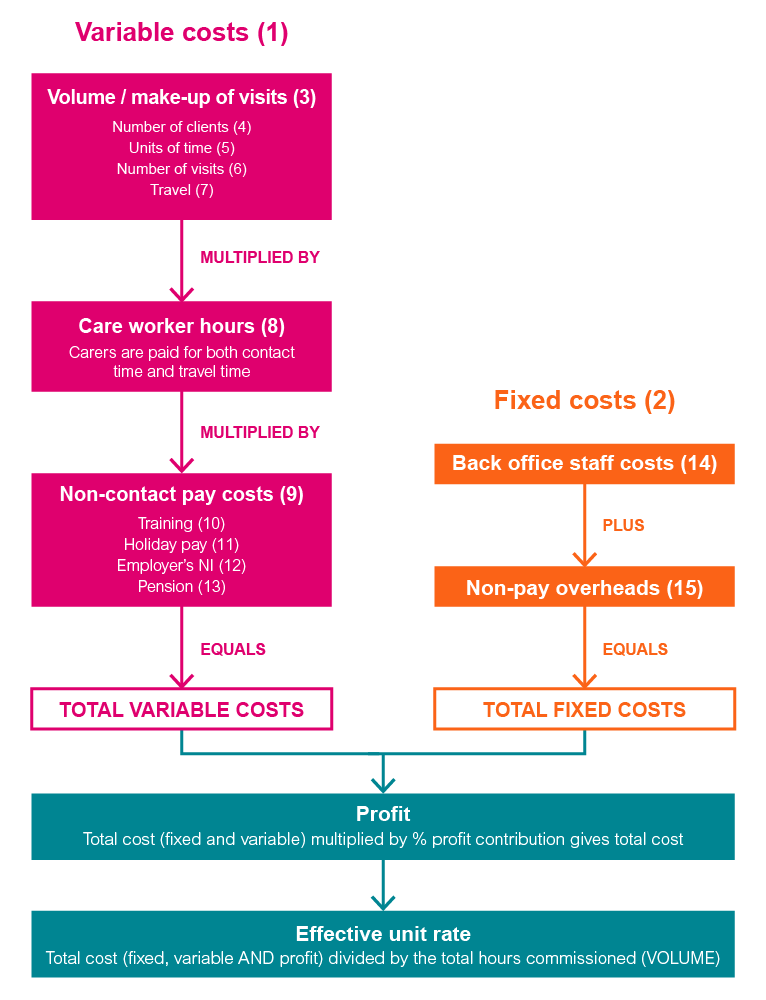

To calculate a unit rate per care hour, the toolkit takes user input values to calculate both fixed and variable costs. Figure 3 below provides an overview of the high-level workflow and calculations in the toolkit, and the below annotates the key elements contained within it. Please note all calculations where annualised amounts are required assumes a 52-week year and that Profit / surplus / contribution is a mark-up percentage of the total costs.

- For the purposes of the toolkit, variable costs refer to those costs aligned to the volume of business a provider is delivering, such as carer direct contact pay and travel, and carer non-contact-related costs, that is, training, sick pay, maternity / paternity, holiday. These are multiplied by the volume of care time (hours) commissioned per annum.

- For the purposes of the toolkit, fixed costs remain relatively constant costs which are incurred irrespective of the volume of care delivered (unit of time / visit length). These include back-office staff and operational overheads such as premises, insurance, consumables, and so on. It is important to note that homecare branches will have a ceiling number of hours before additional back-office costs increase. Fixed costs are divided by the total care time (hours) commissioned, and are annualised for the purposes of cost calculation.

- Volume and make-up of visits – please note, personal protective equipment (PPE) costs are calculated using the proportion of visits requiring PPE and the number of uses of each item.

- The average number of clients per annum is used to calculate Care Quality Commission (CQC) fees. These are broken down to consider units of time, number of visits and travel (see below).

- Units of time – the weighted average visit length is considered in the hourly unit rate.

- Number of visits informs the volume / instances of travel.

- Travel – time (staff) and distance (expenses) accrued on all visits.

- Care worker hours – carers are paid for both contact time and travel time. Hourly pay rates for contact time and travel can vary depending on both a) the type of staff delivering care and b) care delivered at enhanced rates.

- Non-contact pay costs – carers are paid the same rate as the above for all non-contact-related time (that is, sick pay, holiday, training, and so on), excluding where enhancements are paid for contact and travel time.

- Training is accrued at 7.5 hours multiplied by the number of days for each staff member, regardless of average full-time equivalent (FTE) of staff.

- Holiday pay is accrued on all working time (contact, travel, training, sick, additional non-contact pay costs).

- Employer's NI cost is accrued on all working time at the statutory rates, and varies according to the statutory pay thresholds based on average weekly hours per worker.

- Pension contributions are accrued on all working time.

- Back office staff costs – the toolkit takes user input values for staff roles and pay.

- Non-pay overheads – apart from the Care Quality Commission (CQC) fee calculation, which is derived from the average number of clients, all other overheads are user input values. All costs are annualised for the purposes of cost calculation.

1.4. Top tips

There are some key factors to consider in relation to how the toolkit and overall cost of care process can be used most effectively in a local area:

1.4.1. How should the toolkit be populated?

The Homecare Cost of Care Toolkit can be used in a variety of ways and it is clear from discussions with commissioners and providers during the testing phase that there will be a wide range of uses and applications of the toolkit which will influence how it is populated and the exact role of those involved in any process. Therefore, there is no set answer for who should complete the toolkit (that is, the user) and how this should be done. This section describes two main types of scenarios where the toolkit could be used and aims to support commissioners and providers agree an approach that works best for them. These suggestions are not directive or prescriptive.

Example use scenario 1

Commissioners and providers agree to use the toolkit to establish the actual costs incurred by local care providers operating under a specific contract. This could be done to create a baseline of actual costs to support future commissioning or fee arrangements, or to plan for a specific change.

Who provides the information? Under this type of scenario providers are likely to have all of the information required, whereas the commissioner is only expected to have access to some of it (for example, number of commissioned visits). Therefore, the information is likely to come from providers.

Who populates the toolkit? Depending on the local approach, as provider/s are likely to have the information required to populate the toolkit for use in this way it seems most appropriate that they will complete the toolkit. This may be done as part of a process that involves a group of providers agreeing to populate the toolkit and submitting their returns to the council who will collate these to get an overall view of costs.

Example use scenario 2

Who provides the information? Under this type of scenario, the commissioner may understand be able to predict volumes, types of visits, number of people to be supported, travel time and distance and have expectations about staff pay rates and shift structures, and so on. They could use this information in the toolkit to get an indication of the costs a provider is likely to incur in delivering such a service. This will only map a hypothetical scenario, not give precise figures so this approach is likely to be more effective and accurate if providers play a strong role in this work. This is because some of the information would not be known to a commissioner (for example, back-office costs) and to ensure planning for this service reflects the reality of organisational structures and service delivery.

Who populates the toolkit? Under this scenario the commissioner is likely to be the user and populate the toolkit, though this process is expected to benefit from provider information and involvement.

1.4.2. How should the toolkit be used as part of a wider cost of care processes?

When considering how the toolkit can be used most effectively in a local area, commissioners and providers are encouraged to consider the following:

- Importance of transparency, joint-working and a shared understanding on key issues – Commissioners and providers are strongly encouraged to work together to agree how the cost of care process should operate and the specific use of the Homecare Cost of Care Toolkit. Their considerations should include, but not be limited to:

- provider involvement – deciding how providers will be invited to be involved in this process and how all parties can ensure the process is representative of the local sector – they may involve agreeing an ideal / minimum number of providers and what to do if too few / many providers wish to be involved

- timescales – agreeing realistic timescales for the collection of data, reviewing and verifying information, aggregation and analysis of results and making and implementing any subsequent decisions – timescales should accept the likelihood that at times the provider may need to prioritise operational matters over their role in this exercise

- information sharing – agree what information will be shared during and after this exercise with the providers that are involved and have shared information and those that haven’t but deliver homecare on behalf of the council – this is likely to take the form of an aggregated analysis to safeguard the confidentiality of sensitive information

- purpose and use of information – agreeing how information obtained during this exercise will be used during the exercise and then after the exercise is complete to inform decision-making. (On the first point, providers should have regular opportunities throughout the process to check their information is being used and interpreted correctly. On the second point, commissioners and providers are advised to work together to agree the scope and priorities for the exercise and reach a reasonable position on what commitments can and can’t be made for how the results of the exercise will be used. For instance, it may be agreed that this exercise will inform a decision on if differential fee rates are applied for rural and urban visits, but the commissioner could not be expected to commit to a specific decision or action – for example, to increase a fee rate by x per cent – before the exercise is completed and information analysed.)

- Accuracy and completeness of information – the more accurate, up-to-date, and complete the information used to populate the toolkit, the more accurate the cost figures will be. It is recognised this may not be possible for all cost lines and commissioners and providers are encouraged to identify any such issues and agree how to deal with them, before any exercise begins. The resolution may be to use an approximate figure, use a standard figure for all providers or leave a line blank.

- Wider benefits and requirements in relation to cost of care information and processes – a strong message from commissioners and providers during the testing of the Homecare Cost of Care Toolkit was that, if done well, the use of the toolkit and wider cost of care work can bring great benefits to the local area. However, there is the potential that the time and effort it takes to complete could exceed the benefits it delivers. For this reason, it is suggested that in their planning of this work, commissioners and providers carefully consider:

- the purpose and focus of the cost of care exercise – (The common feedback from those who have previously been involved in cost of care work is that broad and significant benefits can be achieved beyond arriving at a unit cost figure. These include improving relationships, getting a better understanding of the links between commissioning and costs and informing changes that improve provider sustainability and help people live more independently in their own home. Those involved in cost of care exercises and who use the Homecare Cost of Care Toolkit are encouraged to consider how they can add the greatest and broadest value, but also be clear on the focus of the work they are undertaking.)

- requirements of cost of care exercises – (At the time at which the Homecare Cost of Care Toolkit was launched, in early 2022, there is a wider national context around costs of care, fair price for care, provider viability but little detail around specific national requirements. Those planning to use the toolkit are strongly encouraged to consider how they can ‘future-proof’ their approach to meet any future requirements and minimise any time and effort needed to repeat, change or adapt any part of the exercise. Using the example of how many providers should be involved in a cost of care exercise or what constitutes an appropriate representation of providers, to future-proof this exercise commissioners and provider associations could jointly invite and encourage providers to participate and formally agree that the group of providers involved are representative. The commissioner could also document all communication and agreements, so they are well placed to demonstrate they; a) were transparent in how they invited providers to be involved and b) agreed those involved were representative of the sector.)

1.4.3. Exclusions

The Homecare Cost of Care Toolkit will not / should not:

- be expected to give a precise cost, especially where information is inaccurate or missing – the toolkit will deal accurately and appropriately with the information used to populate it and will provide a robust basis for understanding and considering costs. However, there are a few factors to be considered:

- Even where toolkit is completed with full and accurate information, there are likely to be some figures that are approximate. For instance, providers are not expected to record or check actual PPE usage for every single visit but are likely to consider the various types of visits that have different levels of PPE usage and then estimate the proportion of visits of each type. Given PPE costs will be around two to three per cent of overall costs, this is felt to be a proportionate approach and testing of the toolkit indicates that the impact of any approximation for this and other costs will have a minimal impact on the overall situation.

- If various providers are involved in this exercise, they are likely to populate the toolkit slightly differently (for example, include different information in each cost line). This should not affect the overall accuracy of the toolkit, but caution should be applied when comparing certain cost lines, especially where information from different providers is aggregated.

- be used to aggregate costs of providers that fundamentally differ in what they are commissioned to provide – the Homecare Cost of Care Toolkit has been designed to be used and populated in various ways. However, where the cost bases and approaches of providers or services are fundamentally different, this should be considered when deciding how to use the toolkit. As an example, assume two different services are commissioned by the same organisation. One service involves commissioning and paying for the delivery of individual visits of 30 minutes, 45 minutes and 60 minutes and the second is a rapid response service where staff are paid to be on shifts rather than for the individual care they deliver. The toolkit can be used in both cases, but the services / providers will have such different cost bases that it would not be appropriate to aggregate all results to obtain a single cost figure. It would be preferable to treat the two services and sets of information separately and use this exercise to establish a cost base for each service.

- be used to understand, but not to judge, how providers operate – as with any sector, homecare providers differ in their size, structure and volume of support provided and their cost base will reflect these differences. A cost of care exercise is likely to further all parties understanding of how providers operate, where any differences exist and the reasons for them. It may be that the exercise also highlights practice that all parties would want to eradicate or improve, and examples could include low levels of management supervision, call cramming and invoice financing. This could be a very useful output from such an exercise and is not about judging a provider, but about understanding what is happening, what challenges have caused this and what can be done collectively to address the situation.

- tell anyone what fee rates should be or what decisions should be made – it is recognised that the commissioning and provision of care and support for people living in their own home is complex. Therefore, any decision made about the commissioning, payment, or delivery of such provision will need to consider various factors. It is important to recognise this is an intelligence toolkit, not a decision-making toolkit. Where commissioners and providers use the Homecare Cost of Care Toolkit effectively it should provide valuable insight that can be used alongside other intelligence to inform future decision-making. As a specific example of this, it should not be assumed that a commissioner will or must pay providers at a rate that is solely based on the outcome of this exercise.

2. Homecare Cost of Care Toolkit user guide

In the sections below you will find the full Homecare Cost of Care Toolkit user guide.

End User License Agreement (EULA)

The Homecare Cost of Care Toolkit can only be used once it has been downloaded. Before downloading, each user is required to review and accept the EULA. Once downloaded, three further worksheets are displayed in the tabs at the bottom of the document – these are:

- Part A – Standard (Cost+) Worksheet

- Part B – Sensitivity Analysis Worksheet

- Part C – Data Output Worksheet.

These three parts are also known as Part I, Part II and Part III. The information in parts B and C is taken directly from Part A and so can only be used once Part A has been completed. Therefore, you should begin by completing Part A.

By using the toolkit, you are agreeing to the terms and conditions within the End User License Agreement (EULA).

The following section describes the functions and inputs required to produce accurate results and should be read alongside the toolkit.

Part A: Standard (Cost+) Worksheet

Part A – the Standard (Cost+) Worksheet is used to input volumes, standard business costs and generate a unit price per hour of homecare. The information added to Part A will automatically pull through into Part B.

User key and sections

A key is provided in Part A – the Standard (Cost+) worksheet to direct users to different types of input and cells with commentary, as shown below.

Each section is made up of tables containing cells that require user entry as well as calculated values and summary totals. Sections are headed with the type of information required, alongside commentary in grey text to describe the inputs and calculations performed in the section.

User input cells (red text with an orange background) will display a comment box next to them when clicked, other cells bordered in red open a comment when the user hovers over these cells, as pictured below.

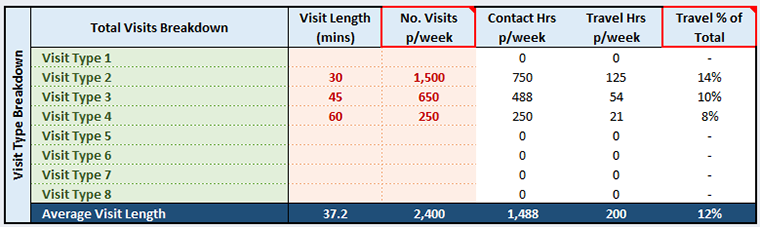

(A) Care hours and visits breakdown

This section seeks to establish the different types of visits undertaken and specifically, the amount of face-to-face contact time involved in each different type of visit and the overall visits and contact hours per week.

What needs to be input?

The table allows input for up to eight visit types to determine the total volume of contact (face-to-face) hours for the branch, provider or market being modelled. Visit types can represent different visit lengths and can be categorised manually by entering free text in the ‘visit type’ cells in green (for example, to specify visit types such as local authority, self-funded, continuing healthcare (CHC), short breaks, sit-in services or awake nights). If you wish to establish different unit costs for different visit types, then you may complete a separate worksheet for each volume of activity (see the note in the 'User key and sections' section above).

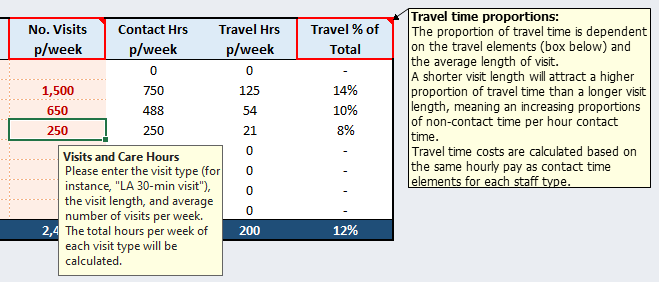

The values in the column contact hours per week are calculated by the visit length multiplied by the number of visits per week. Users should check the output in the ‘contact hours per week’ section to ensure that this reflects the expected figure.

Travel percentage of total = travel time / (contact time + travel time)

Examples:

(a) 38 minutes = 8 [travel] / 30 [contact] + 8 [travel] = 21 per cent

(b) 68 minutes = 8 [travel] / 60 [contact] + 8 [travel] = 12 per cent

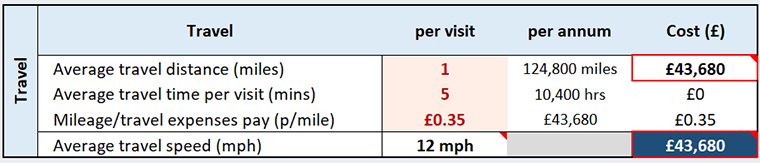

(B) Travel time and mileage expenses

What needs to be input?

Travel costs are calculated using the total number of visits and mileage associated with each visit enter the average travel time per visit (in minutes) and the average travel distance (miles) per visit, based on the annualised number of visits delivered above in Section A. Then enter the mileage / travel expenses pay (per mile) attached to each visit.

The table calculates the total hours of travel time accrued based on the annualised visits and the total annual mileage cost. These figures are also expressed as travel hours per week in the table in Section A.

Total travel costs are then calculated as follows:

- worker pay travel costs for all visits = (minutes per visit x total visits / 60) x weighted hourly pay rate

- total mileage costs = (average miles per visit x total visits) x mileage pay p/mile

- total travel costs = worker pay travel costs (1) + total mileage costs (2).

Please note that the toolkit requires an average travel distance and time for all visits, and therefore the user’s input must represent weighted average figures for the breakdown of visits entered in 2.2.2 above. If the user wishes to apply different travel distances and times to proportions of visits, then use separate worksheets to calculate the unit costs for these. This may be desirable if the user wishes to produce an output showing varying travel times and visits between geographies (for example, rural versus urban). As you will see from the picture above, some figures will remain blank or show £0 until further information is provided later in the tool.

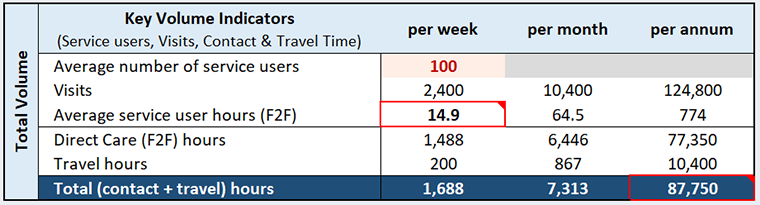

(C) Branch and volume summary

The below table calculates the total annual hours of direct care (contact) and travel accrued based on Sections A and B above.

What needs to be input?

Users must enter the average number of service users per week, based on the information populated in the ‘total visits breakdown’ section.

The number of service users in this table is also used to calculate Care Quality Commission (CQC) fees in the toolkit (described as an overhead cost in section J below), as fees are based on the number of branches and service users. Therefore, the number of service users should be accurate to those expected to be charged for within the annual period.

For more information on how the number of service users is arrived at for the purposes of CQC fee calculation, please see the CQC guidance document here (sections 40 to 44 on pages 16 and 17).

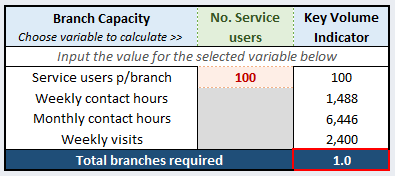

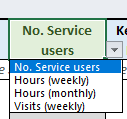

Branch calculator

Where the user is utilising the toolkit to assess the entire market (that is, the totality of services commissioned) to calculate the number of branches required users must select the variable you wish to use for the maximum branch capacity. The values in the Care Quality Commission's (CQC's) regulatory fees guidance are used as the divisor (or multiplier) for the care volumes entered in section A and will scale up any fixed costs (see overheads sections H to J below) accordingly. The table shows the total branches required, based on the division of the volumes entered in the rest of the worksheet.

The variable used to set the size of the branch can be changed by using the drop-down box (cell highlighted with green text), as shown below.

(D) Personal protective equipment (PPE)

This section calculates the actual costs of PPE based on the unit cost at which PPE is purchased, the usage and frequency of PPE against the annual number of visits calculated in Section A.

What needs to be input?

For each type of PPE, the provider should state the cost per unit, items required per visit (that is, on average how many PPE items are used per visit) and percentage PPE calls (that is, the proportion of all visits annually where PPE is required). If one instance of PPE is required for every visit, the number of uses = 1. If more than one set of PPE is required, then number of uses = 2.

Users are not required to establish the exact PPE use for each visit undertaken. Instead, users should consider the average PPE items across all visits and use their judgement to decide what PPE figures are used to populate the tool. For example, if the provider estimates that a third of their visits require no PPE usage, a third require a full set of PPE and a third may require two full sets of PPE, then they would populate the ‘items required per visit’ column with '1' for each item.

Where cost information for PPE or other consumables cannot be calculated per visit, such as hand sanitiser, these may be included in Overheads (section J) instead of in the above table. It is recommended that where available, PPE costs are covered as above.

(E) Direct pay rate card and costs

This section contains the pay rates for workforce involved in direct care delivery.

What needs to be input?

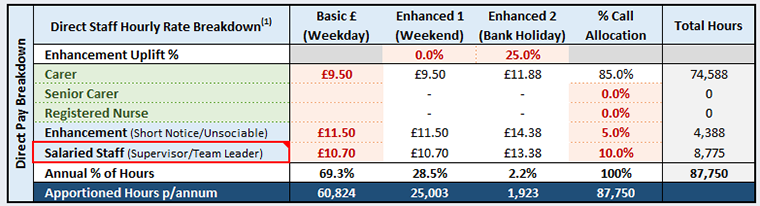

Pay should be input as an hourly rate. By default, the table allows the user to input varying pay rates based on the following worker types: care worker, senior care worker, registered nurse, enhanced/short notice/unsociable hours and salaried (team leader / supervisory) staff. Enter a basic (weekday) rate for each worker type that you wish to represent in the toolkit. There are two variables that ensure accurate costing of all hours to be delivered in the toolkit.

The volume of hours used for calculation in this section include contact and travel hours, not just face-to-face hours. This ensures that workers are calculated as being paid at the same rate for any travel hours, and to comply with Her Majesty's Revenue and Customs (HMRC) National Minimum Wage pay requirements.

1. Enhancements

There are two additional types of enhancements (supplementary to the short notice / unsociable hours row under worker types) that can be added, these represent weekend and bank holiday hours. The proportion of hours delivered that fall into either of the enhanced pay categories will attract that rate instead of the basic rate. The user may enter the 'enhancement uplift' percentage they wish to apply for each enhancement type. In the example in the note below, for basic rate for a care worker on a bank holiday, they are paid at an enhanced rate of £11.14 instead of £8.91 (due to the 25 per cent uplift being applied to the pay rate).

2. Percentage of call allocation

In order for the toolkit to calculate the correct rates and enhancements for contact and travel hours, the user may input the proportion of all hours that are delivered by each level of staff member. This is entered as a percentage of call allocation and represents the percentage of total hours delivered. In the example from the table above, five per cent of all hours are delivered at an enhanced (short notice) worker rate, and 10 per cent are delivered by a team leader. The remaining volume (85 per cent) is delivered at the care workers' rate.

The total direct pay costs are multiplied by the number of care and travel hours per annum (section C) delivered by each type of staff member at the relevant proportion of enhanced hours. The weighted basic hourly rate (against the allocation of direct hours delivered by each staff type) excluding any enhanced rates are used for non-contact related pay costs in section F.

The table below multiplies the rate card by the proportion of hours delivered by the relevant worker at each rate, to give a total pay cost for contact and travel costs (see illustrative example costs in the table below).

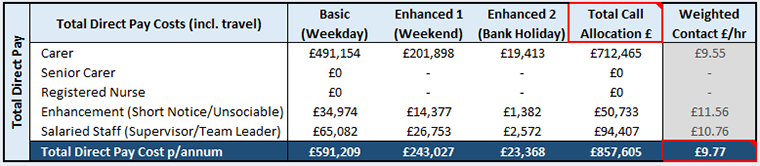

In the example above, total travel and contact pay costs of £857,605 have been calculated using the values entered in the ‘direct staff hourly rate breakdown’ and calculated as follows (rates rounded to nearest whole number):

(a) Care worker

- 97.8 per cent of 74,588 hrs at basic (weekday/weekend) rate of £9.50 = 72,948 hours x 9.50 = £693,006

- 2.2 per cent of 74,588 hrs at enhanced (bank holiday) rate of £11.88 = 1,640 hours x 11.88 = £19,413

(b) Short notice

- 97.8 per cent of 4,388 hrs at basic (weekday/weekend) rate of £11.50 = 4,291 hours x 11.50 = £49,351

- 2.2 per cent of 4,388 hrs at enhanced (bank holiday) rate of £14.38 = 96.5 hours x 14.38 = £1,382

(c) Team leader

- 97.8 per cent of 8,775 hrs at basic (weekday/weekend) rate of £10.70 = 8,582 hours x 10.70 = £91,835

- 2.2 per cent of 8,775 hrs at enhanced (bank holiday) rate of £13.38 = 193 hours x 13.38 = £2,583

The ‘weighted contact £/hr’ is then represented as the total weighted average rate, calculated as follows:

total weighted average rate = annual contact and travel pay (a + b + c) = £857,605 = £9.77 per hour

(F) Non-contact-related pay costs

What needs to be input?

Users must enter the percentage of total hours expected for each non-contact activity to be costed in the toolkit. Non-contact related pay costs include costs that are incurred and paid to workers that do not relate to direct care delivery, this includes holiday pay, sick pay, suspension pay, maternity / paternity and additional non-contact pay costs.

The total number of hours for each non-contact activity is calculated as a percentage on top of the hours calculated in section E above. Users must enter the proportion (per cent) of contact and travel hours for each non-contact pay line (see worked example below). The toolkit then multiplies the non-contact pay hours per annum by the weighted basic hourly rate to calculate total direct workforce hours.

a. For suspension, maternity/paternity, and additional non-contact pay, this is calculated as a percentage of annualised contact and travel hours.

b. Holiday pay is calculated as a percentage of all contact & travel time plus non-contact related pay costs.

c. Enter the number of full-time equivalent (FTE) training and supervision days per worker / direct care staff per annum.

Additional non-contact costs could include uplifts for paying shifts (that is, 30 minutes' break for every 7.5 hours of working time may be expressed as 6.7 per cent = 0.5 / 7.5); or any additional costs attributed to hourly agency costs.

The below table calculates all on-costs based on the total hours required, the blended hourly rate in section E and the total staff in section G (below).

Sick Pay = 1.5% of 10,000 hrs = 150 Suspension Pay = 0.4% of 10,000 hrs = 40 Maternity/Paternity Pay = 1.5% of 10,000 hrs = 150 Holiday Pay = 12.07% of 10,000 + 150 + 40 + 150 hrs = 1,248 Total hours non-contact pay hours = 1,588

Total cost for non-contact pay hours = 1,588 x weighted basic hourly rate (£9.50) = £15,086

Training and supervision costs are calculated as the number of FTE days (at 7.5 hours per day) per year required for each staff member. For this calculation to function, the total number of care staff is required. For a cohort of 20 staff member to receive 6 days training and supervision per year, the total number of hours to pay is expressed as 6 days x 7.5 hours x 20 staff = 900 hours per annum.

Users should consider how many training sessions are required per year, and the mandatory vs. non-mandatory training requirements for each member of staff (depending on the types of customers and care provision delivered).

There may be other non-contact pay costs that a provider could incur. If this is the case, the user should populate this section in the way that is felt to be most appropriate and that most accurately reflects the cost incurred. As an example, a staff member takes compassionate leave and this results in an additional cost to a provider. The nature of the situation and the costs may mean it is most appropriate to include this cost in the ‘sick pay’ column.

Please note that non-contact pay costs in this section of the toolkit relate to those staff delivering direct care. Non-contact pay costs for back-office staff are included within section H below, under salaried FTE costs.

(G) Direct staffing costs, employer’s National Insurance and pension on-costs

What needs to be input?

Users must enter the total care staff per annum required to deliver all working hours related to contact and non-contact pay delivery in order to calculate employer’s National Insurance and pension costs.

Employer’s National Insurance

Employer’s National Insurance (ENI) is accrued on working hours per staff member over and above the legislated ENI threshold per annum. To calculate this, in addition to the total care staff per annum, the user must input the employer’s National Insurance threshold £ (annual pay cap) above which ENI is accrued, and the ENI liability percentage (the percentage at which ENI is accrued above the threshold). Both figures are available via the gov.uk website, which for 2021/22 equates to earnings of £8,844 per person per annum and a 13.8 per cent of income above this rate.

The example above shows, for a staff base of 75 people working an average 26.8 hours per week (at the equivalent annualised pay cost of £13,577), 9.3 hours of work per staff member per week accrues ENI at 15.05 per cent. The total pay cost shown below (to which ENI is applied) is £355,003, resulting in ENI costs of £53,428.

Pension contributions

Users must enter the pension percentage. Employer’s pension contributions are accrued on all working hours unless a staff opt-out percentage is applied. The user-input pension percentage is applied as a proportion of all working hours multiplied by the average pay cost as shown in the example below.

There is a drop-down box in the table above next to 'Use for back-office pension %?' (highlighted in green text). Selecting ‘yes’ will apply the pension percentage entered here to all back-office staff in section H below. Selecting ‘no’ will allow the user to manually enter pension percentage for each staff role / function in section H.

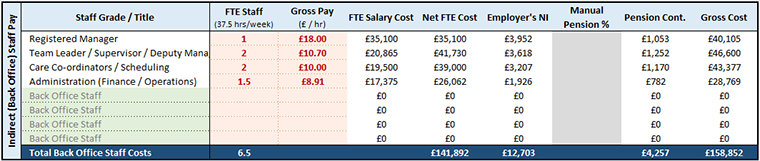

(H) Back office pay costs (overheads)

The table calculates the total pay costs (including Employer's National Insurance and pension on-costs) for the back office, using the on-costs information in section G above.

What needs to be input?

Users must enter the staff required at each grade / job function for back-office functions. Where salaried staff have been identified in section E, enter only the apportionment of staff for back-office FTE / functions below. This is expressed as the number of FTE staff and the gross pay per hour (calculated as FTE at 37.5 hrs per week).

The annualised FTE salary cost is calculated in the column next to the 'gross pay (£ / hr)' column. Refer to this column if you are entering gross hourly pay costs and need to check the total FTE salary cost paid to the staff member.

If you selected ‘no’ to using the pension percentage in section G, you can enter the percentage for pension manually for each staff role in the table below. Use the additional rows (in green) to enter extra staff roles as needed.

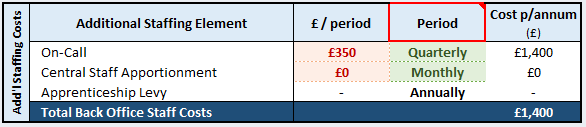

(I) Additional back office pay costs

What needs to be input?

Users must enter any additional pay-related costs. These are any costs that relate to staff pay that do not fit into the above categories. This may include costs for on-call staff of central staff apportionment (for multi-branch, regional or national providers), which may be expressed as a fixed cost applied to the provider or branch for the area being costed.

Enter the £ / period and select the period cost this relates to using the drop down in the green highlighted boxes. The periods to choose from are weekly, four-weekly, monthly, quarterly and annually. The total costs are annualised in the right-hand column.

Apprenticeship Levy can also be calculated automatically based on the pay bill threshold and percentage of levy amount in the 'setup' boxes (described below). If Apprenticeship Levy is charged centrally, include any branch apportionments in 'central staff apportionment' – described below.

(J) Non-pay costs (overheads)

What needs to be input?

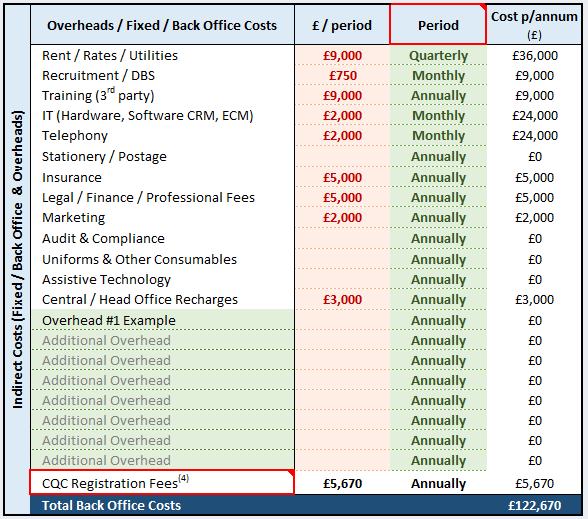

Users must enter the cost of non-pay overheads and select the period (weekly, four-weekly, monthly, quarterly, or annually) from the drop-down boxes. Ensure the costs are entered excluding VAT (if a VAT-registered business). Use the 'additional overhead' rows as required. The table calculates the total annualised non-pay overhead cost per branch. Costs should be input utilising reported actual costs for the selected period.

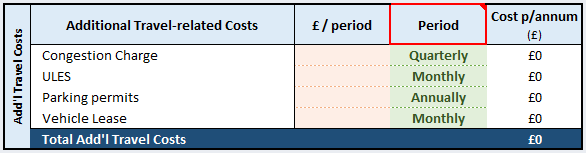

Additional travel-related costs can be captured in the table above. This may include ad-hoc travel costs such as congestion charges, parking permits and schemes such as ultra low emission zones (ULEZ), or vehicle lease costs.

Other overheads are illustrated in the table below. Care Quality Commission (CQC) registration fees at the bottom of this table are calculated using the number of service users entered in section C above. There is a CQC fee calculator in the ‘setup’ boxes section (see guidance section below).

While the toolkit cannot specify every overhead cost that may be incurred for all businesses, the below lists have been developed to illustrate the cost areas and what may be considered when completing this section.

Rents / rates / utilities

- office rents

- any office maintenance, cleaning, and so on

- business rates

- utilities – gas, electric, water, waste management

Recruitment / Disclosure and Barring Service (DBS)

- advertising costs

- pre-onboarding induction (where not included in training costs)

Training (third party costs)

- costs for courses, materials, certification

- external trainers, venue hire

IT

- hardware

- software and licenses

- applications such as electronic care management (ECM)

- technical support

Telephony

- line rental and call charges

Stationary/Postage

- office consumables

Insurance

- employees insurance

- public liability

- professional indemnity

- cyber security (if applicable)

Legal / finance / professional fees

- accountancy fees

- legal fees

- other professional services

Marketing

- advertising and conferences

- marketing flyers, banners and other materials

Audit and compliance

- external compliance costs, that is, mock inspections

- document storage costs

Central / head office recharges

- franchisee fees

- return on capital / loan / interest costs not included in 'earnings before interest, taxes, depreciation, and amortization' (EBITDA)

- annualised capital costs

Uniform / other consumables

- other personal protective equipment (PPE)-related costs not included in the above section

- storage costs

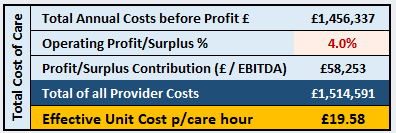

(K) Operating surplus and unit cost

What needs to be input?

Users must enter the 'operating profit / surplus percentage' to represent the percentage margin or business operating surplus (profit). The profit / surplus contribution is expressed as 'earnings before interest, taxes, depreciation, and amortization' (EBITDA) and before any operating dividends or shareholder returns.

This excludes any capital costs, depreciation, contribution to central overheads or shareholder returns already costed in section I above.

The profit contribution may include business specific figures that could include; retained profit, return on capital to shareholders, interest costs, invoice financing and central profit margins.

The effective unit costs per care hour (in the table above) takes all annualised provider costs and operating profit (surplus), and divides this by the total number of face-to-face care hours specified in section A.

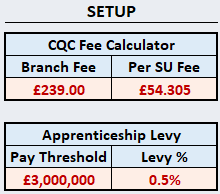

Setup table

The boxes in the setup table (located next to the overheads table in section J) provides extra functionality in adjusting the rates applied for CQC fees and the Apprenticeship Levy based on any future price or legislative changes.

For Care Quality Commission (CQC) fees, the ‘branch fee’ and ‘per setup (SU) fee’ can be amended to reflect any changes in fee rates across years.

The Apprenticeship Levy calculates any costs above the pay threshold and applies the levy percentage rate as a total cost (annualised £) in Section I. These rates can be adjusted as required.

Part B: Sensitivity Analysis Worksheet

This can be used to vary individual cost lines using a ‘slider’ interface.

The Sensitivity Analysis Worksheet provides an extra level of functionality and allows users to adjust several key cost and volume indicators, without affecting the values in the Standard (Cost+) Worksheet. There are many use cases where adjusting costs in this manner may be beneficial. Below are just some examples of where a simple analysis may help in identifying cost impacts for certain changes:

- consider in-year changes to costs (for example, changes in hours delivered, Real Living Wage rates, number of staff, PPE, Insurance or other costs)

- model unit costs based on different geographies / rurality (for example, changing travel time and mileage for different areas)

- identify cost pressures from changes in visit lengths and different hourly unit costs based on, for example, 15-minute, 30-minute, 45-minute or 60-minute visits

- model different volumes based on size of provider / branch (based on number of hours / visits delivered).

The Sensitivity Analysis Worksheet has six sections, as follows:

A. Volume and income levers

hourly unit rate (£), contact hours, visit lengths and total visits

B. Contact / direct pay levers

contact pay rate, average travel time, mileage distance and expenses

C. Non-contact / direct pay levers

non-contact pay rate, training, holiday / sickness / suspension and additional non-contact pay hours and total care staff

D. Direct care staff on-costs

weekly staff hours, staff earnings, employer’s National Insurance and pension costs

E. Consumables and overhead levers

PPE costs, back office (staff) costs and overhead (non-pay) costs

F. Profit and surplus contribution

weekly income and surplus contribution

Each section contains elements that can be adjusted (using a slider interface from a minimum to a maximum value), as well as calculated elements (which return summary values based on the adjustment made in the sliders). Any cost or volume element which can be adjusted is shown with the description of the cost element in blue. Any cost or volume element which is calculated automatically is shown in grey.

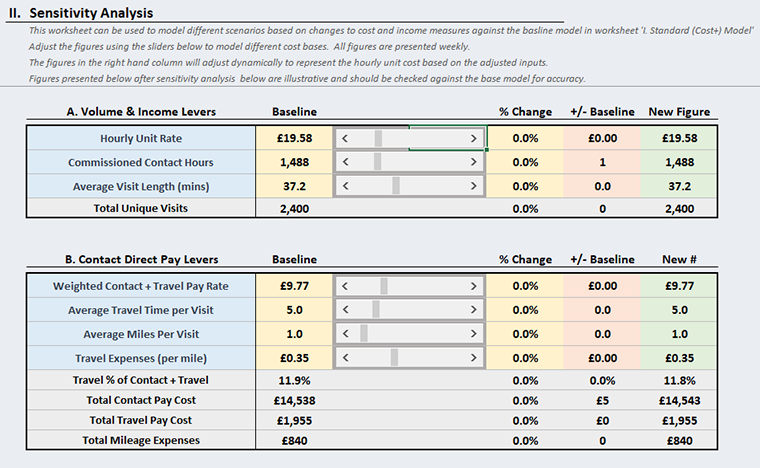

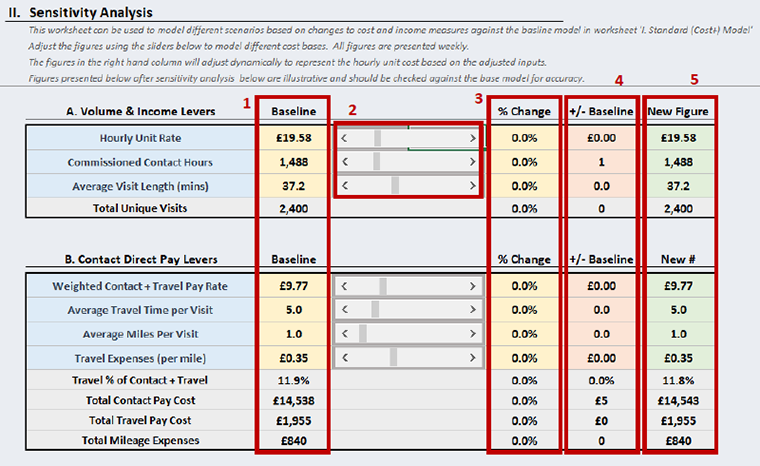

The below figure illustrates the Sensitivity Analysis Worksheet when a baseline ‘model’ has been completed (as shown in the ‘baseline’ column coloured in yellow):

The numbered boxes bordered red in the screenshot above are described below:

- The baseline figures are automatically populated from the values returned in the Standard (Cost+) Worksheet.

- Each cost or volume element which can be adjusted (that is, a cost ‘lever’) has an individual slider. The slider’s ‘zero’ (0) value will change depending on the figures in the baseline. Each slider moves cost or volume up or down in increments. The minimum and maximums are individually set for each lever depending on the nature of the indicator being adjusted. For instance, the ‘commissioned contact hours’ slider adjusts the baseline hours per week up or down in one-hour increments.

- The percentage change column will show the percentage above or below the baseline figure, based on the user adjusting the slider. For instance, if the user adjusts ‘commissioned contact hours’ upwards 10 points from the zero value, based on the example, this column will show 0.7 per cent (as the hours would move from 1,488 to 1,498 hours, which represents a 0.7 per cent increase).

- The '+/- baseline' column (in orange) shows the actual number of units increase or decrease to the new value against the baseline model. Again, using the example of ‘commissioned contact hours’, a 10 point move in the slider would give this cell the value ‘10’, denoting an increase of 10 hours per week.

- The 'new figure' column (in green) shows the new value for each variable once the adjustment has been made by the user. For ‘commissioned contact hours’, this will show the new total value to be used in the sensitivity analysis. Based on a 10-hour increase, the new figure would be 1,498 hours.

Worked example for sensitivity analysis

Assume our illustrated example (in the figure on the previous page) above represents the baseline model from the Standard (Cost+) Worksheet, we can look at the impact on profitability / sustainability on a business model, based on the adjustments in the sliders. The below sections describe an illustrative cost and volume change to show the impact, and what may be considered when modelled the cost impact.

a) Baseline – unit rate and operating surplus

In this example, the user has established a baseline that draws £29,127 of weekly income, with a weekly profit / surplus £ of £1,120 (or 3.8 per cent when expressed as a percentage).

Our column ‘new #’ needs to be adjusted, based on some cost and volume changes in the market.

b) Modelling volume change

Let’s assume demand for hours in the market has grown by 10 per cent. This is represented by the number of commissioned contact hours increasing by 10 per cent (or 149 weekly hours); to give a new total of 1,636 hours per week.

In addition, the average length of visits has reduced to 35 minutes (compared to the baseline of 37.2 minutes). This means our new level of demand has also adjusted to having a higher proportion of shorter visits than previously.

The net impact of the changes is that the total unique visits has grown by 16.9 per cent to a new total of 2,805 per week.

We see the increased volume now being delivered has affected the weekly profit/surplus contribution line, due to the increased variable costs as we have to account for worker direct pay and non-contact pay which will increase in proportion with the increase in hours.

The weekly profit / surplus contribution (that is, profitability) has increased to 5.3 per cent (an additional £575 per week, assuming the unit cost is equal to the income rate obtained for the hours delivered).

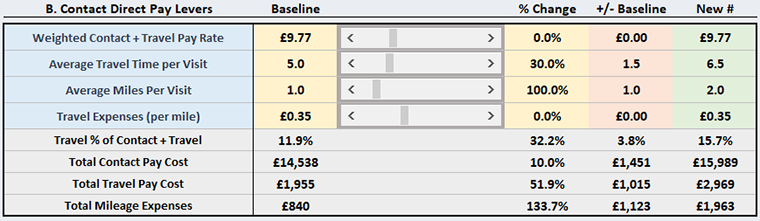

c) Additional costs

Let’s consider that this new volume has come with additional costs. In the below example, the average travel time per visit has increased to 6.5 minutes (from the baseline value of 5 minutes), as the volume increase is largely made up of more rural visits. In addition, the average mileage distance has increased from 1.0 mile to 2.0 miles.

The table above shows the impact of these changes on pay costs:

- Contact (£1,451 increase) and travel (£1,015 increase) pay costs have increased by a total of £2,466 per week due to the increased number of visits and travel costs

- Total mileage expenses have more than doubled (from £840 to £1,963) due to increased visits and more mileage travelled.

The increase in visits and therefore scheduling activity has added an extra cost to our back-office staff of approximately £3,000 per year. We can show this as an increase of 1.9 per cent increase, or £58 a week.

If we look at what these additional changes have done to weekly profit/surplus contribution, we see this has caused a viability issue. The table below shows that despite the fact that volume has increased and income has grown by £2,908 per week, the additional costs now cause a loss of £155 per week, based on the existing unit rate of £19.58.

d) Adjusting for cost impacts

We should now determine what the rate would need be to reach the same level of weekly profit/surplus contribution that existed in the original ‘baseline’ model, based on volume, income and cost.

To do this, the user can adjust the unit rate at the bottom until the figures match the desired weekly profit / surplus contribution.

We can see in the final example below, that a unit rate increase of four per cent (or £0.78 on the baseline unit rate) will allow our new model to obtain the same weekly profit / surplus contribution as before (£1,121 per week).

e) Real-life use cases

Whilst the above represents just one example of how the sensitivity analysis can be used, there are a number of levers that can be adjusted to model different scenarios. These may be helpful in the mix of considerations users of the toolkit make when looking at unit costs and profitability in delivering traditional homecare models based on hours of care. However, the Homecare Cost of Care Toolkit should only form part of an approach and not be relied upon in its entirety to make decisions concerning profitability, overall costs or market fee rates.

Instead, use of the Homecare Cost of Care Toolkit should:

- be checked using professional financial expertise, internally or externally

- not replace other checks and balances in the normal operation of business / financial operational scrutiny

- be updated regularly, and any new actual cost information obtained should always be reflected in the Standard (Cost+) Worksheet in order to maintain accuracy of the overall toolkit.

The Apprenticeship Levy calculates any costs above the pay threshold and applies the levy percentage rate as a total cost (annualised £) in Section I. These rates can be adjusted as required.

Part C: Data Output Worksheet

Part C – the Data Output Worksheet – lists key outputs from Part A and the structure and content of this worksheet. This is an open spreadsheet that allows information to be added, removed, amended, copied and pasted as the user wants. This user guide will not provide further guidance in relation to this worksheet.

Disclaimer

This publication has been prepared only as a guide. The example figures provided in this document are for illustrative purposes and should not be used in place of locally determined figures or relied upon to make decisions concerning local costs.

While every attempt has been made to ensure that the information contained in this document is obtained from reliable sources, ARCC-HR Ltd, the Care and Health Improvement Programme (CHIP), the Association of Directors of Adult Social Care (ADASS) and the Local Government Association (LGA) are not responsible for any errors or omissions, or for the results obtained from the use of this information. No responsibility can be accepted by any of these organisations above for loss occasioned to any person acting or refraining from acting as a result of any material in this publication. Nothing herein shall to any extent substitute for the independent investigations and the sound technical and business judgment of the reader.