Introduction

The overall aim of this workbook is to support portfolio holders and committee chairs to proactively shape good financial management and decision-making and to contribute to financial governance.

Many non-finance portfolio holders and committee chairs receive financial information and react to it. An effective portfolio holder or chair leads by being proactive about finance.

The workbook considers the role of the non-finance portfolio holder and committee chair in the financial planning, control, and decision-making process. The first two sections outline the various roles and responsibilities of councillors and officers in relation to financial governance. Later sections consider the importance of the budget-setting and monitoring processes. The final section brings the financial process together with wider service policy and performance, setting finance in its appropriate place alongside non-financial service information.

We also recommend that councillors complete our councillor e-learning module on the same topic.

This workbook does not seek to provide a detailed overview of how local government finance works, which can be found in our separate councillor workbook on local government finance, which – if you are very new, or unfamiliar, with the world of local government finance – you may wish to review before working through the material below

Before undertaking this workbook, we suggest that you obtain current versions of several financial reports and documents. As a portfolio holder or committee chair, you should have direct access to all the documents and reports – many, if not all, will be publicly available as they will be reported via a council committee. While the format of such documents tends to vary with the nature, history and size of the council, the documents should contain similar types of information (explained below). We suggest that you note the style and content of the reports you receive from officers and review them against this workbook.

This workbook is applicable to leading councillors in different types of council governance system. We use the term ‘portfolio holder’ to refer to leading councillors who sit on the cabinet / executive in a cabinet governance model and we use the term ‘committee chair’ for chairs of the main policy and service committees that operate in a committee governance model. The workbook has not been tailored to councillors who have the leading responsibility for finance, such as a finance portfolio holder but may be useful for them as a tool to support other leading councillors understanding their financial responsibilities.

You do not need to complete the workbook all in one session, so please do work at your own pace. However, we suggest that you complete the sections in the order in which they appear, as the later sections build upon the knowledge you will have gained by working though the previous sections. It is also hoped that you can 'dip in' to any section for a refresher at any time in the future as well.

Throughout this workbook you will encounter different types of information, and suggested actions, indicated by the symbols shown below:

Guidance

– this icon indicates guidance such as definitions, quotations, and research

Challenges

– this icon indicates questions asking you to reflect on your role or approach

Case studies

– this icon indicates examples of approaches used in different settings

Hints and tips

– this icon indicates best practice advice

Useful links

– this icon indicates sources of additional information

Finally, you will note that some terminology used in this workbook is in bold type. This means that the term is more fully defined in the glossary of terms at the end of the workbook.

Councillor roles and responsibilities

All councillors are responsible for ensuring the effectiveness of the authority’s governance. Ensuring effective leadership and oversight of council finances is a key aspect of good governance in local government. Councils are legally required to achieve best value in relation to the use of their funding. When financial management ‘fails’ publicly then councillors are often in the ‘hot seat.’ But exactly who does what in relation to finance? What are the roles of the cabinet or policy and resources committee, of the resources portfolio, committee chairs and of non-finance portfolio holders? This part of the workbook explores these key questions.

What are the financial roles and responsibilities of non-finance portfolio holders?

New portfolio holders and committee chairs in local authorities rarely receive a comprehensive induction in which all their roles and responsibilities are clearly set out from the start. Instead, the usual practice is ‘learning on the job’ and – often – continuing the predecessor's pattern of work. The financial aspects of the role can often seem opaque, unclear, and rather technical. Given the high workload of many portfolio holders, it is easy for them to fall into a pattern of ‘receiving and reacting’ to financial information rather than ‘being proactive and leading.’ It is not unusual to assume that financial governance is predominantly the preserve of the resources portfolio holder and finance officers.

A good starting point for a portfolio holder who wants to fully understand and explore their financial role is to assess the current situation and what responsibilities are set out in the council’s constitution.

As a first step, write down your answers to Challenge 1 below.

Challenge 1

The constitutional role

- What does your council’s constitution state about your roles and responsibilities in relation to finance?

- If there is a cabinet member role description and/or terms of reference in the constitution, does this include reference to finance?

- What do the financial regulations state in relation to councillors’ roles?

- What are the procurement rules and what role do councillors have in them?

Financial responsibilities in practice

- Reflect upon whether you can see that what is set out in the constitution is happening 'on the ground'. Where are the gaps and overlaps?

Key challenges

- What key challenges do you face in performing your financial roles?

- What actions could you take to address these challenges?

Leadership of portfolio resources – Ten key roles

Be 'proactive and leading' on finances rather than 'reactive and receiving'

A councillor in a senior role aiming to be ‘proactive and leading,' rather than 'reactive and receiving’ will be looking to undertake the 10 key roles summarised below. These range from knowledge-based roles such as ‘understanding the general picture of local government finance’ to relationship-building through ‘developing effective relationships with key finance officers’ and understanding a range of systems and processes, for example, ‘understanding your council’s financial processes.’

A non-finance portfolio holder or committee chair should aim to:

- understand the general picture of local government finances

- understand their council's financial processes

- become adept in leading consideration of finance matters in relation to their portfolio or service committee area

- access and understand key financial information in relation to their portfolio or service committee area

- champion integration of finance and service information

- oversee financial aspects of major projects

- understand income and commercialisation in relation to their service area

- oversee financial risk

- understand partnerships and finance

- develop effective relationships with key finance officers.

A non-finance portfolio holder or committee chair will work more effectively if they:

- understand how the council’s financial processes operate

- are familiar with the stages of the budget-making process

- are aware of the assumptions underpinning the council’s medium-term financial strategy

- are knowledgeable about the key financial documents

- understand how their own portfolio or service budget is constructed

- ensure they obtain timely financial information

- are involved in budgetary discussions at key points

- act as a champion for integrating financial and service information

- search for value for money

- ensure that 'the money follows’ political priorities.

There are a range of specialised roles relating to aspects of financial governance, including:

- ensuring effective risk management and providing political leadership of risk

- considering approaches to income generation and commercialisation in the portfolio or service area

- carefully managing major projects and ensuring they are supported with robust business plans

- understanding how working with outside agencies impacts upon finances, for example, through pooled budgets

More detail on each of the ten roles is provided below.

Leadership of portfolio finances – 10 key roles framework

1. Understanding the general picture of local government finances

To succeed in this role, a portfolio holder or committee chair should:

- have oversight of the ‘big picture’ concerning national local government finance

- be aware of upcoming changes in legislation or regulations which may impact financial planning or service delivery

2. Understanding your council's financial processes

To succeed in this role, a portfolio holder or committee chair should:

- understand the council’s medium term financial strategy

- understand the council's council-wide budget process and timetable

- be familiar with the council's key financial documents, for example, relevant sections of the constitution and the financial regulations

- take responsibility for corporate financial and governance processes relating to their portfolio or service area, for example, delivering savings and risk management.

3. Becoming adept with their portfolio or committee’s financial leadership

To succeed in this role, a portfolio holder or committee chair should:

- understand how their portfolio budget is constructed

- ensure that priority-setting is informed by resource availability

4. Accessing and understanding key portfolio financial information

To succeed in this role, a portfolio holder or committee chair should:

- ensure they have access to timely financial information which is presented clearly and effectively.

5. Championing integration of finance and service information

To succeed in this role, a portfolio holder or committee chair should:

- act as a champion for integrating finance and service information, for example, ask for unit costs of services

- ensure a focus on delivering ‘value for money’

- ensure that budgetary decisions follow political priorities

- ensure that finance, performance, and risk information are all monitored regularly

6. Overseeing financial aspects of major projects

To succeed in this role, a portfolio holder or committee chair should:

- ensure that the financial aspects of major projects are carefully project-planned with robust business plans and monitoring of delivery.

7. Understanding income and commercialisation

To succeed in this role, a portfolio holder or committee chair should:

- lead politically on income generation and commercialisation activities in your portfolio or service area, ensuring appropriate due diligence and governance.

8. Overseeing financial risk

To succeed in this role, a portfolio holder or committee chair should:

- understand the council’s risk management processes and approaches

- lead politically on identifying and ensuring appropriate mitigation of risk as it relates to their portfolio or service area

9. Understanding partnerships and finance

To succeed in this role, a portfolio holder or committee chair should:

- consider the financial implications of partnership-working

- work to ‘lever’ finance through collaboration.

10. Developing effective relationships with key finance officers

To succeed in this role, a portfolio holder or committee chair should:

- develop an effective working relationship with the council's section 151 officer

- develop an effective working relationship with their ‘business partner’ (their portfolio finance manager)

- Understanding the ‘dual role’ of the finance department and its culture (see below)

Developing your financial leadership skills

How can new portfolio holders or committee chairs, or those less confident about the financial aspects of their role, develop knowledge and skills in this area?

It can be helpful to consider that in undertaking the 10 key roles, you can frame your development journey in terms of:

- building knowledge

- understanding key systems and processes

- developing effective relationships.

Potential actions to develop your confidence in undertaking your financial roles are suggested below.

- reading the key financial aspects of your council's constitution – particularly the scheme of delegation

- reviewing corporate budget monitoring and budget setting reports to your council and / or cabinet or committees

- meeting with the lead officer(s) for your portfolio/ service area to gain an overview of how your portfolio budgets are developed and monitored.

- meeting with your council's finance or resources portfolio holder or finance committee chair to fully understand your financial roles

- researching and understanding the role different parts of the governance system play in financial decision-making and oversight, for example, your council's audit committee and overview and scrutiny functions

- undertaking the LGA councillor workbook on local government finance.

- attending courses such as the LGA ‘Finance without Numbers’ programme and/or our two part online Financial Governance Leadership Essentials programme

Another approach to developing and evaluating your financial skills is set out in Challenge 2 below.

Challenge 2 – The 10 key roles as a personal development tool

Appendix 1 (see below) sets out a self-evaluation framework for portfolio holders / committee chairs to use as a personal development tool.

For each of the 10 Key Roles you are encouraged to consider:

- How well are you undertaking this role?

- What evidence would you provide to support this?

- What further actions could you take? When?

In addition, this workbook contains many suggestions which will grow your knowledge, skills, and confidence in portfolio financial leadership.

Financial Governance: The Four Faces of Cabinet Working

In a council with the cabinet model, governance works on a number of levels and financial roles and responsibilities are weaved into these different levels. ‘The four faces of cabinet-working,’ set out below, demonstrates the different levels and interplays between cabinet members and senior officers. Good financial leadership by a cabinet partly rests on clarity of the respective roles and responsibilities of the non-finance portfolio holder, the collective cabinet, and the finance portfolio holder.

Which of the roles listed below does what concerning finances and the budget?

- the finance portfolio holder

- the collective cabinet

- individual non-finance portfolio holder and senior officer

- top team (i.e. cabinet plus senior management team)

The 10 key roles framework sets out the roles of the non-finance portfolio holder, but each portfolio holder also has the responsibility to work collectively with the cabinet (and top team) in the following areas.

The role of the collective cabinet

The cabinet, when meeting and working collectively, should:

- propose the budget (alongside the policy framework) for agreement by full council

- ensure a balanced budget is agreed

- ensure the achievement of value for money and best value

- discuss and agree overall budget strategy

- set the overall strategy for income generation and commercialisation, risk management, major projects, procurement, and so on

- agree and drive forward a consistent, coherent political strategy for the council to guide budget decisions.

The role of the resources portfolio holder

In addition to the four faces of cabinet described above, the cabinet member with responsibility for finances (sometimes known as the resources portfolio holder) has a pivotal role to play in the council’s governance. In essence, they are the lead councillor with responsibility for effective financial management and governance. To be effective, they work closely with senior finance officers, and need to develop effective relationships with other portfolio holders and non-finance senior officers.

In a committee system of governance, a service committee chair would also need to consider how their role in financial governance relates to the different roles of other committees. In a committee system where there is a policy and resources committee with a particular role for finance and risk then there is a need to consider what does the policy and resources committee do separately from a service committee? Some policy and resources committees include the chairs and vice chairs from the main service committees. If this is the case, then considering what is done collectively and what is done within the individual committees is important.

Case study – Bracknell Forest Council | The constitutional role of the executive member for finance and corporate improvement

The executive member for finance and corporate improvement is responsible for:

1 .Overall performance and effective operation of the financial resources of the council, including accountancy services, payments, procurement, and income management. To have responsibility for the staff of the council, including their welfare, wellbeing, and relationship with the council.

2. The formulation of the Council’s annual revenue budget, and its implementation following its approval by Council.

3. The formulation of the Council’s annual capital budget, and its implementation following its approval by Council.

4. The powers and duties of the Council for the collection of local taxes, fee income, charges, and debt recovery.

5. Financial (including investment and insurance) management, and management of the Council’s balances.

6. The procurement processes and practises within the council. This to include the procurement obligation to obtain social value for the council’s purchasing activities.

7. To act as lead Member in relation to risk management and audit responsibilities which are not covered by the Governance and Audit committee

8. To be the joint Executive Member for the council’s property joint venture. Holding a board role on the Cambium Partnership.

9. The Executive Member for the Business Change programme and Corporate Improvement.

10. Employee relations, and staff well-being and welfare. Relationship with Trades Unions, employee associations and staff networks. To be the link with the national pay bodies and employer groups.

11. Staff training and development. To lead on being an employer of choice (recruitment, retention, and staff performance management). Staff apprenticeships and being a learning organisation.

12. Any functions under the resources and finance responsibility which are Executive Functions, and which do not fall within the remit of another Executive portfolio.

13. To represent the Council on, and to liaise with, external organisations delivering services directly impacting on or related to the portfolio for which the Executive Member is responsible.

[Source: Bracknell Forest Council, Council Constitution, updated August 2024]

Governance arrangements and finance

The next level of understanding of financial governance is to understand how finance is discussed, determined, and delivered within the wider governance system. There are two illustrations below: the first is a simplified cabinet-based governance system, and the second is a simplified committee system. For any governance system ask yourself, ‘how is financial information provided? Who is it provided to? When? How does the budgetary cycle fit into the political management arrangements? Who can challenge on financial issues?’

A system-wide analysis highlights the role that other councillors can play, for example:

- the full council is the sovereign body of a council, and all councillors have a role in debating and agreeing the budget and policy framework

- the 'overview and scrutiny' function in a council with the cabinet governance model (or in a committee system which contains an overview and scrutiny function) is a statutory function which has the power to scrutinise a council's finances and budgets

- audit committees have a role in providing independent assurance on the integrity of the financial reporting and governance processes

- opposition parties will often seek to contest and challenge council finances and budgets and, sometimes, propose alternative budgets

Challenge 3 – Mapping your political management system and the link to finance

Step 1: Council-wide map

Produce your own ‘map’ or illustration of your council’s governance arrangements in relation to budget-setting, monitoring, and assurance.

Then spend some time considering the following questions:

- Where does ‘finance’ sit in your political management arrangements?

- What are the specific roles of the different parts of the governance system in finance leadership and management and financial assurance?

- What works well? What doesn’t?

- How do ‘decisions’ work through the system? Who is involved? What is the balance between member and officer involvement? How are finances assessed, reported, and challenged at different points in the decision-making process? Where does challenge come from?

- What future changes might impact on the governance of finance?

Step 2: Portfolio-specific map

In Step 2, consider how the map works in your portfolio or service area. You may want to add more detail to your map or to produce a second portfolio specific illustration.

Then consider the following:

- How do issues relating to your portfolio or service finances and budgets flow through the political structures?

- What works? What does not?

- Could improvements be made?

Step 3: Analysis and actions

The final step is to consider:

- What have you learned by undertaking this challenge?

- What improvements could be made?

- What actions and next steps could be taken?

Officer roles and responsibilities

To perform their financial responsibilities successfully, the non-finance portfolio holder or committee chair needs to understand the roles and responsibilities that officers perform in this area. This means exploring the world of the finance officer – both the corporate finance officer and the finance officers who directly support financial management in your portfolio or service areas. How corporate and service finance is structured can vary between authorities, so it is always useful to ensure you understand exactly who carries out the different roles.

The role of the responsible financial officer (also known as the Section 151 officer)

While Section 151 of the Local Government Act (1972) makes clear that the council is responsible for the overall financial administration of the council, the requirement that councils “secure that one of their officers has responsibility for the administration of those affairs” is crucial in every council to discharge this responsibility effectively. Therefore, every council will have a named 'responsible financial officer' who is central to the way the council seeks to govern its finances.

Section 113 of the Local Government Finance Act goes further to require that this officer is a qualified member of one of the accountancy institutes, for example, the Chartered Institute of Public Finance and Accountancy (CIPFA). Therefore, every council’s 'responsible financial officer' is also known as the 'Section 151 officer'. This person is usually the head of the council’s finance function and is central in:

- providing effective financial advice to councillors and officers

- organising and maintaining a sound system of financial governance and control

- ensuring that the council follows all its legal duties in financial matters.

In some authorities, the Section 151 officer might report to a strategic director who has a wider role in corporate services. In others, the Section 151 officer might report directly to the chief executive. It is important to understand your local authority's particular structure and to be clear about who, among senior officers, is particularly influential regarding financial matters.

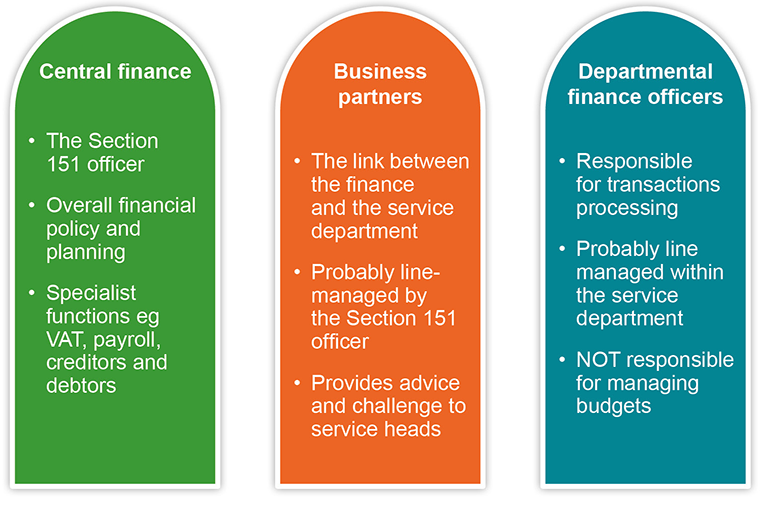

The finance function – a dual role?

The culture and approach of council finance functions has changed over recent years to the extent that most now have a ‘dual role’: that is, the traditional ‘finance police’ role which establishes and enforces financial discipline, as well as a developing role as a ‘finance critical friend’ who can act as an enabler – supporting, encouraging and explaining. A good question to ask yourself is: ‘What’s the culture of the finance department?'.

The finance function – organisation

The finance function is organised into three basic elements:

- the central finance function, usually headed up by the Section 151 officer, which leads on overall financial policy and planning and provides specialist advice on technical areas such as VAT

- the ‘finance business partners’ who support individual services and provide advice to heads of service

- departmental finance officers who are responsible for processing transactions and administering service budgets.

It can be useful to understand:

- what is the exact terminology used in your council and what does it mean in reality?

- where are officers physically located and who line manages whom?

Relationships between corporate finance (particularly in the ‘finance police’ tradition) and service managers does vary and can get ‘tricky’ at times. Traditionally the relationship between corporate finance and the ‘big spending,’ demand-led services can be difficult to negotiate – in a similar way to Her Majesty's Treasury and central Government departments.

All local government managers – including directors, heads of service and departmental management teams – and, in particular, senior officers have an integral role to play in finance. Managing services has to involve managing budgets and understanding cost and demand pressures. However, in certain demand-led services, effectively managing budgets can become challenging. What types of services does your portfolio or service area cover? Are these services in which costs and demands are relatively stable and predictable over time? Are there specific Government grants of longstanding, or is finance supported by unpredictable short-term funding sources? Are fees and charges relatively stable over time?

What you should expect from your officers in relation to finance

Understanding what can be reasonably expected of officers is often unclear to portfolio holders or committee chairs. We recommend that you tackle this head-on by arranging what we call a ‘sit-down’ with your portfolio or service lead officer/s. This can be undertaken relatively early if you are new to the role or, if you are not, you could use other reasons to initiate this discussion. For example:

- you have identified undertaking your financial governance roles as a development issue

- an upcoming budget discussion in cabinet or committee has prompted you to think more deeply about your role

- you have just completed this workbook.

Guidance

The 'sit-down' meeting

To arrange a 'sit-down':

- arrange a face-to-face meeting with your lead portfolio or service officer/s

- explain beforehand that you want to understand what is expected of you in relation to portfolio finances and budgets

- explain that it would be helpful if part of the discussion could:

- outline how portfolio finances are managed between the corporate finance team and the portfolio services

- describe the type of financial information that will be provided to you and when

- provide an overview of key financial pressures and opportunities related to your portfolio/ service area

- allow for discussion about the boundaries of the portfolio holder / committee chair / senior officer roles

- negotiate the shared roles.

Your 'sit-down' meeting will provide an opportunity to discuss and clarify mutual expectations, set out how and when finances will be discussed, and what you as a cabinet member or portfolio holder want to assure yourself of (and vice versa).

Reasonable expectations in this area would include:

- access to timely and accurate financial information

- financial information that is ‘fit for purpose’ – that is, that it allows the portfolio holder / committee chair to perform their financial roles

- regular, scheduled meetings to include discussion of finance and budgets

- a willingness to talk honestly and collaboratively about financial pressures and opportunities

- a mutual understanding of the respective roles of leading councillors and senior officers in relation to financial matters (and more widely) – clarity over how to distinguish separate roles from shared roles

- a willingness to provide access to service officers below the senior level on financial issues, for example, inclusion of finance business partners or departmental finance officers in meetings or briefings where appropriate

- service officers who understand both the service pressures but also financial pressures and the importance of robust financial planning and management.

We recommend that you work collaboratively with senior officers, seeing the relationship as a partnership bringing together different, but complementary, experiences, values, and skills.

Challenge 4

Working effectively with officers on finance

Reflect on your interaction with officers on financial issues, and ask yourself the following questions:

- What has been the quality of the support you have received? What works? What does not?

- Who do you go to for financial advice? The portfolio service director? Finance business partner?

- How could officer support and advice be improved?

- What actions could you take to improve your interactions with officers?

Further reading

- The Chartered Institute of Public Finance and Accountancy (CIPFA) is highly influential in the world of local government finance. CIPFA's publication – The role of the chief finance officer in local government – is useful in explaining what you should expect from the council’s Section 151 officer.

- CIPFA's Financial Management Code (FM Code) supports councils to demonstrate that they are meeting legislative requirements in their overall legislative requirements. Every council is required to comply with the code, and it would be useful for you to speak with your resources portfolio holder/ committee chair (or Section 151 officer) to understand how your council has assessed its financial governance arrangements against the code – and whether any improvements have been suggested.

The importance of the budget

An overview of the financial planning process

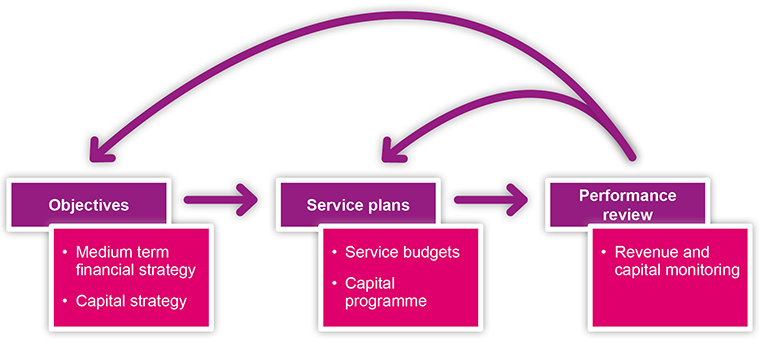

The figure below illustrates the way in which every council seeks to manage and monitor its finances to ensure that services are delivered both effectively and within budget. Councils operate a two-stage budget-setting process.

First, a high-level view of the council’s future finances is constructed which, for revenue income and expenditure, is known as a medium-term financial strategy (MTFS) – or, in some councils, as a medium-term financial plan. An equivalent high-level document for capital income and expenditure is also constructed, known as the capital strategy.

Second, the council will use the above documents to construct an annual budget – both for revenue and capital income and expenditure – in individual departments and the council as a whole for the forthcoming year.

Once the budget is set, the council will monitor income and expenditure against the budget (see the section on 'Monitoring spending and income against the budget' below). It is vital that the finances of the council are integrated within the wider policy and performance management framework (see the section on 'Integrating finance with wider service performance information' below).

Constructing the budget

All councils, regardless of their political governance arrangements, are required to have a 'balanced and robust' budget for the forthcoming financial year which leaves the council with adequate reserves for the future.

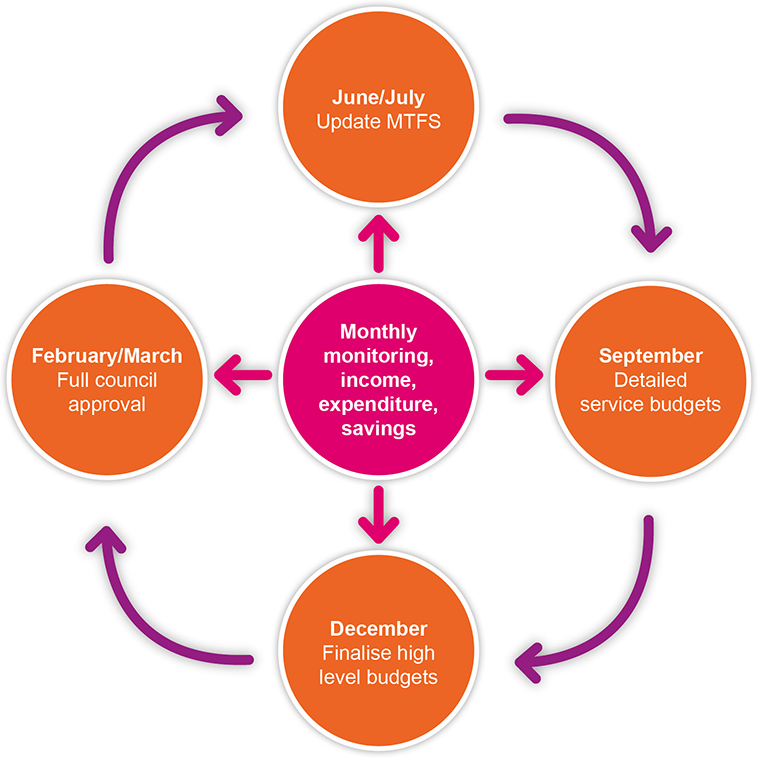

As demonstrated in the figure below, the financial planning process carries on throughout the year. In an ideal world, however, councils look to update their medium-term financial strategy (MTFS) each year in the early summer, using this high-level update to commence the detailed budgeting required in the autumn for the next financial year. In councils with the cabinet system of governance it is good practice to involve scrutiny in reviewing budget plans at an early stage. Once the local government finance settlement has been announced (usually in mid- to late December), the draft budget is then further subjected to the scrutiny process, leading to a cabinet recommendation to full council in late February or early March.

While the above diagram appears to show that elected members have their say towards the end of the budget-setting process, portfolio holders and committee chairs should be proactively driving the budget formulation in their portfolios / service areas from the very start of the process. The following sections look in further detail at how councillors can do this.

Updating the medium-term financial strategy (MTFS)

The medium-term financial strategy (MTFS) summarises the likely income and expenditure planned by the council over a three- to five-year period. While this is a corporate document which might only deal with an individual portfolio or service area in a single line, it should be derived from similar, more detailed financial planning work at portfolio or service level. While the nature and form of what might be termed 'portfolio MTFS' documents vary, there should be a clear link between the corporate MTFS and the medium-term financial planning undertaken at portfolio or service level. This is likely to contain elements of both a top-down and a bottom-up approach, as outlined below.

Top-down

Projections of the council’s likely income from corporate sources such as Council Tax, business rates, and any Government grants, will be provided by the Section 151 officer to enable the council to consider its medium-term financial position in the light of such corporate constraints. It is unlikely that such figures can be challenged by individual portfolio holders or committee chairs. However, councils are also likely to provide what might be considered as corporate rules and guidelines for individual areas to use as they consider their budget requirements. For example, a corporate inflation rate to be used for all salary calculations is likely to be provided. Such corporate guidelines and rules should be reviewed by individual portfolio holders and committee chairs, with the assistance of officers – in particular, the finance business partner (or equivalent) – to ensure that they adequately reflect the needs of the service moving forward. It is also likely that other portfolio-specific guidelines will need to be established, for example, any specific inflation indexing that has been agreed in service-specific contracts.

Bottom-up

It is important that the corporate MTFS is as accurate and complete a document as possible and so it is essential that there is good communication between portfolio / service areas and corporate finance. To illustrate this, some councils provide a corporate assumption on the overall increase in fees and charges income for forthcoming years but leave specific fees and charges increases for the portfolio / service area to decide upon. Others provide a detailed list of every fee and charge levied at the council in an appendix to the overall budget papers.

However, the medium-term financial strategy (MTFS) is updated, individual portfolio holders/ committee chairs need to ensure that they are proactively involved in the MTFS update and annual budget proposals that eventually find their way to full council for approval. This will involve early, and possibly detailed, discussions with service officers to ensure that the MTFS projections – and, crucially, the annual budget for the forthcoming year – are sound both in terms of policy direction and deliverability.

Challenge 5

The medium-term financial strategy (MTFS)

Spend some time reviewing the information you receive from officers concerning the update of the MTFS. You should easily be able to find a cabinet paper that seeks approval for the new MTFS, but this will be at corporate level and is at the end of the process.

Reflect upon how involved you are in the actual updating process in your service area:

- Is there a process for updating the MTFS at service level? If so, how involved are you in this process?

- Is there a document that could be seen as a 'service MTFS'? If not, how does the service provide these numbers to be included within the corporate MTFS?

- Do you have discussions with service directors and the finance business partner as they prepare the update?

- How could you be more proactive in the MTFS update process?

Capital strategies and plans

Most councils own large portfolios of land, buildings and other assets which are integral to public service delivery. Therefore, your council should also have established processes to review the assets it owns in an asset management strategy which, in turn, informs the financial aspects of the council’s capital strategy and capital programme.

While all of the documents mentioned above are corporate documents, they should be derived from departmentally based strategies and plans covering in more detail the capital assets that are used by the service department (for example, the leisure centre building will be the responsibility of the leisure and culture department).

In our experience, councillors are less involved in the formulation and management of capital strategies and plans than their revenue equivalents, which is surprising given how important assets are for effective service delivery. It is essential that capital spending plans are policy- and priority-led in a similar way to the council’s revenue activities.

Challenge 6

Assets and capital spending

- What information do you receive as a portfolio holder or committee chair in relation to the assets your department uses in delivering its services?

- How involved are you in the formulation of future capital spending plans?

- How could you be more proactive in this area?

The annual budget-setting process

While councils regularly update and review their MTFS as good practice, local government law remains based around a detailed annual budget for the forthcoming year. Therefore, each council will utilise information in their MTFS to prepare a detailed annual budget for every aspect of the council’s income and expenditure. Once approved by full council, the authority to spend against the budget will be delegated down to individual officers who are specifically designated as budget-holders – these will usually be heads of service.

Constructing the annual budget is a complex process, but it is important that portfolio holders/ committee chairs retain an overview of the detailed budget decisions being made by officers, as the budget amount will have consequences for service delivery for the forthcoming year. To gain and maintain a strategic overview of the annual budget-setting process, you will need to understand both how the annual budget is being constructed in your portfolio/ service area, and specifically focus on any significant changes that are being proposed in next year’s budgets by way of new budget growth and savings. We will look at each of these in turn below.

Budget construction tools

While portfolio holders / committee chairs should leave the detailed work to officers in order that those councillors retain a strategic overview, it is useful for portfolio holders/ committee chairs to understand how a budget is constructed. Councils tend to use a combination of three tools when constructing the next year’s budget – and each tool has advantages and disadvantages.

Incremental budgeting (Tool 1) effectively 'rolls over' last year’s budget (the base budget), making any necessary adjustments to it in terms of matters such as inflation, new money for new responsibilities, and / or service savings. This is probably the most straightforward of the three tools used and has the advantage of being relatively easy to undertake. However, it has the significant disadvantage of not challenging whether spending and income budgets in the past were appropriate and sustainable for the forthcoming year. Clearly, this tool is not appropriate where the service has been subject to any significant reorganisation or change which has made the current budget inappropriate for the new service.

Zero-based budgeting (Tool 2) is in effect the exact opposite of incremental budgeting in that it does not roll over last year’s budget but starts from scratch (a zero base) every year. This is a very powerful budgeting tool that enables a fundamental review of the budget in accordance with what is required from the service in terms of service output and outcome and can be used to good effect during service transformation projects or as a more fundamental review of a service. However, the amount of time and effort that is required to undertake such an exercise should not be underestimated and it is impractical to use this tool annually throughout the council.

Priority-based budgeting (Tool 3) seeks to ensure that budgets are set to ensure that a service area is resourced to deliver its priority areas, with any budget savings being made in areas that are considered lower priority. As the portfolio holder/ committee chair, you will wish to ensure that the council’s priorities for your service area are appropriately resourced and so you may wish to employ this tool when working with officers in constructing the budget. However, councils are complex organisations and so it is unlikely that it will be possible just to prepare a list of priorities, starting at the top of the list and resourcing each priority individually until the money runs out.

Challenge 7

Constructing budgets

- Have a conversation with your service director and finance business partner about how detailed budgets are constructed in your service area.

- Can you see the three tools mentioned above being used?

- How could the tools be practically employed more effectively to make the budget better in terms of policy and service aims and objectives?

Identifying and approving budget savings

The pressure on local council budgets in terms of increasing service demand and the limitations on the council’s ability and scope to raise income means that most councils have processes to identify areas in the budget where savings can be made. Elected members will be very aware that it is these savings proposals that tend to be the most controversial parts of the budget-setting process and so it is essential that leading councillors are actively involved in the savings identification process as early as possible.

Savings can be made in two ways. First, money can be saved by becoming more efficient in the way services are structured and delivered. These tend to be relatively uncontroversial as the service remains largely the same, but it should be noted that after over a decade of budget constraints, the scope to make further efficiency savings might be limited. This means that many councils are relying more heavily on the second type of saving which requires more fundamental rethinking and redesigning services (sometime known as service transformation) or simply by reducing service provision. These services are clearly more fundamental and potentially more politically problematic.

Councils usually have established processes for identifying savings. Some have special working groups (sometimes known as 'star chambers') where budget proposals are challenged prior to them being included in the draft budget proposal, usually by councillors (and sometimes officers) from outside the service area under review. Others use the scrutiny process to review proposals. Whatever the approach at your council, as portfolio holder or committee chair, you should be involved not only in the review process but also early in the way that savings (and new projects) are developed. Indeed, you may well wish to put forward savings and new project proposals proactively yourself.

While the budget must be balanced, it is clearly not enough for a leading councillor to just have a final review with a right of veto on a list of proposed savings identified by officers. Rather, they should be proactive both in making clear the political and policy aspects of savings (including any savings that are totally politically unacceptable) as well as suggesting potential areas of savings themselves.

Challenge 8

Identifying and approving budget savings

Spend some time reviewing the way your council prepared its budget proposals for the last financial year.

- How involved were you as a portfolio holder / committee chair in constructing the budget for your service area?

- How were savings identified, how was any new money allocated? Did officers simply provide you with a list of potential savings and ask for your views or were you involved in the development of savings and new growth plans?

- Then think and plan how can you be more proactive in the identification of savings. Powerful questions might include: How do we know that we are currently allocating our budget in accordance with established priorities? What are the risks in doing what we propose to do, how can these be mitigated? What are the longer-term effects of next year’s budget likely to be? Could we achieve the same outcome more cost effectively by organising services in a different way?

Monitoring spending and income against the budget

The previous sections have explained the importance of the council budget. Once the budget has been approved by full council, it is equally important that income and expenditure is monitored regularly to ensure that it is in accordance with the budget.

While detailed budget-monitoring is an officer activity, it is important that portfolio holders / committee chairs maintain political oversight and can contribute to any corrective action that is required should service finances deviate from the approved budget.

The budget-monitoring process

Every council has detailed and well-established processes to monitor spending and income against its budget. The figure below illustrates a typical budget-monitoring process.

The approved budget is uploaded to the council’s financial system in a way that generates a detailed budget for each service. The council’s financial procedure rules and regulations delegate responsibility – to specific officers known as budget managers (usually heads of service) – for managing each service's financial activity, including monitoring income and expenditure against the delegated budget.

The financial system will provide regular budget-monitoring reports to the budget manager, sometimes on a real-time basis, to enable effective control. Most councils have a formal monthly process where budget managers are required to:

- review their spending

- consider how they are progressing against the budget

- provide their forecast of likely income and expenditure to the end of the year.

While the finance business partner and service finance staff will be actively involved in the provision, analysis, and challenge of this information it is important that all such information, and in particular the forecasts, are owned by the budget manager. Put simply, the best person to manage a budget is the person closest to the actual spending decisions.

Usually, officers will provide the cabinet or service committee with regular update reports on the overall budget situation, together with information on the reason for any significant variances and details of any corrective action that is proposed to bring things back to budget. This report should also be available to the scrutiny function for their consideration. Such reports are taken to committee either quarterly or, possibly, monthly. However, this is usually at a high level and so individual cabinet members/ committee chairs and vice chairs should expect to receive more detailed reports on the budget situation for their service areas.

While it is important that portfolio holders / committee chairs maintain a strategic overview of budget-monitoring issues rather than finding themselves too involved in the detail, they should receive the information they need to maintain a strategic overview of their service areas, have an opportunity to discuss progress with senior officers and have an input into any corrective action that is necessary. Such information will enable leading councillors to answer the following questions:

- Is the service area broadly operating as expected in accordance with the approved budget?

- What are the key areas of forecasted over and under-spending?

- What are the implications for the delivery of policy and priority areas?

- Are approved savings being delivered in accordance with the plans established at budget time?

- If not, are officers proposing alternative ways of making savings?

- What are the policy and service implications in such alternative plans?

Capital budget-monitoring

Given the importance of the capital budget, it is just as important that the council monitors performance against its capital budget as it does with its revenue budget. However, in our experience, councillors receive less information on this area.

As a portfolio holder or committee chair of a service area with projects in the capital programme, you should ensure that you receive regular, certainly quarterly, updates on the delivery of capital projects against the budget, together with the reasons for any over-spending or slippage in the plan. These reports should also make clear if there are implications in the revenue budget due to slippage in the delivery of the capital budget.

Challenge 9

Assets and capital spending

Spend some time reflecting on the way budgets are monitored and reported at your council.

- Apart from the overall budget-monitoring report that is discussed at Cabinet/ committees, what other information do you regularly receive from officers that is at a more detailed level for the services in your portfolio/ service area?

- Are these reports adequate and enable you to discuss with senior officers how things are progressing?

- Do these reports detail both revenue and capital aspects of the portfolio?

- What do you do with these reports? How proactive are you in understanding and responding to the issues raised?

Integrating finance with wider service performance information

Section 3 of the Local Government Act (1999) requires all councils to “make arrangements to secure the continuous improvement in the way in which its functions are exercised, having regard to a combination of economy, efficiency and effectiveness”. This is defined as ‘best value.’

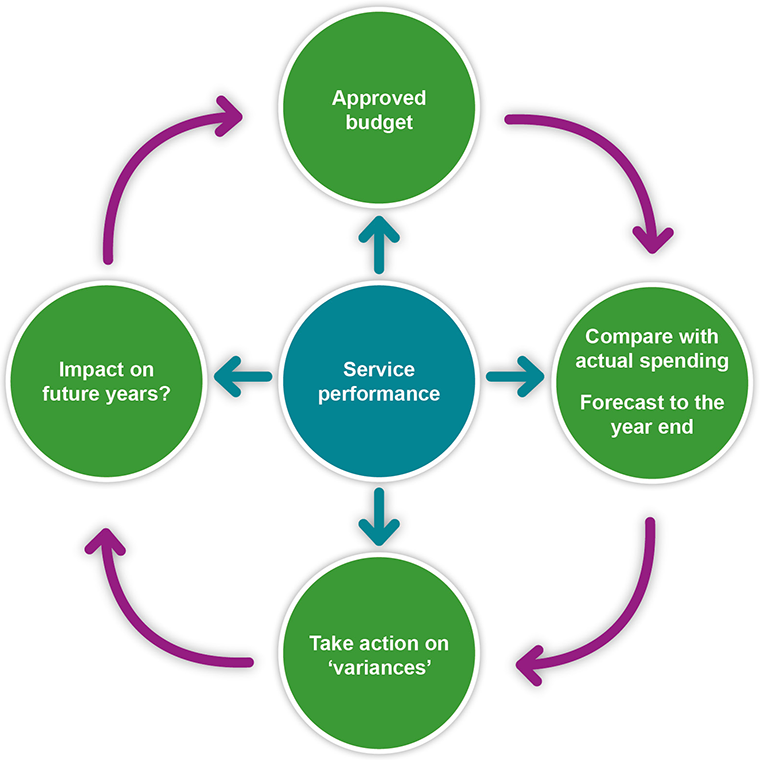

While the ways in which councils fulfil and report on best value vary, the basic principles remain the same – councils need to ensure that the services they provide offer best value in relation to the money and other resources used to deliver them. This can be illustrated by returning to the figure we used at the start of this workbook to describe the financial management process, and then overlaying what might be considered as the 'performance management process'.

US President Joe Biden is quoted as saying: “Don’t tell me what you value, show me your budget, and I’ll tell you what you value.” This illustrates the importance of making sure that budget and spending decisions are fully in line with wider policy priorities.

The portfolio holder/ committee chair has a key role in this process and, so, it is essential that you receive relevant and timely performance information not only on the financial performance of your service area, but also any related information on service achievement, output, outcome, and risk. Ideally, such performance information should be integrated, enabling a view to be taken on both finance, risk and service performance in the same document or report. Such integration is vital to effective decision-making.

If finance, risk, and service performance information are provided separately, you are only considering part of the picture.

Performance information is at its most effective when users can monitor progress both over time and also in comparison with other councils. Portfolio holders and committee chairs should look to their officers (especially service directors) to be able to provide such comparison information and use it to 'tell the story' of the council's achievements and the challenges it faces. Our free data benchmarking platform – LG Inform – collates all the various performance data councils provide to government, presenting the information in a manner that is easy to understand and which enables performance to be compared with other councils. This can be accessed at http://vfm.lginform.local.gov.uk/

How finance interacts with service delivery

Accountants use the phrase 'cost behaviour' when considering the relationship between the cost of a service and service performance. While it is best to leave officers to undertake the detailed analysis, it is useful for councillors to have a basic understanding of how cost (and income) varies as service provision changes when reviewing and challenging such information.

Some costs will increase and / or decrease directly in line with service activity. These are known as 'variable costs'. For example, the budget for building repairs will increase or decrease in line with the number of repairs that are undertaken.

Other costs do not vary with service activity and are, therefore, known as 'fixed costs'. For example, the council will need to pay business rates, and possibly rent, on the premises it uses. The level of rent will be the same, regardless of how much the building is used.

Officer salaries are an interesting case. Strictly speaking, salaries are variable costs as the budget will rise and fall depending on the number of staff on the payroll. This is certainly true for those on agency- or consultancy-style contracts. However, certainly in the short term, the budget for permanent staff might be considered as a fixed cost as there will always be a delay in either new recruitment or while the council goes through the required procedures for severance and redundancy.

The same can also be true for some sources of income but this tends to be known as “price elasticity of demand.” The introduction or increase in the charge for a service is likely to affect the number of users of the service and so both variables need to be considered during any review of fees and charges.

Understanding the way costs behave as service performance changes can be very useful when reviewing budgets and considering transformation and other service changes. For example:

- A large metropolitan council has noted that the increase in the cost of fuel has caused an overspend in the budget for fuelling the council’s fleet of refuse freighters. Fuel is a variable cost. The council is now increasing its efforts to introduce electric or more fuel-efficient vehicles into the fleet, so the increased fuel efficiency can offset the rise in the cost of diesel

- A district council increased the charge for its green waste collection service at the beginning of the year but was concerned that the increase in price would result in lower uptake of the service. However, they were pleased to find that no such reduction took place. In fact, the communications work the council undertook to explain the new charge to residents resulted in increased service usage

- A city council has recently experienced overspending in its budgets for housing homeless people. This can be directly attributed to the increase in the number of people using the service

- Many councils report sometimes substantial under-spending in their capital budgets. This is typically because various projects have not progressed during the year. The under-spending (which is usually reported as slippage) is due to reduced service delivery and activity rather than efficiency

Councils provide complex services and so cost behaviour can also be complex. However, as a portfolio holder / committee chair, you should receive information from your officers on such issues when considering service performance. As a principle, as the portfolio holder or service committee, you should resist making any decision that might affect either the budget or service performance without first understanding the interaction between these two variables.

Challenge 9

Assets and capital spending

Review the information you receive as portfolio holder (and more generally as a member of cabinet) or committee chair and reflect on:

- How useful is this information for demonstrating that your council provides best value?

- How integrated is the information you receive on the finance and budget of your services with wider performance information on service delivery and outcome?

Review the latest budget-monitoring information for your service area.

- Can you easily find information on both the variation in budget and the consequent change in service delivery?

- How well do the reasons provided for budget over and underspends enable you to understand cost behaviour in the various services under your portfolio?

Finally, reflect on how involved you are in best value and budgetary control decisions.

- How could you ask the right, strategic questions without becoming bogged down in the detail?

Conclusions

In order to be effective, every portfolio holder or committee chair needs to understand the finances of their service area.

While finance can be a daunting subject, it is hoped that this workbook has provided you with the understanding and tools you require to effectively consider the information and advice provided to you by officers.

In summary, the effective portfolio holder/ committee chair will:

- Be proactive – rather than reactive – in considering financial matters

- Provide a policy and political lead perspective on your service area's finances, rather than just reacting to information provided to you by officers

- Become a champion for integrated finance and service performance information, to ensure that officers and councillors alike are making decisions based on the best information available

Glossary of terms

base budget

– starting point for the construction of next year’s budget (this is usually the budget for the current financial year, which is rolled forward to the next financial year and then adjusted as necessary to reflect inflationary and other pressures)

best value

– legal duty introduced in the Local Government Act (1999) that requires councils to make arrangements to continuously improve the way in which its functions are exercised and to have regard to a combination of economy, efficiency, and effectiveness

budget manager

– nominated officer who has responsibility for managing spending and income against the approved budget for a service (this responsibility is set out in a council’s financial regulations and is usually delegated down from councillors to service directors and heads of service)

capital expenditure and income

– expenditure and income allocated to creating and / or improving a council’s assets, including its land and buildings (capital is legally separate from the council’s revenue activities and so there will be separate processes for allocating and controlling capital budgets)

capital programme

– approved capital budget which usually covers a period of between three and five years, but which is updated annually as part of the overall budget setting process

capital strategy

– council-wide document which sets out a council’s approach to managing its capital assets and spending plans and which is, usually, reviewed annually and reported to full council as part of the annual budget setting process

finance business partner

– A finance professional who provides strategic financial support to a particular council department or portfolio. They will probably report to the Section 151 Officer but will be part of the Departmental Management Team (or equivalent) While not all councils use this term, every council service area should have financial support available to it in the form of advice, support, and challenge on the service area’s finances

local government finance settlement

– annual announcement by the Government of the amount of grant funding to be provided for the forthcoming year (a provisional settlement is usually announced in mid-December, with the final settlement confirmed in mid- to late January)

medium-term financial strategy (MTFS) – known in some councils as a medium-term financial plan (MTFP)

– budget which estimates income and expenditure at a high level over at least three future financial years

reserves

– money set aside to support the overall financial stability and resilience of the council (a council’s savings which provide a financial buffer against financial volatility)

resources portfolio holder

– in a council with the cabinet model of governance, common name for the portfolio holder / cabinet or executive member who has specific responsibility for the council’s resources, including its finances (not every council uses this term but every council with this governance system will have a portfolio holder / cabinet member who has responsibility for its overall finances)

revenue expenditure and income

– day-to-day expenditure and income on a council's running costs (revenue is legally separate from a council’s capital activities and so there will be separate processes for allocating and controlling revenue budgets)

Section 151 officer

– common alternative name for the council’s 'responsible financial officer' – the officer who, by law, every council must designate as having legal responsibility for providing effective financial management and advice across the council and who must be a qualified member of one of the UK's main accountancy bodies

slippage

– term used in capital budgeting to indicate that planned expenditure (or income) has not been incurred in a period and is now anticipated in a future period, mostly because there has been a delay in the project itself.

Appendix: Month-by-month checklist of financial activity – when to expect what information

This checklist is designed to give you an example timeline of a council's key finance and budgeting activities. Advice and support can be found in the LGA’s guide to the annual budget process.

Please note that different councils have different reporting structures and timetables, but these are likely to follow something similar to the generic timetable set out below. Notes have been provided to give further details on the role of the portfolio holder/ committee chair at each stage.

April

Financial activities this month

- April marks the start of the new financial year and is generally a quiet month

- Your finance department should have uploaded your council's approved budget onto your financial management system and provided budget holders with their approved budget for the forthcoming year

- The finance department will also be very busy closing last year’s accounts and starting the process of preparing the annual financial statements for the previous financial year

Notes

- You should ensure that every service within your portfolio/ service area has started the year with a clear indication of its budget

- It is almost certain that the budget will not be sufficient for service managers to do everything they want to do. Because of this, it is helpful to ensure that any risks have been identified and suitably mitigated

May

Financial activities this month

- Around this time, look out for your council's 'out-turn report', which will contain the latest update of your council’s financial position and reserves going forward and which will be reported to your cabinet or resources committee

- As a portfolio holder/ committee chair, you should receive a detailed report on the out-turn for your area of responsibility/ service area containing information on spending and income in the previous financial year and how it compared to the budget

Notes

The out-turn report:

- will provide information on how your council performed against its budget in the previous financial year

- should contain no surprises – any issues should have been highlighted and acted upon during the year

- provides the most up to date information on the council’s financial position and so is worth reviewing for issues that may impact on your service area’s financial planning for the current year and future years

June

Financial activities this month

- During June, senior officers and the resources portfolio holder/ service committee are likely to start thinking about rolling forward the council’s medium-term financial strategy (MTFS) and the next year’s budget

Notes

- Be aware that planning for future budgets has already started.

- As portfolio holder/ committee chair, ask yourself how are you going to lead the development of high-level future budgets to ensure that best value is delivered alongside your policy priorities?

- Have you agreed with officers a process for the preparation of the budget which allows sufficient opportunities for member involvement and scrutiny?

July

Financial activities this month

Look out for the 'Quarter 1 performance report' being reported to your cabinet or resources committee this month. Performance reports compare service performance and financial performance against the budget and should be sent to councillors each quarter

Notes

- What more detailed information have your received from your service area on how budgets are progressing?

- What opportunities have you had to proactively lead any work that is necessary to ensure that services are delivered effectively and within budget?

- While there is still a long time to go, does the Quarter 1 performance report highlight any areas of concern for your portfolio’s finances or performance?

September

Financial activities this month

- September heralds the start of the detailed budget-setting process for the next year. There is a wide variation between councils as to how and when this is reported to elected members (and, therefore publicly), so be prepared to monitor the agendas of your full council – and your cabinet or resources committee – over the next few months

Notes

- While it is best to leave officers to undertake the detailed budgeting, how are you going to lead this process? How are you going to ensure that policy and political priorities are addressed in next year’s budget?

- The budget-setting process is likely to involve a process for identifying potential budget savings for future years. How are you going to be proactive in identifying savings? Are officers being clear on the possible effects on service delivery on the savings that are being identified?

October

Financial activities this month

In October, look out for the 'Quarter 2 performance report' being reported to your cabinet or resources committee. Performance reports compare service performance and financial performance against the budget and should be sent to councillors each quarter.

Notes

- Forecasts of likely spending and income for the financial year should be becoming a lot firmer in the Quarter 2 performance report. Is everything going to plan? Are approved savings being delivered? Are there any unintended consequences that need to be highlighted?

- Don’t forget capital! What information are you receiving about how the capital programme is progressing for your service area?

November

Financial activities this month

- In November, the Government usually publishes its updated Spending Review. Even though local government is usually consolidated into one line of this review, the information may indicate what resources might be available to councils over the coming years

- Many councils conduct a formal budget consultation process with the public around November

Notes

- By now you should have received detailed information about the budget for your service for the forthcoming year. Are you content that the proposed budget will deliver services efficiently and effectively? Have risks been identified and mitigated?

December

Financial activities this month

- In December, the Government publishes the 'local government finance settlement'

- Your council's senior finance officers will receive indications from Government on the amount of government grant and Business Rates assigned to your council for the forthcoming year

- This process also confirms the rules on Council Tax increases and referendum limits for the forthcoming year

- Depending on how late the Settlement is made available, some councils may report draft budgets to cabinet and scrutiny committees in December. However, this is more likely to happen in January (see below)

Notes

- In December, budget papers should be discussed by your cabinet or resources committee. How are you going to act as a political champion for your service areas?

- Don’t forget that a budget for capital income and expenditure must be set as well. What information are you receiving on your service’s capital programme and budget for the forthcoming year?

- How can you utilise the scrutiny process (or the discussions held at committee meetings) to further improve the budget or service delivery plans?

January

Financial activities this month

- In January, look out for the 'Quarter 3 performance report' being reported to your cabinet or resources committee. Performance reports compare service performance and financial performance against the budget and should be sent to councillors each quarter. Please note that this might form part of the budget report

- Budget reports and medium-term financial strategy (MTFS) updates will be reported to your cabinet or resources committee for approval around now.

- Councils with overview and scrutiny committees will report the draft budget to committees in January This is likely to include detailed scrutiny of the savings proposals contained within the draft budget

Notes

- By Quarter 3, forecasts of spending and income to the end of the year should be reasonably accurate. You may wish to reflect upon how identified budget variances and challenges have been managed by officers during the year. Has it been able to bring things back on budget? If so, how proactive have you been in the various solutions that have been found?

February / early March

Financial activities this month

- Most councils will hold full council meetings in February (or very early March) to approve the budget and Council Tax for the forthcoming year

Notes

- While it is likely that your council's leader and / or resources portfolio holder will recommend the budget to full council, as a portfolio holder/ committee chair you should be confident that you have had the opportunity to be proactive in the budget-setting process and that you look to the new financial year understanding the risks and challenges your service areas face in delivering services within budget

- Reflect upon what your political priorities are for the forthcoming year and make sure that these have been communicated to your service director and other senior officers. You could choose to develop with them a series of key performance indicators (both financial and non-financial) that you can all monitor during the year to ensure that everything remains on track

Further information and support

- Our website at local.gov.uk is an invaluable source of help and advice for all those in local government. Our Finance and business rates topic webpage provides a wealth of information, including useful publications and case studies. Our Finance improvement support webpage includes information about support and guidance on this subject, including a ‘must know’ on the statement of accounts and a guide for audit committees which may be of wider interest

- Good financial management and governance are essential elements of the council’s wider governance and assurance framework. We have produced a councillors’ guide to this framework

- CIPFA (the Chartered Institute of Public Finance and Accountancy) is a useful source of more detailed financial discussion and guidance

- LGIU (Local Government Information Unit) publishes a range of publications – and hosts training sessions and other events – relevant to various aspects of local government finance

LGA training seminars and events

- Our courses on risk management and Finance for non-finance cabinet members leadership essentials provide portfolio holders / leading members with opportunities to explore further details related to the topics covered by this workbook

- What about the Financial Governance 2-part online course and the ‘finance without numbers’

- Further support for elected members on this and other topics can be found on the LGA webpage

- We also offer regular online courses on ‘finance without numbers.’ Details can be found at the following link

Appendix: 10 Key Roles Framework – Self Evaluation

Leadership of Portfolio / Service Committee Finances - 10 Key Roles Framework – Self Evaluation

Notes to complete:

There are two parts to this self-evaluation. Begin by reviewing the ten roles listed and write short notes assessing how well you are undertaking the role and what further actions you could take. Then move on to the second part, which asks you to consider your self-evaluation overall and prioritise key development areas and actions.

| Key Role | Brief explanation |

Self-Evaluation: How well are you undertaking this role? What evidence would you provide to support this? What further actions could you take? When? |

|---|---|---|

| 1.Understand the general picture on local government finance |

|

|

| 2. Understand your own Council’s financial processes |

|

|

| 3. Be adept with your Portfolio - Financial Leadership |

|

|

| 4. Be aware of and understand key portfolio financial information |

|

|

| 5. Be a champion for integration of Finance and Service information |

|

|

| 6. Ensure robust oversight of the financial aspects of major projects |

|

|

| 7. Ensure you have inslght of Income and Commercialisation |

|

|

| 8. Ensure robust oversight of financial risk |

|

|

| 9. Understand the links between Partnership and Finance |

|

|

| 10. Foster effective Relationships with key finance officers |

|

Summary Self-Evaluation

After completing the above consider:

- which of these ten areas do you think you are most comfortable with? Are performing well? Are your strengths?

- which of these areas are you less comfortable with? Are less sure in? or have not yet had the time to develop?

- from the above, what would you consider to be your key development issues/areas? what could you do to meet these development needs? what actions could you take?