A paper by MHCLG

In July, the Government announced that local authorities would be allowed to spread the estimated deficit on the 2020-21 Collection Fund over three years.

Following discussions with CIPFA, this paper looks at the approach the Government proposes to take to spreading business rates and Council Tax deficits.

Introduction

1. For the purposes of Collection Fund accounting, the treatment of council tax and business rates surpluses and deficits is essentially the same. Before the beginning of the financial year, billing authorities calculate their council tax requirement (including precepts) and their estimated non-domestic rating income. Based on these calculations, payments from the Collection Fund are “fixed” and paid over the course of the year.

2. Any surplus, or deficit on the Collection Fund, as a result of income from council tax/ratepayers being more or less than originally estimated, are shared between billing and major precepting authorities (and, in the case of business rates, with central government).

3. The process of sharing surpluses and deficits is spread over two years. Before the end of the financial year in question (year 1), billing authorities are required to estimate what the surplus/deficit on the Collection Fund will be at the end of that year. The estimated amount is paid to authorities (in the case of a surplus), or by authorities (in the case of a deficit) over the course of the following year (year 2); and must be taken into account when authorities set their year 2 budgets.

4. When outturn figures for the financial year in question (year 1) are available (about midway through year 2), the difference between the actual year 1 surplus/deficit and the estimated surplus/deficit is payable by/to authorities during the course of year 3 and must be taken into account when authorities set their year 3 budgets.

5. As a result of Covid-19, there is likely to be a larger-than-normal deficit on the 2020-21 Collection Fund. Authorities will estimate the deficit in December 2020/January 2021 and budget for it in 2021 budgets, raising concerns that spending on local services will be significantly curtailed and/or authorities’ financial viability put at risk in 2021-22.

6. Therefore, the Government announced that they would amend secondary legislation to allow authorities to spread the estimated deficit on the 2020-21 Collection Fund, over the three years 2021-22 to 2023-24.

Summary of approach

7. The calculation of Collection Fund surpluses/deficits is set out in Regulations. The Government’s intention, therefore, is to amend regulations to change the statutory calculations.

8. Broadly speaking, (and subject to the further detail in paragraphs 16 onwards), the proposed amendments will require authorities to credit two-thirds of their estimated loss of council tax and non-domestic rating income in 2020-21 in the calculation of the estimated surplus/deficit they make prior to 2021-22. This will reduce the estimated deficit on the Collection Fund that is to be taken into account in setting 2021-22 budgets by two-thirds of the loss of 2020-21 income, leaving authorities to deal with only a third of that loss in that year’s budgets.

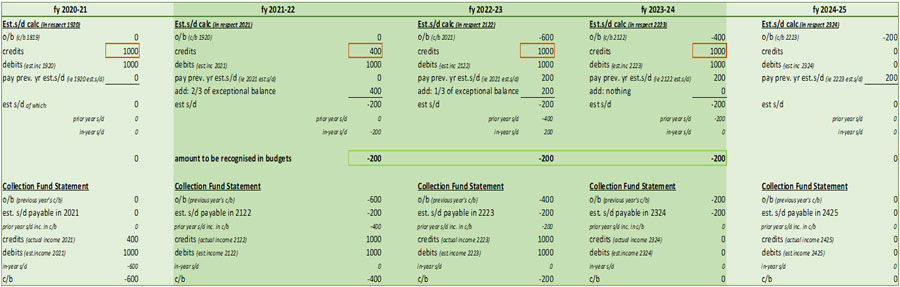

9. In the following year’s calculations, the Regulations will require authorities to include a credit one-third of estimated loss of 2020-21 council tax and non-domestic rating income; and because of the way the estimated surplus/deficit calculation interacts with the real surplus/deficit recognised in the Collection Fund Statement, this will have the effect of spreading the estimated loss of 2020-21 income over three years, as shown below in figure 1.

10. Figure 1 shows, in isolation, the treatment of a loss of income of 600 in respect of 2020-21, which is perfectly forecast by the authority in their estimated surplus/deficit calculation immediately prior to 2021-22 – as shown in the top half of fig. 1 in the second column. (The credits and debits – of 400 and 1000 respectively – represent the actual and estimated income for 2020-21.) The full 600 deficit would normally have been reflected in 2020-21 budgets. But by adding back 2/3rds of this value, authorities are left having to budget for a deficit of only 200.

11. The actual deficit of 600, however, has to be recognised in accordance with normal accounting practice in the 2020-21 Collection Fund Statement (shown in the bottom half of fig.1 in the first column); and in accordance with Regulations, the closing balance of-600 is carried forward into the estimated surplus/deficit calculation made before the start of 2022-23 (top-half of fig 1, third column). Because only 200 of the deficit was paid off over the course of 2021-22, this would have normally left an estimated deficit of 400, which authorities would have been expected to budget for in 2022-23. But by adding back one-third of the original estimated deficit of 600, authorities are again left to budget for a deficit of 200.

12. But in accordance with proper accounting practice, the full deficit of 400 is recognised in the 2021-22 Collection Fund Statement (bottom half of figure 1, second column); and this is carried forward to the estimated surplus/deficit calculation made before the start of 2023-24 (top half of figure 1, fourth column). Because another 200 was paid off in the course of 2022-23, this leaves an estimated deficit of 200, which authorities must include in 2023-24 budgets. In this way the original estimated deficit of 600 is spread equally across 2021-22, 2022-23 and 2023-24.

13. It is important to note that only the estimated loss of 2020-21 income is being spread. As explained in greater detail below, the difference between estimated and actual surplus/deficits in respect of 2019-20 will impact in full on 2021-22 budgets; and the difference between estimated and actual 2020-21 income will impact in full on 2022-23 budgets etc.

14. Also explained below is the way in which we propose to apportion the estimated surplus/deficit between authorities. Although the technical approach will differ between business rates and council tax (reflecting technical differences in the Regulations) they will achieve the same result. Using the above by way of example, the 600 which is spread 200-200-200 across the three years 2021-22 to 2023-24 will be apportioned only between those authorities who would, but for the amending Regulations, have been liable for a share of the 600 deficit in 2021-22. Each authority will pick-up the same share of the 200 as it would have picked-up in 2021-22 had the 600 deficit not been spread. Any other estimated surplus/deficits – caused by differences in estimated and actual income in 2019-20 and later years – will be shared as normal.

Policy parameters

15. In framing the necessary regulations, the Government proposes to adopt the following parameters.

Determining the deficit to be spread

16. Collection Fund surpluses/deficits are cleared over two years. Therefore, in any year, when authorities estimate the surplus/deficit on the Collection Fund (in January before the start of the financial year), the estimate comprises two elements:

- A “prior-year” surplus/deficit – which is the difference between the previous year’s estimated surplus/deficit (which is payable to/from the Collection Fund over the course of the year in question), and the actual surplus/deficit for that year; and

- An “in-year” surplus/deficit – being the estimate of the surplus/deficit in respect of the year in question.

17. In determining the deficit which is to be spread, we are proposing to provide in Regulations that only the “in-year” amount is to be used. In other words, we will entirely discount the “prior year” balance, which in this instance, will relate to 2019-20 and which will not have been significantly affected by Covid-19.

18. This will have a number of consequences. It will prevent 2019-20 prior-year surpluses from mitigating/cancelling-out the impact of Covid-19 on the in-year 2020-21 Collection Fund balance. It also means that authorities will not have to spread any prior-year surpluses. Instead they will be able to budget for the entire prior-year surplus in 2021-22 Budgets.

19. But, conversely, if authorities have prior-year deficits, they will not be able to spread those deficits, but instead will have to budget for the entire prior-year deficit in 2021-22 as well as having to budget for third of the in-year (ie 2020-21) deficit.

Mandatory vs Discretionary

20. The scheme would apply to all authorities that calculated an estimated “in-year” deficit on the 2020-21 Collection Fund. Authorities that calculated an estimated deficit would not have a discretion to opt out of the scheme. They would be required to credit or charge the sums to the Collection Fund as set out in the Regulations, thereby spreading the 2020-21 deficit over the three years from 2021-22 to 2023-24.

21. By not allowing local discretion, we will greatly simplify the administration of the scheme, not least because any decision to spread the deficit (or not) affects not only billing authorities, but also precepting authorities. Allowing discretion therefore raises issues about how and by whom the discretion is to be exercised.

22. Besides, if an authority desperately did not want to spread the cost over three years, but instead wanted to bear the full cost in 2021-22, it could do so through adjusting its Reserves, notwithstanding the requirements of the Regulations.

23. Authorities that calculated an estimated surplus on the 2020-21 Collection Fund, will not be required (or have discretion) to spread the surplus. They will simply be required to budget for their share of the estimated surplus in 2021-22, in the normal way.

24. Nor are we proposing to make a de-minimis provision under which small deficits (measured, perhaps, as a proportion of the Council Tax Requirement, or a proportion of 2020-21 estimated (NNDR1) non-domestic rating income would be exempt from the need to spread. In part this is in the interests of administrative simplicity, but also because some precepting authorities cover a large number of billing authorities and whilst the deficits in individual billing authorities might be small, when taken together, they could (at least, in theory) leave precepting authorities having to budget for more significant amounts

Separate calculations

25. Although the basic approach to spreading estimated surplus/deficits will be the same for both council tax and business rates, we propose to treat them separately for the purpose of determining:

- the amounts to be spread; and

- how those amounts are to be apportioned between billing and precepting authorities.

not least, because in respect of any billing authority’s Collection Fund, the bodies who are liable for a share of the council tax deficit will be different from those who are liable for a share of the business rates deficit.

26. This means, of course, that it will be possible for an authority to spread, for example, a council tax deficit, whilst budgeting for a business rates surplus, or vice versa.

27. The alternative of requiring authorities only to spread a deficit balance if there is a net deficit on both council tax and business rates would introduce considerable complexity into the scheme.

Fixing the amount to be spread

28. The amount to be spread would be determined by the calculation of the estimated 2020-21 deficit. Once calculated it would be fixed and would determine the sums to be credited to the estimated Collection Fund calculations in each of 2021-22 and 2022-23. This means that to the extent that the estimated 2020-21 deficit is inaccurate, there would be no opportunity to adjust it in 2022-23 and 2023-24.

29. Effectively, therefore, the difference between the estimated and actual 2020-21 surplus/deficit would not be spread, but would be treated as usual – in other words, the entirety of the difference would hit 2022-23 budgets.

30. Nor are we currently proposing to spread future deficits. So, if deficits were significant in respect of 2021-22 or 2022-23, the full estimated deficit would hit budgets in 2022-23 or 2023-24 along with the third of the 2020-21 estimated deficit which had been carried forward to that year.

Shares

31. The estimated 2020-21 deficit (lower because of the amount credited to the calculation in accordance with the amendment regulations) will be apportioned between authorities in accordance with the shares due to each authority in respect of the 2020-21 in-year balance

32. In subsequent years, we propose to provide that the balance of the estimated 2020-21 deficit which authorities will have to budget for in 2022-23 and 2023-24 should be shared between the billing authority and those precepting authorities who were liable for the 2020-21 deficit, in the same proportions as applied in respect of 2020-21.

33. In other words, if the identity of the major precepting authorities changes between 2020-21 and 2023-24, only those authorities that were liable for a share of the 2020-21 deficit will be expected to bear the liability for the remaining thirds of that deficit in 2022-23 and 2023-24. Similarly, we will provide that the apportionment is made on the basis of the shares applying to the 2020-21 deficit, regardless of how those shares may change subsequently.

34. The only exception will be in respect of authorities that are reorganised after 2020-21, who will pick up the liability of their predecessor authorities in the same way as they pick-up other liabilities.

Phasing

35. The Government has announced that the 2020-21 Collection Fund deficits will be spread over three years. Currently, as outlined, in paragraphs 7 - 12 above, we are proposing that this should be done in equal amounts, such that authorities are having to budget for a third of the 2020-21 estimated deficit in each of 2021-22 , 2022-23 and 2023-24.

36. It would be possible to phase the repayment of the deficit differently. For example, if authorities were felt to be under most pressure in 2021-22, we could require that only one-sixth of the deficit hit budgets in that year, with perhaps two-sixths hitting budgets in 22-23 and the remining three-sixths in 23-24.

37. It is not however obvious why one set of phasing arrangements is better than another, or what phasing would be preferred by the majority of authorities.

Business rates: deficits and s.31 payments

38. Following the submission of NNDR1s in January 2020, the Government significantly amended and extended the reliefs that could be given to ratepayers for which authorities would be compensated through s.31 payments.

39. Because the additional reliefs, provisionally estimated to cost in the region of £10 billion, were not included in NNDR1s, the amount of business rates collectible from ratepayers will be £10+ billion lower than the figure for non-domestic rating income included in NNDR1s, on which payments from the Collection Fund in 2020-21 were based. This means that, regardless of any other Covid-19 impact, there will be a £10+ billion deficit on the Collection Fund.

40. The deficit attributable to additional reliefs, however, is not a “real” deficit. Authorities will receive s.31 grant for the loss of income arising from the additional relief. This element of the deficit is therefore being fully funded by Government and will not impact on local authority budgets in 2021-22.

41. Accordingly, we are proposing to exclude the proportion of the in-year deficit attributable to additional relief from the phasing arrangements.

42. In practical terms, because we will not know how much additional relief authorities have awarded until after 2020-21 NNDR3s are returned in mid-2021, we will need to use an estimated figure for the additional relief given and deduct this from the estimated in-year deficit.

43. Our proposal is not to use the estimate of additional relief made by authorities in April, or October, but instead to ask authorities for a later estimate made at the time they submit their estimated surplus/deficit calculations. Such an estimate is likely to be a better reflection of the outturn figures than an estimate made earlier in the year – see paragraphs 44 – 49 below for further detail on the implementation of this proposal.

Practical implementation – Business Rates

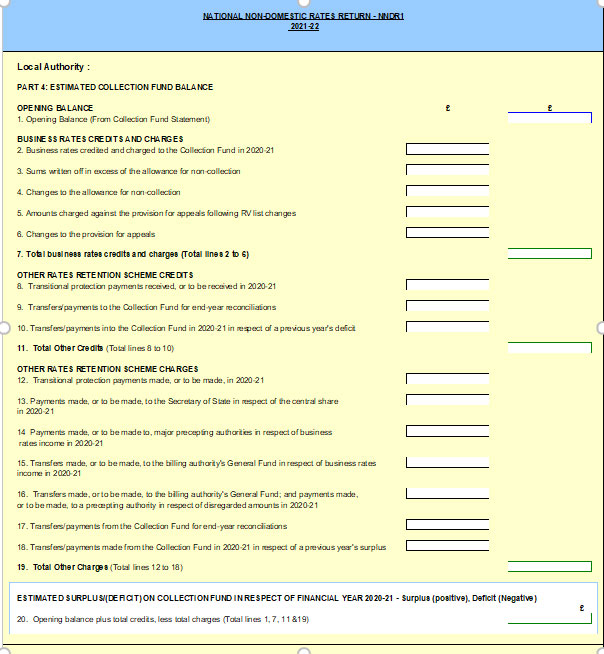

44. Part 4 of the 2021-22 NNDR1 will provide for the calculation of the estimated surplus/deficit on the Collection Fund for the previous year (2020-21). The format of Part 4 is reproduced below. In each of 2021-22 and 2022-23, we propose to add a new line immediately after line 19, (“line 19a”) allowing for the entry of the credit needed to spread the in-year deficit. This would mirror the approach we took between 2014-15 and 2017-18, when authorities were allowed to spread the cost of backdated appeals.

45. We could provide guidance to authorities on how to calculate this figure. But we believe that the better approach would be to provide for the automatic calculation of the “line 19a” figure on the face of the NNDR1, based on the entries made by authorities in Part 4. We propose to do this in a new Part 4A to the NNDR1.

46. The only other calculation that would be needed would by that required to strip out the “in-year deficit” created by the s.31-funded additional reliefs. As indicated in paragraph 43 above, our preference would be to base this calculation on an up-to-date estimate of the additional relief to be awarded. Rather than conduct a separate data collection exercise, we propose to use Part 4A of the NNDR1 to capture this figure. Authorities would be asked to enter their latest estimate of the relief they would award ratepayers in respect of retail relief, nursery relief and local newspaper relief. The sum of these reliefs, less the NNDR1 figure for retail relief, would give a good proxy for the value of the additional relief given.

47. Part 4A would also be used to apportion the final estimated surplus/deficit figure (between authorities. To so this we will need to breakdown the final estimated surplus/deficit (ie after taking account of the amounts to be credited to the calculation in 2021-22 and 2022-23) into prior-year and in-year estimated surplus/deficits and, exceptionally, into the deficit that is being spread over the three years.

48. The advantage of constructing a new Part 4A, apart from being able to set out the calculation, would be that it would keep the data entry for the 2020-21 additional relief, separate from the rest of the NNDR1 which, of course, requires data entries in respect of 2021-22 amounts.

Practical implementation: Council Tax

49. There is no equivalent of Part 4 of the NNDR1 for Council Tax surpluses/deficits, not least because, unlike business rates, central government does not have a share of the Collection Fund balance for Council Tax and, therefore, there is not the same need to collect information on council Tax balances.

50. In respect of Council Tax, a billing authority is already required by Regulation 11(3) of the Local Authorities (Funds) (England) Regulations 1998 (SI 1998/2428)(as amended) to notify its precepting authorities of the Council Tax surplus/deficit and of how this will be apportioned between them. In amending the Regulations to provide for changes to the calculation of the estimated surplus/deficit, we will provide that, in respect of 2021-22,the billing authority must indicate the total value of the 2020-21 deficit that is being spread and the share, by value, of that deficit that each authority will be expected to bear in each of the three years 2021-22 to 2023-24. For 2022-23 and 2023-24, the billing authority will be required to identify the value of the 2020-21 deficit that is being charged to each of its precepting authority in that year.

51. To ensure transparency, we will amend the Council Tax Requirement (‘CTR’) forms due to be returned to the Department in respect of each of 2021-22, 2022-23 and 2023-24. For these years, billing authorities will be required to provide data on the Council Tax Collection Fund deficit that is being spread, as well as its apportionment between the billing authority and its major preceptors.

52. We will issue advice to authorities setting out the requirements of the amendment regulations, including how authorities are to calculate the sum to be spread and the basis on which it is to be apportioned. We might go further, if helpful, and provide, exceptionally for the years 2021-22 to 2023-24, a proforma like part 4 of the NNDR1, to automatically calculate the estimated council tax surplus/deficit based on the Regulations and data entries by authorities.

14 October 2020