1 Introduction

1.1 Background

During 2020, Local Partnerships and the Local Government Association (LGA) developed a greenhouse gas (GHG) accounting tool to cover Scope 1 and 2 and limited Scope 3 emissions. Local Partnerships and the LGA worked to promote and launch the GHG accounting tool, including a webinar in September 2020 and promotional activity in the LGA climate change bulletin. To date there has been over 400 downloads of the tool.

At the launch webinar, feedback was sought from local authorities regarding the usefulness of the tool. The general feedback was good, but there was a clear feeling that further work would be appreciated in relation to Scope 3 emissions.

Scope 3 emissions are a complicated area to report, and sector led guidance is an excellent way of promoting consistency and speeding up progress. Some areas of local authority activity, such as office buildings, are already covered by sector-specific guidance. However, key areas of local authority spend do not currently benefit from sector specific guidance, including social care, waste and highways. This has led to limited Scope 3 reporting and missed opportunities for driving emissions reductions. Additionally, a general lack of consistency means local authorities may apply poor screening exercises, undertake incorrect assessments and ultimately, under-report Scope 3 emissions.

Sector specific guidance will help with providing clarity in interpretation of the Greenhouse Gas (GHG) Protocol and support improved accuracy and robustness of reporting. Good guidance will help local authorities:

- understand what Scope 3 emissions are for the activity area

- identify the most material activities from the services provided

- accurately account for their activities.

1.2 This guidance

Local Partnerships was commissioned by the Local Government Association to produce guidance for local authorities on measuring and managing Scope 3 greenhouse gas (GHG) emissions.

This is sector-specific guidance for social care services Scope 3 GHG emissions, covering all the main aspects of social care spend and applicable to both outsourced and in-house services.

The key areas of social care which the guidance covers are:

- older adults – residential and nursing care, domiciliary care, extra care housing, day care

- adults with disabilities – residential care, day care, supported housing, floating support, respite care

- single homeless – hostel, supported housing, floating support

- homeless families – temporary accommodation

- children – residential care, foster care, domiciliary care and advocacy and support

- community based service

- transport to specialist services.

It is structured as follows:

- introductory information, including what Scope 3 emissions are

- screening – a starter’s guide for local authorities when undertaking Scope 3 reporting to aid beginners, and a refresher note for those more advanced

- technical – interpretation of accounting protocol for social care and recommended approaches to accurately account for key activities.

1.3 Who is this guidance for?

This guidance is aimed at:

- climate/sustainability officers in local authorities with overall responsibility for emissions reporting.

- social care commissioning officers with responsibility for the commissioning and procurement cycle, setting key performance indicators (KPIs) and managing ongoing contracts.

- social care providers within the value chain, who will be reporting on their own Scope 1 and 2 emissions, which will be a requirement for councils’ Scope 3 requirements.

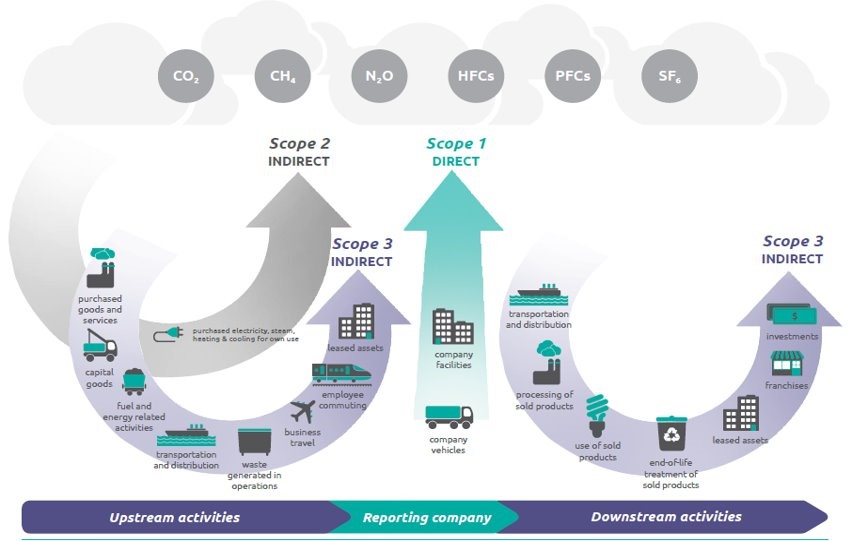

2.1 The GHG Protocol and emissions scopes

The GHG Protocol splits emissions into three distinct reporting scopes, which are depicted below:

Scope 1 emissions are released as a direct result of an activity. For a Council this will largely comprise combustible fuel for heating boilers and fuel burned in owned fleet vehicles. There may also be an element of fugitive emissions from air conditioning units and medical gases used in care provision.

Scope 2 emissions are those released as an indirect consumption of an energy commodity. For a Council this will be the purchased grid electricity used in its operations (buildings and street lighting).

Scope 3 emissions are all other indirect emissions other than electricity. The measurement of Scope 3 emissions is an emerging area and they usually represent 70-80% of a local authority’s total emissions5. Scope 3 emissions reporting is relatively new, and methodologies are still emerging to allow for measurement in many areas.

This diagram shows that under the Corporate Standard (which also applies to councils), emissions sources are categorized as direct or indirect and then further divided into scopes.

Direct sources are all owned or controlled by the reporting council. Direct sources are classified as Scope 1.

Indirect sources are owned or controlled by another company, but a portion of those emissions are from the actions of the reporting council. Indirect sources are known as Scope 2 or Scope 3.

Scope 2 emissions consist of electricity, heat or steam that is purchased by the reporting company.

Scope 3 emissions are all other indirect emissions, such as capital goods, business travel, investments, transportation, and distribution.

These activities can lead to emissions such as carbon dioxide, methane, nitrogen trifluoride, fluorocarbons, nitrous oxide, sulphur hexafluoride.

2.2 What are Scope 3 emissions?

In the Local Authority context, Scope 3 emissions are the emissions that are indirect emissions as a result of council activity. These will include emissions from water consumption, outsourced fleet vehicles, staff business mileage and major outsourced services such as waste management/treatment, highways maintenance and social care provision.

Social care provision will be a mix of contract and service types, adding complexity to the reporting landscape, the practicalities of data collection, and the ability for the reporting authority to make a meaningful impact in reducing greenhouse gas emissions.

The GHG Protocol Scope 3 Accounting and Reporting Standard states emissions that should be reported as Scope 3 are:

- emissions from activities in the value chain of the entities included in the company’s organisational boundary.

- emissions from leased assets, investments, and franchises that are excluded from the company’s organisational boundary but that the company partially or wholly owns or controls.

For a council this would mean emissions that are a consequence of the council’s operations that occur at sources the council does not own or control and that are not classed as Scope 2 emissions. Typically, these relate to the emissions associated with the transmission and distribution of the council’s purchased electricity, outsourced or contracted operations and business travel by means not owned or controlled by the council.

Scope 3 emissions are more difficult to account for, because the required data often lies with other organisations or individuals. As a result, there is a higher degree of estimation in Scope 3 categories.

A first step towards reporting on Scope 3 emissions will be to understand what the emissions sources are, whether the data is available and the degree of accuracy of the available data before embarking on producing a Scope 3 baseline. This will involve an emissions mapping exercise, and the production of a plan to develop the reporting for this service area – it is unlikely that all the data for the reporting activities outlined in this guidance will be available at the outset for most local authorities.

Setting a base year for Scope 3 emissions from social care may be a more recent point in time than a council will have set for their Scope 1 and 2 emissions, as councils may have been reporting on these emissions for a number of years, data is readily available and reporting methodologies are well established. Scope 3 emissions reporting for outsourced services is not as well established, and it may take some time to establish a reporting boundary and identification of activities on which to report. A base year for social care emissions should be set, this may not be the first year of reporting, it may be more appropriate to set a base year to align with a specific point in the care commissioning cycle, for example, which may be in the future. For example - reporting can be undertaken prior to this, to establish emissions sources and the data collection requirements. The base year can be set for when the Scope 3 inventory is sufficiently complete and reliable, for example at the point of commissioning a new major contract.

2.4 Drivers for reporting

The underlying purpose of all GHG emissions reporting is to provide transparency so that opportunities for improvement can be identified. An initial mapping and screening (section 2.6) review should enable a local authority to identify the areas to focus on initially. Other measures can follow, it is not necessary to have a complete Scope 3 inventory to start reporting provided you keep a clear record of what has been included and excluded for future years comparison and have a robust plan for developing the missing data sources.

An increasing number of local authorities are starting to report on a wider range of metrics within Scope 3. The Carbon Trust has developed a helpful guide for beginners - ‘Make business sense of Scope 3’. An extract is provided below:

Carbon Trust Best Practice in Managing Scope 3 Carbon Emissions.

Best practice in managing Scope 3 carbon emissions

1. Keep a focus on business needs and value generation that can be derived from measuring and interpreting Scope 3 emissions.

2. Understand what existing data can be used, and how easily additional data can be obtained.

3. Start with a very wide, but shallow view to have an initial understanding of how to focus efforts, by taking 'amount bought' and 'amount sold' multiplied by the most applicable emission factors.

4. Then where appropriate engage with companies/customers, obtaining primary data, collaborating in person at an appropriate level of detail and scope, by either:

a. Continually build out 'important' areas to understand in more detail, upon which to build out reduction plans, and/or

b. Focus in depth on a few most important products/categories, using product foot-printing or value chain optimisation approaches to understand in detail how to move from the current state to a more profitable and more sustainable future state - and then extrapolate key findings to other products/categories as applicable.

5. Ensure suppliers feel part of a 'value chain enterprise' working together with other companies to improve the efficiency of products to meet end-consumer needs.

6. Put information into the hands of decision makers about how their decisions impact the total value chain, not just their operations; and change their KPIs to reward them for optimising the total and not their part of the value chain.

2.5 Control and influence

A key theme for a council looking to set a Scope 3 reporting boundary is control vs influence, which links to the concept of direct and indirect emissions. What do we mean by direct and indirect sources of emissions, and how much control do we have over them? The box below offers an explanation in relation to the emission scopes.

Indirect emissions you have less control over – you don’t decide the fuel mix in the power station for the electricity you consume for scope 2 emissions, scope 3 you have no control over the manufacturing process of the goods you purchase. You do have influence over this however, through your purchasing choices.

Scope 2 emissions – whilst you don’t make the decision about the power station fuel source, you can take action to use the electricity you purchase in the most efficient way.

Scope 3 emissions – you don’t decide how a particular product was manufactured, however you can make choices about the types of products and source materials that you do purchase.

Applying this concept to social care and identifying emissions sources and activities that may be appropriate to include in Scope 3 reporting requires understanding the levels of control and influence that a council has over its commissioned services.

This will be further explored in section 2.6.

2.6 Mapping and screening

In addressing Scope 3 emissions and deciding what to include in future reporting, councils need to prioritise activities where data collection and reporting will lead to a meaningful impact.

The mapping/screening activity is required to understand the scale of the emissions that could be reported as Scope 3. To identify all possible emissions sources for each of the reporting categories, it is often referred to as casting a “wide but shallow net”. This approach will identify all possible sources of emissions from service provision in house, and by care providers commissioned by the council, and then undertake a prioritisation activity to focus in on those emission sources where meaningful data can be reported, and where there is opportunity to manage and reduce emissions.

The following sections outline the steps to work through.

2.7 Emissions sources

Emissions sources from social care provision can be initially identified via the following categories as listed below:

Emissions may come from services delivered in-house, in which case, they will have mostly been measured as part of the council’s own Scope 1 and 2 accounting, and/or from outsourced providers, in which case they will form part of the council’s Scope 3 emissions. Outsourced providers may be from the private or voluntary sectors and be commissioned and non-commissioned.

As Scope 3 emissions are ones arising from activities over which the council has indirect control, then non-commissioned activities should not be included as the transaction is voluntary and not dependent on funding or other direct support from the council.

Examples of non-commissioned activity could be a church shelter for homeless people or a private care home for older people. However, if the council is funding residents in private care homes then they should be included in Scope 3 activity (consideration of a proportionate calculation for the number of beds).

The first step in mapping emissions is to create a long list of all social care contracts and services commissioned by the council. Include details about the contract value, length, type of provider (large national provider, Small Medium Enterprise, individual), volume purchased for equipment/consumables to cast your wide net across all activity that could be reported on.

As part of this exercise, information relating to existing KPIs or available data relating to each contract should be captured.

2.10 Which care services should be reported on?

| Type of care | Buildings emissions | Employee and other transport emissions | Equipment emissions | In-house (I) or outsourced (O) |

|---|---|---|---|---|

| Residential/day activities | Y | Y | Y |

Both |

| Domiciliary care | Y | Y |

Both |

|

| Support/advocacy and community based services | Y | Y |

Both |

|

| Transport for clients and equipment | Y | Y |

Both |

What should be included for each of these types of care are considered in turn below.

Residential and daycare

This includes residential care, nursing care, supported accommodation and hostels, daycare, and respite care for older adults, vulnerable adults and children.

These types of care will be delivered from a building, either owned by the council in the case of in-house care or used and occupied by the council’s clients as part of an outsourced contract. The fuel supply will have been measured in Scope 1 for gas and other combustible heating fuels and Scope 2 emissions grid supplied electricity for in-house services but not for outsourced contracts. Consequently, this is an area of focus for outsourced contracts and a reporting KPI should be included within contracts for these contracts.

Residential and daycare will involve staff travelling to a particular building to deliver the care, so for both in-house and outsourced contracts this business travel will form part of relevant Scope 3 emissions.

Both in-house and outsourced residential and daycare settings will be involved in purchasing goods and equipment, including PPE for staff, hygiene products for clients and food and drink.

Domiciliary care

This includes home care services, foster care for children and supported lodgings for vulnerable adults.

In the case of home care, services are delivered to the client’s home and so the council has no influence over the emissions generated from clients’ premises, so these emissions would not form part of the council’s Scope 3 reporting. Emissions as a result of travel between visits (recorded as staff business mileage) will be reported as a council’s own Scope 3 emissions for directly employed staff, and mileage and fuel data should be requested from outsourced care providers (which will also be part of the council’s own Scope 3 reporting).

Support and advocacy and community-based services

This includes a range of services, including support to children, families and older and vulnerable people either in their own home or delivered from office accommodation or other settings. This includes services commissioned by public health and adult skills. Given that the outsourced component of these services is relatively small, and the council’s own office accommodation will have been measured in Scope 1 reporting, it is not suggested that this is included as a priority activity for Scope 3.

Transport for clients and equipment

This includes transport for clients to and from day activities, including schools and holiday activities for children, and transport of equipment to clients. It could either be by means of the council’s own vehicles or an outsourced contractor’s vehicles. Use of the council’s own vehicles will have been included in Scope 1, but any outsourced contractor’s vehicles should be included in Scope 3.

Equipment should be included in both in-house and outsourced services.

2.11 Commissioning considerations

It will always be most effective to consider GHG reporting at the beginning of the commissioning cycle, as it is difficult to impose new requirements on a contract mid-term without affecting cost or performance. It is also important to consider different types of suppliers and how any additional reporting requirements may affect them. For example, small, local suppliers may not be able to bear the burden of additional reporting in the way that a large national provider can. Given that large suppliers are normally delivering larger contracts then it makes sense to start with them, and to apply discretion to any additional burdens to small suppliers. Council commissioners will understand the nature of their suppliers.

It will always be important to understand the local context when considering new requirements in commissioning. For example, in an urban area, care workers are far more likely to visit their clients by public transport than in a rural area, where the use of a car will be necessary. Incentives for travel by public transport or disincentives for private travel may consequently be possible in an urban area, but unlikely to be workable in a rural one.

Such an incentive, for example by varying the amount paid for mileage according to the emissions a vehicle produces, could be applied. However, thought would have to be given to data collection requirements, and in this case to understand the potential emissions of workers’ private vehicles. This would be challenging for in-house provision and more so for outsourced contracts. One of our respondents was trialling a vehicle lease scheme for its own staff to reduce the emissions of staff travel (other incentive schemes could be salary sacrifice for the purchase of electric vehicles or bicycles).

In areas where services are jointly commissioned, for example with health partners, the council can influence the specification. Even for a contract which is solely commissioned by a health partner the council can attempt to influence ‘upwards’. For example, Medway are working with their health partner to influence a hospital discharge transport contract in order that it incentivises lower emissions.

They have also been able to introduce the following:

A community based integrated care equipment contract has specified the use of electric vehicles

In a domiciliary care contract, ‘baskets of areas’ have been allocated to keep travel by care workers to a minimum.

Children’s social workers are piloting electric vehicles.

2.12 Contract management

Suffolk County Council’s commercial ‘ask’ is engaging with suppliers across their supply chain to ask them to come on board with the Council’s commitment to addressing the climate emergency.

While it may be difficult to change contract requirements mid-contract, ways to influence behaviour can be trialled. For example, Suffolk carry out stakeholder engagement for public facing contracts, including asking clients how important climate change is to them. A high response could start to exert influence on the supplier to change ways of doing things.

2.13 Provider viewpoint

The LGA’s social care provider issue group provided insight into the issues and opportunities relating to Scope 3 reporting requirements that may be placed on them. While the majority of social care providers are not subject to GHG reporting obligations at present, larger companies may be required to report emissions under the Streamlined Energy and Carbon Reporting (SECR).

What is clear, is that for effective data collection and emissions reporting, local authorities will need to engage early with their care providers, and consider the challenges and opportunities as part of the initial mapping and screening activity.

2.15 Using a combination of calculation methods

As the number and type of services and contracts for social care provision will be varied, it will be necessary to use a combination of the calculation methods across the emission sources within the reporting boundary, and even within each of the reporting categories. The selection of the most appropriate calculation method will depend on the contribution to the overall emissions baseline – a pragmatic approach to data collection and calculations should be taken, without compromising data quality and transparency.

These could include:

- applying more accurate data/calculations for large contributors

- applying less accurate (and less time consuming) data/calculations for small contributors

- grouping or combining similar activity data (eg, goods and services)

- obtaining data from representative samples and extrapolating the results to the whole

- using proxy techniques.

Example 1: Residential care home contract

Data required from contract:

- Scope 1 – heating fuels for sites within the contract (primary data).

- Scope 2 – electricity for sites within the contract (primary data).

- Scope 3 – business mileage associated with the sites within the contract (primary data).

- Scope 3 – purchase of equipment and consumables (PPE) within the contract (secondary data).

Emissions factors required:

- UK Government factors for Scope 1 and 2 and industry average emissions values for goods purchased.

Accounting methods – Hybrid method

Sum of purchased goods and services:

∑ Scope 1 and Scope 2 emissions from supplier relating to service provision (kg CO2e)

+

∑ (value of purchased goods (£) x emission factor of purchased good per unit of economic value (kg CO2e/£))

+

Sum of business mileage:

∑ (quantity of fuel consumption (litres or miles) x emission factor for the fuel (kg CO2e/litre or kg CO2e/mile)

Example 2: Business mileage for council staff providing care services

Scope 3 – mileage/fuel consumption from staff expense claims specific to service delivery, stating vehicle size and fuel type (primary data)

Emissions factors required:

UK Government factors for Scope 1 for each applicable vehicle and fuel type.

Accounting methods – Fuel or distance based method

Sum for all vehicle types:

∑ (distance travelled by vehicle type (miles) x vehicle specific emission factor (kg CO2e/mile)

Or

Sum for all vehicle types:

∑ (quantity of fuel consumed (litres) x fuel specific emission factor (kg CO2e/litre)

Example 3: Council purchase of PPE

Scope 3 – spend data, quantity of goods (primary data).

Emissions factors required:

Industry average emissions values for goods purchased.

Accounting methods – Spend based method

Sum of all purchased goods or service:

∑ (value of purchased goods (£) x emission factor of purchased good per unit of economic value (kg CO2e/£))

2.16 Data improvements over time

The scale and complexity of social care commissioning by councils means that the process of data collection, making assessments of and implementing measures to improve data quality will be an iterative one.

Understanding the commissioning cycle will be key, to forecast when additional data sources and services may get included in the Scope 3 reporting inventory, and councils may well wish to focus efforts to improve data quality for activities that make a more significant contribution to the overall emissions baseline or have longer duration contracts, and where they are in a position to put in place measures (contract KPIs, commissioning standards) that will result in a meaningful impact on emissions reduction.

2.17 Conclusion

This guidance document provides an interpretation of the GHG Protocol for Scope 3 reporting for councils and the social care sector, to support the development of ongoing emissions reporting by local authorities. Scope 3 reporting for social care is complex, and the range of scale of service delivery means it may take councils some time to build up a comprehensive dataset. The steps outlined in this guidance will support improved reporting and drive meaningful change for the sector as more councils and care providers engage. The greenhouse gas accounting toolkit provides a mechanism to collate and report Scope 3 data as part of a full greenhouse gas emissions report.

Contact

Contact details

Rachel Toresen-Owuor

Programme Director, Local Partnerships

Email: [email protected]

Tel: 07825 963 218

Disclaimer

This report has been produced and published in good faith by Local Partnerships and Local Partnerships shall not incur any liability for any action or omission arising out of any reliance being placed on the report (including any information it contains) by any organisation or other person. Any organisation or other person in receipt of this report should take their own legal, financial and/or other relevant professional advice when considering what action (if any) to take in respect of any associated initiative, proposal or other arrangement, or before placing any reliance on the report (including any information it contains).

Copyright

© Local Partnerships LLP 2021