Foreword

Ongoing concern about the changing climate is high amongst councils and the wider public. In response to this most councils have either declared a climate emergency or formally debated the issue and expressed their concern.

There is a clear need to act, but we are working against a backdrop of 10 years of austerity and budgets depleted further by the economic impacts of the COVID-19 pandemic. The Local Government Association (LGA) undertook a member survey in March 2020 at which time the overwhelming issue most councils were concerned with when tackling climate change was the ability to fund the measures necessary.

Over the last couple of years, the Government has made a series of announcements which impact green finance for councils. Most significantly these include the establishment of the UK Infrastructure Bank (UKIB), announced in November 2020, the response to the Public Works Loan Board (PWLB) consultation in November 2020 and the Net Zero Strategy in autumn 2021. It will be refreshing its Green Finance Strategy (GFS) during 2022.

The LGA and Local Partnerships have produced this Green Finance Guide to provide both practical guidance and examples of good practice to support councils in England to find the most appropriate and affordable ways to finance their green ambition.

This is an updated version of the guide, originally published in December to provide additional information in relation to the UKIB and updated information on grant funding.

We hope you find this guide helpful and that it will support the delivery of a wide range of local authority projects.

Executive summary

1.1 Background

According to the National Audit Office almost two thirds of councils in England are aiming to be carbon neutral 20 years before the national target and 91% of councils have adopted at least one net zero commitment.

Through its work with its member organisations the LGA is aware of significant pressures on delivery of these targets amongst councils. The most frequently reported barriers were amount of funding (97 per cent to a great or moderate extent), accessibility of funding (94 per cent), lack of workforce capacity (92 per cent), internal skills and expertise (77 per cent), conditions of funding (87 per cent), and reliability of funding (74 per cent).

Since the introduction of the Prudential Code for Capital Finance in 2003, the Public Works Loan Board (PWLB) has been a mainstay of local authority capital programmes. In October 2019, the Government announced a review PWLB: future lending terms aimed at finding proportionate and equitable ways of preventing councils from using PWLB loans to buy commercial assets primarily for yield. The review was followed in March 2020 with a consultation. The outcome of the consultation was published on 26 November 2020, together with revised lending terms aimed at preventing investment purely for yield. A key change introduced as a response to the review required councils looking to access PWLB to demonstrate that their borrowing supports service delivery, housing, regeneration or preventative action. The requirement to limit borrowing to investments directly relating to delivery of public services and the function of the local authority is now embedded in the updated Prudential Code. This means that borrowing must be primarily and directly for public services relating to the function of the local authority, irrespective of whether the borrowing is sourced from the PWLB or any other provider of debt such as a bank, bond issue or investment fund.

The UK Infrastructure Bank (UKIB) was launched in June 2021 and has been lending to its first schemes since Q4 2021, it will be publishing its lending strategy in summer 2022. The UKIB provides access to funding for both councils and private sector organisations. For councils the funds accessed through this source will be cheaper than through PWLB but are only available for larger projects (>£ 5m) which are aligned to the UKIB’s purpose of net zero and local economic growth.

1.2 Central Government

In bringing forward the GFS (GFS) Government has recognised two key objectives:

- to align private sector financial flows with clean environmentally sustainable and resilient growth, supported by Government action

- to strengthen the competitiveness of the UK financial sector.

There are three strategic pillars to the strategy to support these objectives:

- Greening finance – which centres on ensuring climate and environmental factors are integrated into mainstream financial decision making.

- Financing green – where the focus is on accelerating finance for clean and resilient growth and improving access to finance for green investment.

- Capturing the opportunity – which aims to cement the UK’s position as a global leader for green finance and ensure the UK is at the forefront of green financial innovation, data and analytics.

Whilst the GFS is not focused on local authority investment, it signals a clear view from the Government that the UK’s net zero emissions target will not be met without tapping into the significant private sector funding available. The GFS is due to be refreshed in 2022, which may involve more specific commentary in relation to councils and it is likely there will be consultation in the coming months inviting input from the sector.

1.3 Measurement and verification

Green finance refers to the financing of new and existing public and private investments with sustainability objectives. Sustainability objectives include renewable energy and zero carbon energy generation and distribution, energy conservation measures, climate adaptation works, migration of activities away from fossil fuel sources, conservation and sustainable agriculture.

Green finance can take many different forms, including green bonds, green loans, a green revolving credit facility, green hire purchase, green lease and asset loans, green grants and mechanisms to create market certainty.

A key feature of green finance is the need to be able to verify that the project has produced the environmental benefits set out in its original business case. The measurement and verification process can take a number of forms, but all should be clear, transparent and auditable. For some schemes there are national or international accreditations that would be a key part of demonstrating environmental benefit. Where these schemes are not available there is a need to develop clear and auditable measures.

In addition to the audit of the benefits delivery there is increasing focus on the emissions produced during project delivery. In June 2021 the Government introduced Public Procurement Note (PPN) 06/21 (Taking account of Carbon Reduction Plans in the procurement of major government contracts) with the aim of reducing carbon emissions in central government procurement. Whilst PPN 06/21 is not mandatory for councils it provides a useful starting point for an evaluation set and is likely to be a requirement for any borrowing from the UKIB.

1.4 Equity and grant funding

Equity covers both direct capital contributions and the leverage of land and other assets in additional finance. Some councils have access to equity funding from reserves, and property assets can also be used as a form of equity.

In addition to equity and assets there are many potential sources of grant funding. Green grants cover areas as diverse as building energy efficiency schemes, flood adaptation work, afforestation and the installation of electric vehicle charging facilities. Grants are used by the Government either to stimulate growth or a particular activity, or to develop a market prior to full commercialisation.

1.5 Debt funding

Green Finance is often used to refer to debt funding of green investment. In addition to PWLB funding, councils are starting to see the emergence of new funding sources which can compete with PWLB, in particular Community Investment Bonds and the UKIB.

When considering debt funding, councils should consider a number of factors as set out in Table 1 below.

| Form of debt | Cost of borrowing | Borrowing amount | Security | Proposed due diligence | Comments |

|---|---|---|---|---|---|

| Public Works Loan Board | Depends on lending term. 25 Year Annuity Rate at around 3% in April 2022 | 100% | Lending against revenues of the local authority |

Extensive board and council member approval process for project.

The PWLB application process is currently deliberately permissive but requires submission of a three year capital plan and s151 officer sign off that borrowing does not include projects primarily for yield. |

Borrowing cannot be primarily for yield and must support local authority objectives in service delivery, housing, regeneration or preventative action. (Although this requirement is also applied to any lending not sourced from PWLB and can impact a council’s ability to borrow PWLB in subsequent years for other purposes if it is not adhered to) |

| UK Municipal Bond Agency (UKMBA) | Highest costs are similar to PWLB, with lowest being around 50bps above gilts (currently 2.5% to 3%) | £ 250m+. The UKMBA will aggregate the requirements of several councils and the sum can relate to delivered projects and future requirements | Against the covenant strength of the local authority. Single authority bonds will require a credit rating score. Pooled bonds require a credit assessment (not published as a rating) | Due diligence focus around the financial standing of the local authority. |

Bonds can be expensive and time consuming to put in place, but potentially provide access to long term cheap debt. Shorter term ‘note’ arrangements can be provided for interim finance whilst a sufficiently large pipeline is developed. Minimum size for pooled investments is around £5m for a local authority. Green reporting / verification is tailored and works to utilise existing criteria. |

|

Green lenders

|

Most expensive form of lending at rates equivalent to private sector projects | Typically, up to around 80% of a steady state project | Lending against the project assets | Extensive technical, financial and legal due diligence undertaken by green lender. |

As for PWLB, in addition green loans are likely to be specific to both the local authority and the project. Most likely applicable to joint venture or more commercial projects |

| Crowdfunding/ Community Municipal Bond (CMB) | Potential to provide capital on terms which are equal or better than PWLB – currently around 3% at April 2022 | Potential for 100%, although local authority CMBs above £1m not yet tested | Securing funding against the local authority credit rating, unlike PWLB this may require a credit rating. |

Extensive board and council member approval process for projects. Process that emulates the ease of use of PWLB |

As for PWLB Examples include West Berkshire and Swindon Councils.

|

| Salix | Interest free loan | 100% no-maximum loan value but amount dependent upon payback period | Lending against the local authority | Compliance tool and business case to assist in application. Responsibility and competence requirements placed on local authority. |

As for PWLB Assurance/audit process post project delivery |

| UKIB | Gilts + 60bps, at around 2.6% at April 2022. | Project specific | Secured against the covenant of the local authority | Project specific | There will be a requirement for benefits recognition and reporting and potentially for compliance with PPN6/21# |

The UKIB, UKMBA, PWLB, CMBs and Salix all have a strong role to play in the financing of councils’ green projects. Private sector green finance outside of these avenues is generally more expensive and more restrictive than these instruments in the current state. Unless there are significant market developments it is unlikely that private sector debt will be an attractive alternative for most public sector projects outside of the routes discussed without further aggregation of project pipelines.

1.6 Conclusions

Green finance is ultimately about the funding of sustainable projects, regardless of the source of the finance. It is important that, whatever the source of finance, local authority green projects are able to provide transparent and reliable verification of the non-financial benefits and have an understanding of how they can manage carbon emissions during their delivery stages.

Councils are well placed to access cheap debt finance, both through PWLB, the UKIB, the UKBMA and through the emerging CMB market (see West Berkshire Council example in section 5.4). Financial terms for PWLB and CMBs are likely to be similar going forward, with CMBs providing the opportunity to connect local people to projects in their area but are unlikely to raise all the funding necessary for larger projects. CMBs and PWLB can be blended to support projects where both local connection and larger funding packages are required. The cheapest source of potential funding will be either through the UKMBA or the UKIB, but this is only for larger projects needing to borrow £ 5 million or more.

Other than where partnership working with the private sector is envisaged, there is rarely a need for councils to engage with the more complex and expensive private sector green finance.

The Government has a range of support mechanisms in place including grants and price support mechanisms to some sectors. It is possible that this will be supplemented during the course of the current Government’s term of office.

1.7 Recommendations

Councils looking to invest in green projects should consider the following.

- Can the project demonstrate it primarily supports the function of the local authority?

- How will the project’s sustainable benefits be measured and verified?

- Is there a source of grant funding available for the project? It should be noted that these change from time to time, so it is important to keep up to date.

- Recent grant funding for energy efficiency projects may be repeated in subsequent years. In order to access funds, it may be necessary to move quickly, so preparing schemes in advance is an advantage when looking to secure grants, if grants are not available this will also assist in seeking alternative means of funding. Councils should also consider using existing energy performance framework agreements to ensure speed of delivery, certainty of benefits and compliance with procurement law.

- Access to alternative routes for funding have an administrative burden (for example enhanced levels of project specific due diligence) which need to be considered as part of the funding decision.

- Councils have access to both grant funding and cheap finance, providing a competitive advantage over the private sector where there is competition for assets (such as in the purchase of renewable energy generation capacity).

- Where councils are offering finance into joint venture projects or to utilise their land assets to leverage projects the implications of state aid and more complex procurement need to be fully factored in alongside the potential benefits of new sources of capital and expertise.

Introduction to green finance

Over the last few years around 75 per cent of councils have declared a climate emergency, with many of these also committing to becoming net-zero emitters of greenhouse gases. Meeting these commitments will require both significant investment into low-carbon infrastructure and the decarbonisation of heat. Even if global greenhouse gas emissions are contained to 2C above pre-industrial levels, the UK will experience a significant increase in temperature, more frequent extreme weather events and rising sea levels. Measures to adapt to a warmer climate will be far reaching and will require significant investment.

In publishing a GFS, the Government has recognised the need for a comprehensive approach to greening financial systems, mobilising finance for clean and resilient growth, and capturing the resulting opportunities for UK firms. The challenge for both the local government sector and the providers of that finance is in finding appropriate mechanisms that provide competitively priced funds and programmes of sufficient scale and resilience to attract them.

Meanwhile the measures taken by councils in support of the response to the COVID-19 pandemic have strained local authority budgets. Green finance will be a key focus of both the recovery and renewal programmes for many councils following the COVID-19 pandemic, and to the future deployment of green infrastructure projects.

From a recent survey of members, the LGA has established that councils face a range of challenges to enacting climate change action. Securing the required resources and staff capacity, including overall funding needs, short-term funding cycles, and lack of clarity on goals or instructions for implementing successful climate change related projects.

LGA Member survey key findings

- Over four fifths of respondents stated that the limited amount of available funding was a barrier to their authority tackling climate change to a great extent, and no respondents said that amount of funding was not a barrier at all.

- 49 per cent of respondents said Short-term funding necessitates 12-month contracts.

Barriers to tackling climate change

Respondents were asked the extent to which a variety of factors were a barrier to their authority tackling climate change and found the most frequently reported barriers were amount of funding (97 per cent to a great or moderate extent), accessibility of funding (94 per cent lack of workforce capacity (92 per cent), internal skills and expertise (77 per cent), conditions of funding (87 per cent), and reliability of funding (74 per cent).

Whilst funding appears to be a barrier to the delivery of green ambition, it is the need for long term cheap finance that is prepared to engage in a wide range of projects with long term and variable returns that is needed.

This guidance has been produced to provide practical advice on how councils can access and utilise green finance to meet economic recovery goals and climate emergency ambitions, drawing on examples both from the United Kingdom and international case studies. In authoring this guidance our focus has been on the mobilisation of green projects and we have therefore looked at wider financial measures as well as the various forms of green debt finance available. We have considered both the projects a local authority might directly fund, but also those it may wish to support or stimulate within its geographic area.

2.1 What is green finance?

Green finance refers to the financing of new and existing public and private investments with sustainability objectives. Sustainability objectives include renewable energy and zero carbon energy generation and distribution, energy conservation measures, climate adaptation works, migration of activities away from fossil fuel sources, conservation and sustainable agriculture. Green finance can take many different forms, including green bonds, green loans, a green revolving credit facility, green hire purchase, green lease and asset loans, green grants and mechanisms to create market certainty.

Green financial instruments are very similar to traditional brown finance in that they are defined more by the specific purposes that they can be used for, rather than by any differences in how they operate. The key distinction for green finance is how it can be demonstrated that the investment is producing the environmental benefits it set out to deliver and some products may have penalties linked to failure to verify such. Green finance may also have more stringent requirements attached relating to the decarbonisation activities and ambitions of suppliers responsible for project delivery.

Chapters 4 and 5 of this guidance set out a brief description of green finance options that are available to councils. It is possible to use traditional ‘brown’ finance for green projects and in particular councils should be mindful of specific requirements to audit or certify green benefits or any penalties that apply in the event that this is not achieved.

2.2 UK Government GFS

On 2 July 2019, HM Treasury and the Department for Business, Energy and Industrial Strategy (BEIS) published the GFS, which establishes the Government’s direction on financial markets intervention against the backdrop of the UK’s statutory commitment to reduce greenhouse gas emissions to net-zero by 2050. The GFS has two key objectives:

- to align private sector financial flows with clean environmentally sustainable and resilient growth, supported by Government action

- to strengthen the competitiveness of the UK financial sector.

There are three strategic pillars to the strategy to support these objectives:

- Greening finance – which centres on ensuring climate and environmental factors are integrated into mainstream financial decision making.

- Financing green – where the focus is on accelerating finance for clean and resilient growth and improving access to finance for green investment.

- Capturing the opportunity – which aims to cement the UK’s position as a global leader for green finance and ensure the UK is at the forefront of green financial innovation, data and analytics.

Of interest to councils is the financing green strand of the strategy which seeks to mobilise and accelerate private capital flows into clean growth and environmental sectors to support the delivery of the UK’s carbon targets. The Government recognises that public sector funding alone will not be sufficient to deliver the transition to environmentally sustainable growth, and as such is focused on mobilising private finance and removing associated market barriers. It is anticipated that this strategy will be updated during 2022.

2.3 Role of institutional investment

A lot of attention is placed on the role and influence that institutional investors can have in delivery of a GFS, largely due to the scale of funds at their disposal. The latest data from the Office of National Statistics indicates that the total assets held by insurance companies, pensions funds and trusts in the UK is approaching £5 trillion. Within that, from a local government perspective, the 88 funds that make up the Local Government Pension Scheme had assets approaching £340bn as at the end of March 2021.

These investors have a primary responsibility to their clients and members in terms of being able to generate growth and returns that can meet their obligations as they fall due. Inevitably, this has meant and continues to mean holding investments in businesses reliant upon fossil fuels, ranging from multinational oil and gas companies to firms involved in carbon intensive manufacturing.

However, institutional investment is seeking to reduce its exposure to carbon as a result of the policy and legislative shifts of governments in response to climate change, the demands of their clients whose funds they are holding and the corporate recognition of their fiduciary duty to be a responsible investor. This is manifesting itself in a number of ways such as using influence as shareholders to ensure de-carbonisation plans are delivered and increasing investments in renewable energy initiatives. If this is to become a long term sources of direct finance to publicly sponsored green project delivery then there will need to be better means of aggregation for project pipelines to develop the scale necessary to deliver affordable finance.

In January 2021, the All-Party Parliamentary Group for Local Authority Pension Funds launched an inquiry into the role pension funds can play in helping the economy transition to a net zero position in a way that is fair and just. This is considered to involve balancing both the environmental and social considerations including, for example, the impact on workers and places who rely on carbon intensive industries.

From a finance perspective, the report recommended that funds need to give due weight to ‘just’ transition risks in their capital allocation and that policy statements should be used to guide investment decisions, including those of fund managers.

How such funds allocate capital and the type of investments they make will vary according to yield requirements. The principles set out in the next section of this guide equally apply to institutional finance whether that is provided on a debt or equity basis. Examples include purchasing portfolios of operational assets; partnership ventures involved in earlier stage project development and indirect investment through specialist infrastructure funds.

Underlying principles

Finance is fundamentally a combination of equity and debt, i.e. money you own and money you borrow.

3.1 Risk and finance

There is a direct relationship between risk and the cost and availability of debt finance, this applies to green finance as it does to any other form of finance.

The more that risks can be reduced, the lower the rate of interest that will apply and the easier it will be to obtain debt finance. The blend between equity and debt is usually driven by a combination of the risks associated with the project and the covenant strength of the borrowing party. The higher the risk the greater the proportion of equity likely to be required.

Some projects may not be fundable for debt and equity as the associated risks are deemed to be too high. The examples below set out why this might occur and various instruments that have been employed by the Government to avoid market failure.

- An initiative is new or emerging and there is not a tried and tested delivery model. An example of this would be the introduction of wireless charging for electric taxis where the Office for Zero Emission Vehicles (OZEV) intervened to provide some grant funding for a pilot project to prove the concept and support more widespread rollout.

- Financial returns are insufficiently certain. An example of this would be large scale renewable energy generation where the Government has put in place the Contracts for Difference (CfD) mechanism to provide price certainty (without providing subsidy).

- The market is not sufficiently developed or there is no guaranteed route to market. An example of this would be small scale renewable energy generation where the Government has put in place the Smart Export Guarantee (SEG) scheme. This provides a guaranteed route to market for small scale renewable energy projects, without providing either price certainty or subsidy.

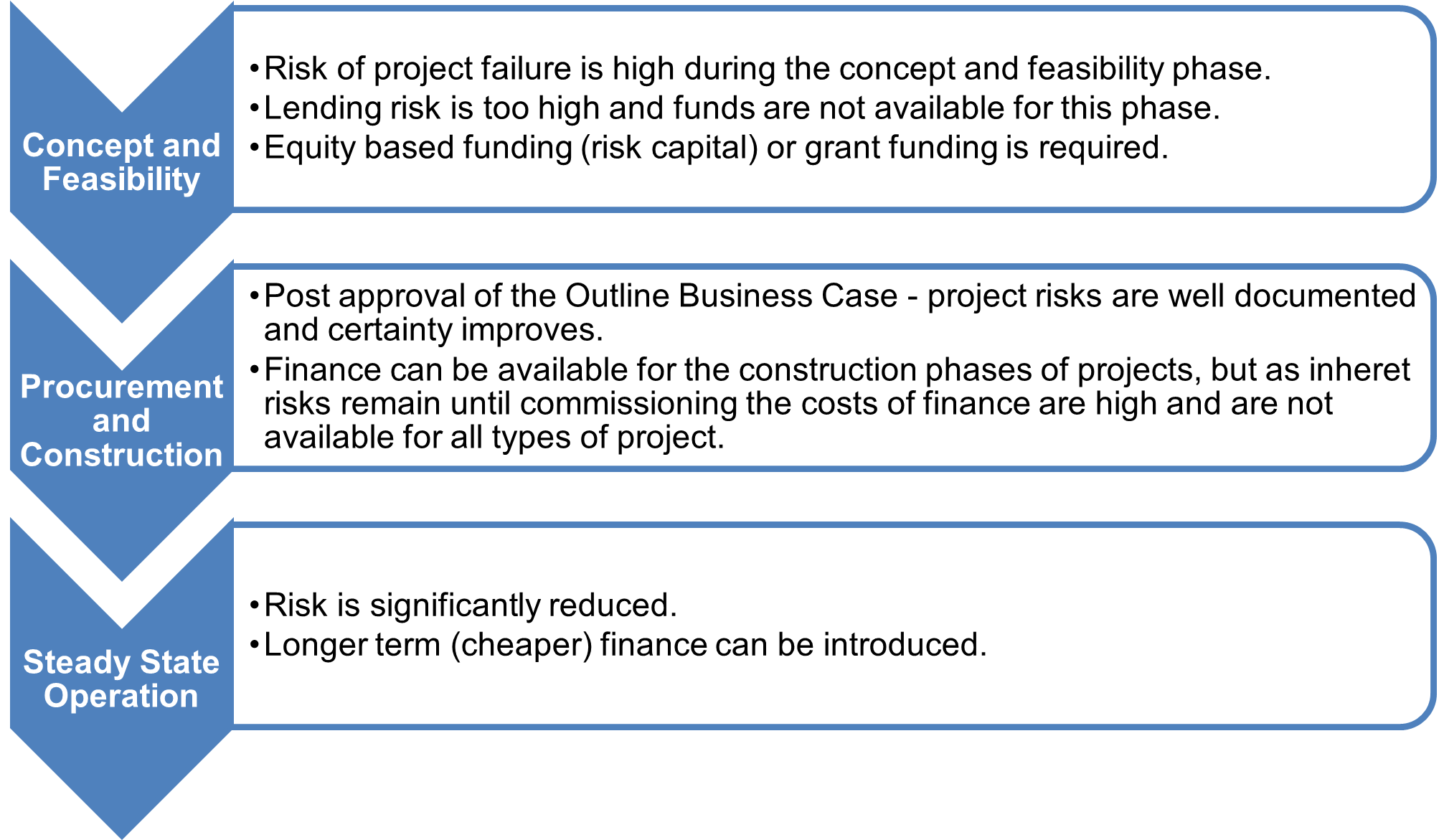

3.2 Evolution of project risks

Total risks within a project reduce and evolve as it progresses from concept through feasibility to procurement and construction and onto steady state operation. Different types of finance will be applicable to different stages of the project. The cost of finance; and the terms of finance can be subject to change at each phase. It is common to change the finance in commercial projects once they become operational. An example of this is the refinancing of PFI projects. Figure 1 shows this in more detail.

All private sector finance will follow these principles, however some public sector finance, such as the PWLB is based on the statutory status and strength of the local authority, as opposed to the risks associated with any particular project or programme.

An understanding of private sector financing mechanisms is important where the local authority is acting as a partner or guarantor in a scheme. Where this is the case, the local authority should check carefully whether such arrangement is permissible under subsidy control regulations.

3.3 Transaction structures

A local authority may need to consider potential transaction structures for a number of reasons. These are likely to include:

- the need or desire to put a project at arm’s length to the local authority by virtue of it involving commercial trading activity

- the local authority working in partnership (either formal or by other arrangement) with external parties – which may be public or private sector

- the local authority extending support to a third-party scheme through the inclusion of assets, finance or funding.

Aside from specific requirements of individual parties to a project, the overall transaction structures are largely shaped by risk and tax factors and will need to be considered on a project specific basis.

In partnership projects, the local authority with its access to capital finance can decide on what funding role it wishes to play at each stage, dependent on the risks and opportunities. If the project involves partners alongside the local authority, then limited liability partnerships have become the favoured vehicle because of their tax transparency with each party’s share of profit being assessed for tax as part of their respective corporation tax position. For councils, it means their share of profit is not reduced for tax as they are not liable for corporation tax.

3.4 Differences between public and private sector financing

Private sector financing

Typically, private sector financing will be a combination of debt and equity, with the debt being layered according to the level of risk as follows:

- Senior debt – up to around 80 per cent of a steady state project may be fundable through senior debt. Interest rates are lower reflecting the security that it has in the event of project failure and payment default.

- Junior debt (sometimes referred to as mezzanine finance). This can be used to reduce the amount of equity required to fund a steady state project. Junior debt has a second call on resources in the event of project failure (behind the senior debt) and the interest rate is higher to reflect the higher level of risk.

- Construction finance – private sector finance during a construction phase is generally significantly more expensive than either senior or junior debt. Typically interest rates are four or five times higher to reflect the greater project risk prior to completion and commissioning.

- Project development finance – this is specialist and often not available in isolation, it is more often found when accompanied by a project development service. Where development finance is available, the interest charged is generally very high and based around a share of the overall value of the asset created. The risk profile for project development finance is similar to that of equity.

- Equity – almost all projects will require a degree of equity funding. As the project progresses through the development phases and certainty increases, the proportion of equity required falls from 100 per cent initially to as low as 5 per cent on some heavily geared projects. Equity always takes the highest level of risk and consequently expects the highest rate of financial return.

Private sector funding is generally project specific and looks to secure lending against the project assets. It is common for private sector projects to refinance once they have achieved steady state. This enables senior debt to be drawn in and equity released for other projects. The ratio of debt to equity is known as gearing and can produce significantly higher returns for the retained equity investment.

For example, if a £10m investment produces an overall return of 8 per cent then an equity investor would receive an annual return of £800,000. If however, the project was geared at 80 per cent with debt funding borrowed at 4 per cent interest then the equity investor’s cash investment would be reduced to £2m and the annual return would be £480,000 after paying interest – representing a return of around 24 per cent on the retained equity investment whilst also releasing £8m to invest in new projects.

Public Sector debt funding

Typically, councils take a different approach to borrowing and will use their overall standing and covenant strength to borrow and fund a programme of activity. The borrowing is secured against the authority rather than against specific projects.

This approach usually provides cheaper overall finance with fewer hurdles to draw down funding than private sector alternatives. Long term interest rates available to councils are similar to senior debt finance rates.

The relatively low interest rates and ease of securing the lending mean that there need to be specific reasons why a local authority project would want to consider private sector debt funding.

3.5 Measurement and verification

A key feature of green finance is the need to be able to verify to project stakeholders that the project has produced the environmental benefits set out in its original business case.

The measurement and verification process can take a number of forms, but all should be clear, transparent and auditable. For some schemes there are national or international accreditations that would be a key part of demonstrating environmental benefit.

Recognised verification standards

Recognised verification standards vary from time to time and it is important to check at the point of committing to a project what the current standards for that type of project are. Recognised schemes provide some form of auditable and widely accepted methodology to provide a high degree of confidence to investors and customers that the scheme delivers the green benefits it promises.

Some currently recognised verification standards in the UK which would be applicable to green finance include:

- Renewable Energy Generation of Origin (REGO) certificates. REGOs are provided by the Office of Gas and Electricity Markets (OFGEM) and provide certainty that electricity has been generated from renewable sources. These are useful for the generator in relation to verification, they can become more problematic for a consumer as the scheme allows the REGOs to be traded independently of the electricity units supplied.

- The Woodland Carbon Code (WCC) is the UK’s voluntary carbon standard for woodland creation projects. It provides reassurance about the carbon savings that woodland projects may realistically achieve through the issue of Woodland Carbon Units (WCU). WCUs can also be sold as part of an offsetting scheme to generate additional income.

- National Cycle Network accreditation through Sustrans.

Other forms of verification

Where there is no accredited verification scheme there are often still clear and straightforward means of verification. Examples would include:

- Changes in units of fuel consumed (e.g. kWh of electricity, or litres of diesel). This would need a baseline to work from and ongoing measurement and verification post implementation. Integrating Measurement and Verification into an Energy Performance Contract (EPC) brings standardisation and transparency, and certainty to the project outcome. It is increasingly recognised as a way of boosting stakeholder confidence in energy efficiency projects, particularly where services are funded through the financial value of the savings achieved. For example the Re:fit Framework (see section 5.8.2) suggests the use of International Performance Measurement and Verification Protocol to verify the savings achieved by Energy Services Companies.

- Changes to waste and recycling rates in an area measured in tonnes collected.

Verification can be bespoke to a project – but needs to be specific, measurable, achievable, realistic and timely and aligned to the original purpose of the project. Verification reporting should always be public.

Equity

4.1 Forms of equity

Reserves are the most commonly cited form of equity for councils, together with capital assets. Grant funding can also be considered as a source of equity for some projects.

Grant funding has some of the characteristics of green debt, especially in relation to the measurement and verification of outcomes. In pure finance terms it may not require security over the project assets or other financial recourse in the event of project failure and no interest payments are due. Grants often have a ‘clawback’ clause which recovers grant funding in the event that the project or scheme is discontinued or deviates from its original purpose to the extent that it would be unable to deliver the benefits originally envisaged. The clawback is similar to the financial recourse provisions of debt funding but applied in more specific circumstances. The interaction between any recourse and clawback provisions on a project need to be carefully thought through.

4.2 Equity and associated sources of funds

Definition and application

Equity represents ownership in a project and the level of ownership adopted by a local authority will be determined by a number of factors including the investment choices available. Conventionally, equity may be offered to raise funds but if the local authority holds the role of project originator, it would not need to share equity solely for those purposes given its ability to access capital. It may, however, wish to share equity as part of managing risk e.g. the local authority may seek a development partner with expertise and experience that it cannot source internally. Furthermore, it may need to share equity with partners by virtue of circumstance in order for the project to proceed e.g. for a renewable energy project the local authority may not own the land on which the project is sited or hold the grid connection offer. Our separate guidance (Renewable Energy Good Practice guidance for the LGA) discusses these issues in more detail.

Potential sources of equity

Local authority reserves are the main source of local authority equity for projects, although some authorities have also developed Section 106 planning policy (s106) which has allowed them to collect funds from developers for green projects and this is a further potential source of equity funding. Funds generated from this source will require spending within five years of collecting and must be used in compliance with the s106 policy.

It is possible that any future changes to the planning regime may impact the ability of councils to collect and direct s106 funding.

Other forms of equity contribution might include use of resources without recharge, or the contribution of land or other assets to a project. Where land assets are involved there will be a need to demonstrate that the project provides best value.

When grant funding is available this can supplement or replace a direct equity contribution.

4.3 Sources of grant funding

Post European Union (EU) Exit the Government is likely to be the source of most grant funding available to UK councils. The Government typically offers grant funding in one of the following situations:

- There is a need to prove concept and build investor confidence. This may be for research work or project pilots etc.

- There is a need to stimulate a particular section of the market, especially where there is market failure or market change is desirable, but not happening quickly enough.

- To provide economic stimulus through the direct procurement of goods or services, but where the Government is unable to procure them directly.

Where grants are provided this is generally for a specific period and they are then closed or withdrawn. Examples of green grants currently available are set out in the sections below. These are not exhaustive, and it is important that a local authority looks for current grant funding when developing a scheme. There have also been further funding announcements in the Ten Point Plan for a Green Industrial Revolution and whilst the specifics of how these funds can be accessed is not yet clear the following additional funding was identified:

- £200 million to create two carbon capture clusters.

- £500 million for hydrogen projects.

- £525 million for new large and smaller-scale nuclear plants.

- £1.3 billion for electric vehicle charging infrastructure.

- £582 million support for the purchase of ultra-low emission vehicles.

Heat networks

The Government is committed to achieving net-zero greenhouse gas emissions by 2050. Meeting this legal commitment will require virtually all heat in buildings to be decarbonised, and heat in industry to be reduced to close to zero carbon emissions. Presently, heat is responsible for a third of the UK’s greenhouse gas emissions. As such, heat networks are a crucial aspect of the path towards decarbonising heat. In the right circumstances, heat networks can reduce bills, support local regeneration and can be a cost-effective way of reducing carbon emissions from heating.

There is already a growing heat network market in the UK which is supported by Government commitment. This is through the Heat Network Investment Project (HNIP) of up to £320m and the work of the Heat Network Delivery Unit (HNDU), supporting councils and project developers in the early phases of scheme development.

Heat Networks Delivery Unit

The Heat Networks Delivery Unit (HNDU) was established as part of the Government’s decarbonisation strategy. The Unit provides funding and specialist guidance to councils who are developing heat network projects, supporting them through a number of project development stages. All councils in England and Wales can apply for support. Since its inception in 2013, HNDU has awarded support to over 250 schemes across over 150 councils in England and Wales, including £23m of grant funding.

HNDU grant funding can provide up to 67 per cent of the estimated eligible external costs of heat network development studies (where ‘eligible external costs’ means the money paid by the local authority to third parties to deliver the heat network development stages). The local authority will need to demonstrate in their application that it has secured at least 33 per cent in match funding. HNDU grant funding can also provide up to 100 per cent of the cost of estimated externally procured project management support.

Since its inception, HNDU has run 11 funding rounds. Round 11 closed on 31 December 2021. More information can be found on the HNDU guidance page on the .gov website.

Heat Networks Investment Project (HNIP)

In tandem with HNDU, the Government is investing up to £320m through HNIP to support the commercialisation and construction of heat networks across England and Wales. This provision is through capital grants and loans.

To date, HNIP has funded over £150m for over 30 projects across England. The HNIP delivery partner (Triple Point Heat Networks Investment) has a dedicated investor relations team that engages with the investor community and broadens the reach of heat networks investment by raising third party finance for projects applying to HNIP. For more information visit the HNIP overview and application page.

Green Heat Network Fund (GHNF) transition scheme

To capitalise on the progress made by HNIP, and to support the development of low and zero carbon heat networks the GHNF has been created. It is a capital grant open to public, private, and third sector applicants in England. The GHNF was launched in March 2022, with funding rounds taking place on a quarterly basis with award notifications anticipated two months after application. The timing of funding rounds and further information can be found in the Green Heat Network Fund guidance.

One Public Estate (OPE) – ninth round (now closed)

The OPE programme is an established national programme delivered in partnership between the Office of Government Property in the Cabinet Office, the LGA and the Department for Levelling Up, Housing and Communities (DLUHC). Their joint aim is to bring public sector bodies together, to create better places by using public assets more efficiently, creating service and financial benefits for partners and releasing land for housing and development.

The ninth round of funding placed particular emphasis on the Government’s commitment to level up. For more information and to keep on eye on future funding from OPE please visit One Public Estate and Land Release Fund prospectus.

Governments £1bn Public Sector Decarbonisation Scheme (PSDS)

BEIS launched the PSDS on 30 September 2020 delivered by Salix Finance. There have since been two further rounds of funding, totalling £3.175bn over the period to 2024/25. The scheme allocates grant funding for capital energy efficiency and heat decarbonisation projects within public sector non-domestic buildings including Government departments and arm’s length bodies in England with the aim of delivering the following objectives:

- deliver stimulus to the energy efficiency and heat decarbonisation sectors, supporting jobs

- deliver significant carbon savings within the public sector.

The purpose of the grant scheme is to help make eligible buildings more energy efficient and install low carbon heating measures, for example, insulation, glazing, heating controls, and heat pumps (eligible technologies are split into 4 different categories). The cost to save a tonne of carbon (CO2e) over the lifetime of the project must be no more than £500, which is automatically calculated by the support tool in the grant application form.

The scheme allows public sector bodies to apply for a grant to finance up to 100 per cent of the costs of capital energy-saving projects that meet the scheme criteria. For more information about the scheme and to monitor the potential for future phases please visit the Salix Finance website.

Local Partnerships and the Greater London Authority own and run the Re:fit 4 Framework which is a procurement initiative for public bodies wishing to implement energy efficiency measures and local energy generation projects on their assets (see section 4.8.2). Current Re:fit Framework users can use the opportunity to review existing project briefs and develop projects eligible for BEIS grant funding, particularly projects that were previously discounted (such as insulation and glazing) because of long pay back periods (25 years plus). Local Partnerships can also support councils’ preparation for grant applications in this respect.

These grants and the Green Homes Grants have been offered as part of a COVID-19 economic stimulus package. The 2019 Conservative Party manifesto committed to a larger sum of public funding for energy efficiency in buildings than has currently been announced (£9bn as opposed to the £4 billion announced to date). It is possible that further iterations of this funding may become available in future years.

Public Sector Low Carbon Skills Fund (now closed)

The Public Sector Low Carbon Skills Fund was available alongside the Public Sector Decarbonisation Scheme. It provided grants to help all eligible public sector bodies to source specialist and expert advice to identify and develop energy efficiency and low carbon heat upgrade projects for non-domestic buildings, before preparing robust and effective applications to the Public Sector Decarbonisation Scheme. Two rounds of funding have closed. If there are future rounds of the Public Sector Decarbonisation Scheme there may be future rounds of this fund which it is anticipated would be detailed on the Salix website.

Energy Company Obligation Flexible Eligibility (ECO FLEX) grants

Energy Company Obligation (ECO) is a Government energy efficiency scheme to help reduce carbon emissions and tackle fuel poverty. ECO 4 is a £1bn programme and is available from April 2022 to April 2023. The aim of the scheme is to install energy efficiency measures in properties that are currently energy inefficient which in turn reduce households’ fuel bills. ECO provides qualifying residents the opportunity for potential improvements such as a new central heating system, upgrades to the existing heating system and/or insulation measures.

The ECO scheme is only available through energy providers, it is not available to councils to deliver home energy efficiency improvements. However, under the ECO FLEX, councils are permitted to identify and designate households as eligible under the Affordable Warmth Scheme. £500m of the total budget for ECO 4 will be assigned to ECO FLEX.

To participate in the ECO FLEX scheme councils must publish a Fleixble Eligibility Statement of Intent which identifies an income threshold, cost or vulnerability criteria at a local level, ensuring that funding reaches those communities that are often least engaged with the energy market. Once households are identified, the declaration confirms the eligibility against the statement of intent’s criteria.

Further details of how to apply are available of the OFGEM website, and councils are encouraged to follow the guidance on the BEIS website

The Green Homes Grant – Local Authority Delivery (LAD)

The LAD scheme was launched in August 2020 and aims to raise the energy efficiency of low income and low energy performance homes with a focus on energy performance certificate ratings of E,F or G. It was delivered in phases, with phase 1A and 1B aiming for delivery of projects to be concluded by March 2022.

Phase 2 of the funding saw £300m funding allocated between the five Local Energy Hubs, to then be distributed to councils to deliver energy efficiency upgrades in low-income homes across England by the end of March 2022.

Local Partnerships was commissioned by BEIS via the five regional Energy Hubs to produce this Local Authority Housing Retrofit Handbook to provide practical advice to councils in England. It brings existing resources together in one place, and to find out what’s going on in your area, please visit your local net zero hub at the links below:

- North East & Yorkshire Net Zero Hub

- Local Energy North West Hub

- The Midland Energy Hub

- Greater South East Net Zero Hub

- South West Net Zero Hub

Tree planting

Current grants for tree planting include the Local Authority Treescapes Fund and the Urban Tree Challenge Fund, the Local Authority Treescapes Fund and the Urban Tree Challenge Fund.

Over £9 million will be allocated to successful applicants across these funds.

Local Authority Treescapes Fund

Now in its second round, successful applicants to the Local Authority Treescapes Fund will be allocated a share of £5.4 million for the planting of up to 650,000 trees in 2022/23. Projects will support councils to establish trees in different ways, from natural regeneration (where trees are left to naturally develop) to traditional planting. Community engagement is encouraged, and councils can bring together local residents, schools and environmental groups to restore trees in areas outside woodlands. These include riverbanks, parks, beside roads and footpaths, and within vacant community spaces – areas where treescapes are often highly degraded due to neglect or disease.

Trees make our towns and cities healthier and more pleasant places to be, helping to moderate temperatures, reduce pollution, decrease flood risk and improve people’s quality of life. If successful, applicants to the fourth round of the Urban Tree Challenge Fund will be awarded a share of more than £3.8 million – enough to fund the planting of over 28,000 large trees in both urban areas, and where rural and urban areas meet. This funding aims to grow the number of trees in and around deprived urban areas to bring people from all socio-economic backgrounds closer to nature.

There are several key differences between the Local Authority Treescapes Fund and the Urban Tree Challenge Fund. You can read a Forestry Commission blog outlining these differences and offering guidance on how to apply for both funds.

Applications for both funds are now open until 11:59pm on Tuesday 31 May 2022.

For more information and to apply, go to Local Authority Treescapes Fund and the Urban Tree Challenge Fund pages on the gov.uk website.

The Forestry Commission will open a new Tree Production Capital Grant this spring. The Tree Production Capital Grant will provide funding to increase the domestic production of tree seed and saplings, supporting investments in expansion, automation and mechanisation of facilities and equipment. This will help improve not only the quantity but also the quality, diversity and biosecurity of supply.

Applicants will be able to apply for up to 50 per cent of the costs for capital projects and equipment such as: intelligent transplanting systems; polytunnel infrastructure and equipment; irrigation systems and infrastructure; seed trays; grading machines; biosecurity investments such as water treatment and refrigeration equipment.

The grant will enable suppliers to bolster production at pace and has been designed to complement the innovation outputs of the Tree Production Innovation Fund, which provides support for research projects that will enhance UK tree production methods.

To be eligible for funding, applicants must be UK-based and will need to demonstrate how the grant will be used to increase English tree seed or sapling supply.

To receive the latest news on the grant, sign up to the Forestry Commission’s e-alert. For more information, please contact [email protected] or read the Forestry Commission’s latest blog on the Tree Production Capital Grant.

Woodland creation funding and grants

There are various sources of funding available for woodland creation in the UK, which are summarised below. Further information can also be found in the leaflet on responding to the climate emergency with new trees and woodlands.

Woodland Creation Planning Grant (WCPG)

The WCPG provides funding to help cover the costs of producing a UK Forestry Standard compliant woodland creation design plan, which can support applications to other funding sources for woodland creation, such as the Woodland Carbon Fund (see below).

This grant contributes to the costs of gathering and analysing information needed to make sure that any proposal for productive multi-purpose woodland (over 10 hectares) considers impacts on biodiversity, landscape, water, the historic environment and local stakeholders. The grant scheme operates in two stages, which in total will provide £150 per hectare, up to £30,000 per project.

Woodland Carbon Code (WCC)

The WCC is the national standard for verifying and validating carbon savings from afforestation projects in the UK. Accredited schemes have the opportunity to sell ‘carbon credits’ which represent CO2 savings generated by the new woodland. This can provide an additional source of revenue if, for example, a project is not cost-effective with Woodland Carbon Funding WCF funding.

Woodland Carbon Guarantee

In November 2019 the Government announced a new £50 million scheme, the Woodland Carbon Guarantee, aimed at promoting afforestation, whereby the Government would agree to purchase WCC carbon credits from a participant at an agreed price set by auction. Instead of a grant or loan towards the cost of woodland creation or maintenance, this scheme offers WCC participants a guaranteed income over a 35-year period, although they may choose instead to sell carbon credits on the open market.

The next WCG auction will take place in 2022. The date will be published on the WCG webpage. In order to apply you must first register your project with the Woodland Carbon Code.

England Woodland Creation Offer

The England Woodland Creation Offer (EWCO) provides landowners, land managers and public bodies the opportunity for support to create new woodland, with possibility of receiving over £10,000 per hectare. For more information view the Woodland Creation's leaflet.

Green vehicle related funding

The Government offers grants to support the wider use of electric and hybrid vehicles via the Office of Zero Emission Vehicles (OZEV). The total funding committed to support the transition to zero emission vehicles is £3.5 billion. £620m has been targeted for electric vehicle grants and infrastructure, with a focus on local on-street residential charge points.

The Government’s new UK Electric vehicle infrastructure strategy was published in March 2022, confirming £1.6 billion of public funding for charging points. £450m of this will be used to create a Local Electric Vehicle Infrastructure Fund (LEVI), under which councils will be able access funding to install charging hubs and on-street charging points. A £10m pilot scheme has been launched for the fund and is anticipated to fund between three and eight projects. Councils and partnerships in England can apply for funding under the pilot scheme. To apply you must send an expression of interest email to Energy Saving Trust with the email subject LEVI expression of interest and the completed application must be submitted by 11:55pm, 17 June 2022.

For more information on the LEVI, its eligibility criteria, and details on how to apply visit the LEVI guidance page.

The pilot fund is complementary to the existing On-Street Residential Chargepoint Scheme (ORCS). whereby councils can apply for funding to help with the costs of procurement and installation of on-street charging points for residential use. Councils are able to receive a grant to part fund (75 per cent) of the capital costs. OZEV will provide up to £6,500 per chargepoint installation, and each project should not exceed more than £100,000 in OZEV funding. More information can be found here.

The Workplace Charging Scheme is a voucher-based scheme that provides support towards the up-front costs of the purchase and installation of electric vehicle charge-points, for eligible businesses, charities and public sector organisations. You can apply by completing the Workplace Charging Scheme application form.

The Department for Environment Food and Rural Affairs (DEFRA) Air Quality Grant Programme provides funding to eligible councils to help improve air quality. It is focused on air quality issues (such as NOx and particulates) and supports a wide range of initiatives such as establishing low emissions zones, retrofitting fleets with low emission technologies and traffic measures. It has also funded electric vehicle chargepoint infrastructure.

Active travel and cycles lanes

In July 2021 a £338 million package to boost cycling and walking across the country was announced. The package includes funding to build hundreds of miles of high-quality cycle lanes and is part of the government’s commitment to build back greener from the pandemic.

Local transport authorities outside of London were given funding through the Capability Fund.

Additional sources of green funding, which flow from the Government’s 2018 Clean Air Strategy, are as follows:

- The Bus Services Act 2017, which includes a range of measures to improve bus services through franchising and better partnership working. Councils and bus operators are encouraged to agree a package of improvements to introduce bus priority measures to reduce idling and journey times, or to introduce Ultra Low Emission Vehicles along key routes.

- In March 2021 up to £120m was made available through the Zero Emissions Buses Regional Area scheme to help local transport authorities, outside of London, introduce zero-emission buses. Applications are no longer being accepted, but a further £150m was made available in the October 2021 spending review, to support the scheme, taking the total funding to £270m in the financial year 2021 to 2022.

- The National bus strategy, “Bus back better” was published in March 2021, guidance to councils and bus operators can be found here.

- The Cycling and Walking Investment Strategy published in 2017 identifies £1.2bn of funding to be invested in cycling and walking from 2016 to 2021. This has already included £101m made available through the Cycle City Ambition programme to improve cycling infrastructure in eight cities, and £80m to support local projects to improve safety and encourage cycling.

Shared Prosperity Fund

The Government has announced a UK Shared Prosperity Fund (UKSPF) in the 2021 Spending Review the fund is worth £2.6 billion over the period to 2024-25. Further details can be found on the UKSPF website.

The national planning system and greenspace mapping are examples of further programmes which benefit cycling and walking infrastructure and will directly result in increases to cycling and walking activity. The Healthy New Towns programme, supported by NHS England and Public Health England, was launched on 1 July 2015.

The Community Infrastructure Levy and s106 contributions allow councils in England and Wales to raise funds from developers undertaking new building protects in their area in order to help provide vital infrastructure, based on local priorities. These funds can be used to for a wide range of infrastructure, including transport, parks and green spaces, cultural and sports facilities, provided the scheme has sufficient resources and the local authority has compliant policy in place to enable funds to be collected for the purpose.

The Cycle to Work Scheme is a tax-efficient, salary-sacrifice employee benefit, introduced in the 1999 Finance Act, which provides a way of encouraging more adults to take up cycling. Employers are able to loan cycles and safety equipment to employees up to the value of £1,000. At the end of the loan, an employer can offer the cycle for sale to the employee, but at the full market value. Electric vehicle salary sacrifice schemes also exist which enable an employee pay for an electric car each month using their gross salary. It’s the same as other salary sacrifice schemes, such as childcare, cycle to work schemes or pension contributions.

Flood defence

Lead local flood authorities (unitary authorities or county councils) have the lead operational role in managing the risk of flooding from surface water and groundwater. In areas with no district council, they also have the lead role in managing flood risk from ‘ordinary watercourses’, for example any watercourse that isn’t a main river.

A flood risk management authority can apply for grant-in-aid (GiA) to fund Flood and Coastal Erosion Risk Management (FCERM) projects. A highway authority or water authority can only apply for a GiA for projects to reduce flood risk which are outside its normal area of responsibility. More information can be found tn the FCERM guidance. Further details on funding arrangements can be found on the LGA’s flooding funding arrangements webpage.

Peat/habitats improvements

The UK Peatland Strategy identifies a target for two million hectares of peatland to be in good condition, under restoration, or sustainably managed by 2040. In the March 2020 budget, the Government announced a £640m Nature for Climate Fund to plant more than 40 million trees and restore 35,000 hectares of peatland in England.

The fund is to be used to dramatically increase the rates of tree-planting in England along with funding more research into the most appropriate species to plant across the country, a scaling up of the nursery sector to grow saplings, establishing new partnerships with landowners, and increased planting rates on sites. As part of the budget the Government also announced a Nature Recovery Network Fund of £25m to support habitats and species action in nature recovery areas.

4.4 Other significant government funding sources

Whilst not specifically ‘green funding’ it is anticipated that successful bids to national schemes such as the Shared Prosperity Fund and the Levelling Up Fund will need to demonstrate their green credentials.

Debt

5.1 Forms of debt

Debt funding comes in many forms and from a wide range of providers. However, it can be split into forms which are secured against a particular asset and forms which are secured against the activities of the local authority.

Securing funding (usually either PWLB, a municipal bond or a CMB) against the local authority reduces the level of overall lending risk and therefore provides access to lower rates of interest.

There are further market interventions which can be used to reduce risk and therefore reduce interest rates and increase the availability of debt. These generally take the form of providing surety for a debt or guaranteeing the availability and value of income streams.

Councils are able to access debt in a variety of different forms. The selection of one form of debt over another will be specific to both the local authority and the project.

5.2 PWLB

The PWLB is one of the main lenders to councils and accounts for around two thirds of local authority debt. Since the introduction of prudential borrowing, the PWLB has normally offered the lowest rate of interest available to councils and is provided on a more flexible basis than most private sector funding. Lending is structured around the statutory provision of the local authority as opposed to specific projects. PWLB borrowing is automatically secured on the revenues of the local authority rather than by reference to specific project revenues, assets or collateral. This enables lower interest rates and entails significantly less external due diligence on individual projects than other forms of borrowing.

The Government published new lending terms for PWLB on 26 November 2020, primarily aimed at introducing proportionate and equitable ways to stop councils investing in commercial assets primarily for yield.

The new lending terms introduce specific requirements:

- Submission of a high-level description of capital spending and financing plans for the following three years, including their expected use of PWLB.

- The s151 officer to confirm that there is no intention to buy investment assets primarily for yield during the next three years as part of that submission and when applying for a new loan.

- Lending to be for the purposes of service delivery, housing, regeneration or preventative action. The Government has issued guidance rather than developing strict definitions in recognition of the complexity of the sector .

PWLB was used by Warrington Borough Council in the acquisition of two solar farms in Yorkshire as set out in case study below.

Case Study 1: Warrington Borough Council – PWLB

Carbon accounting practice does not allow councils to buy a green tariff electricity and claim the carbon benefits, instead the grid supplied intensity rate applies. If a council generates its own renewable electricity from a directly owned or identified source then it is possible to account for the carbon savings, provided additionality (i.e. new provision) can be demonstrated. Most councils are large users of electricity and in 2018 councils collectively spent over £863m with the big six energy companies. As energy is one of the largest controllable overheads in council buildings, many councils have looked at offsetting the retail cost of electricity and to generate income through energy generation. One such example is that of Warrington Borough Council which acquired two solar farms to sleeve the power back to themselves, and in doing so benefit from price certainly on their wholesale electricity costs.

The first, a hybrid solar farm consists of a 34.7MWp solar farm plus a 27MW battery storage facility. The project is located near York and completed construction in December 2019 by the Council’s contractor Gridserve. The second, a 25.7MWp solar farm in Hull was completed in spring 2020 (also by Gridserve). Both projects were developed subsidy free with electricity from the York solar farm being sold on the open market whilst the Hull site supplies all the Council’s own energy needs. The Council has put a contract in place with Gridserve to operate and maintain both projects over their lifetimes.

The Council funded this through a PWLB loan, with loan payments being supported by a Power Purchase Agreement (PPA) where the Council signed a long-term agreement to buy the electricity generated by the Hull solar park to power its own operations. This secured a revenue stream for the project to get financed, without the need for a Government subsidy, and guarantees zero carbon electricity is being used by the Council.

5.3 UKMBA

The UKMBA is publicly owned with its shareholders being the LGA and 56 councils. Councils have the power to issue bonds, an IOU that can be traded on the financial markets, but it is not currently a common activity due to the cost, time and fees involved relative to the cost and flexibility offered by the PWLB. The UKMBA provides councils with a clear and effective route to market, either for a single or a pooled bond. Bonds can provide cheaper finance than PWLB and interest rates are outside the direct control of Government.

Bonds are raised against the covenant strength of the local authority and for single bonds (i.e. one local authority) a credit rating will be required. For pooled bonds the UKMBA will undertake financial due diligence on the councils which will not result in a published credit rating. The UKMBA is able to issue certified Environmental, Social and Governance (ESG) bonds for compliant projects and has a published certified framework for these. ESG bonds attract a lower interest rate than standard bonds and provide finance which is potentially cheaper than PWLB.

The reporting requirements are relatively light touch and seek to rely on criteria the local authority have already developed to support their project reporting.

Bonds require a minimum size of £ 250m borrowing which can be either from a single local authority or a pool of councils. The UKMBA will broker any pooled arrangements. Projects can be refinanced through this route and a local authority is able to include both projects which have been completed within the last three years and projects which are being delivered over the next two years.

Bonds have the advantage of being able to forward fix an interest rate for up to two years, without the need to draw the funds immediately. This can provide significantly more funding cost certainty than PWLB.

Lending terms can be flexible between 10 and 45 years and whilst the UKMBA does not provide financial advice it will help councils decide which is the best option for their requirements.

5.4 UKIB

Background and mandate

The UKIB is a new Government-owned policy bank, focused on increasing infrastructure investment across the UK. It will partner with the private sector and local government to finance investments that deliver the net zero agenda and drive local economic growth. The UKIB will finance strategic and high value projects across the range of local authority bodies and will invest alongside the private sector, crowding-in private sector capital.

The UKIB is wholly owned and backed by HM Treasury, but will operate independently and has two core objectives:

- help tackle climate change, particularly meeting our net zero emissions target by 2050

- support regional and local economic growth through better connectivity, opportunities for new jobs and higher levels of productivity.

Investment criteria

The UKIB can lend to both private sector investors and local and mayoral authorities, where those high value investments align with its core purpose. Like any other bank it will review individual projects on their own merits and investment is not guaranteed just because a project aligns with core objectives.

The focus is on high value and complex projects which align with the following principles:

- the investment drives regional and local economic growth or supports tackling climate change

- the investment is infrastructure based and will prioritise projects in the sectors of clean energy, transport, digital, water and waste.

- the investment is intended to deliver a positive financial return, in line with the UKIB’s financial framework

- on the private lending side, the investment is also expected to crowd in significant private capital over time.

Green eligibility

Included in the UKIB’s mandate is that investments do no significant harm and as such, the UKIB will not invest in projects which involve fossil fuels, with limited exceptions around carbon capture and storage or carbon capture, usage and storage, or decommissioning of existing fossil fuel assets.

UKIB financing assessment will likely align with the criteria set out for public procurement under PPN6/21.

Lending capacity and support

When the UKIB was launched in June 2021 an initial £22bn of financial capacity was allocated by HM Treasury, consisting of:

- £4bn for local authority lending

- £8bn for private sector equity and debt

- £10bn of private sector loan guarantees.

An associated advisory service is available for those councils who would like to discuss potential types of project in more detail. The advisory service is still in its development phase, but it will be aimed at providing councils with practical support and guidance on structuring complex infrastructure projects.

Pricing and other criteria for lending to councils

Qualifying projects will need a ticket size (i.e. loan value) of at least £5m and there is currently no defined maximum size for projects or programmes. Lending will be priced at Gilt + 60bps, which is more competitive than PWLB. This should reflect an incentive to councils to push forward their de-carbonisation and growth agenda.

Loans will have attached sustainability monitoring criteria attached to ensure that the advertised benefits are realised over and above the requirements for PWLB lending. The resource requirements for this will need to be understood as part of the development of the financial case for the Outline Business Case for projects.

The financing can be used in conjunction with other Government grant funding.

Future developments

UKIB is in its early development phase. It is formalising its first Strategic Plan and is scaling up in its capabilities and capacity. By March 2022, the UKIB had provided financial support to four projects.

The UKIB’s first Strategic Plan is expected in June 2022.

5.5 Community Municipal Bonds (CMB)

Crowdfunding is a process by which people provide money to projects, companies or organisations via a website or platform. Depending on the nature of the financial arrangement, people receive a return that is either financial (investment-based) or non-financial (donation-based).

A CMB structure is a new model of public sector crowdfunding, which offers the potential of providing low-cost capital for councils while also delivering socially and environmentally positive outcomes. This structuring provides councils with the ability to raise money more locally for green projects and provides a direct connection between their communities and new green infrastructure. Increasingly the rates and terms for community lending are close to those offered by PWLB.

West Berkshire Council was the first local authority in England to launch a Community Municipal Investment (CMI) bond (see case study below). More recently, in August 2020, Warrington Borough Council launched a CMI bond (via ethical investment platform Abundance Investment) to raise £1m to help finance the construction of a solar farm near Cirencester and its co-located battery storage facility (a 24MW hybrid project). The CMB has a five-year term and will pay investors 1.2 per cent per year, on a twice-yearly basis. The minimum investment was just £5. Warrington Borough Council is one of only a few UK councils to have a credit rating from Moody’s international rating agency. The CMB fund raise closed after reaching its £1m target, attracting over 500 investors from across the UK, with an average investment of almost £2,000 each.

Both the West Berkshire Council and Warrington Borough Council CMIs were issued by the council corporate body and administered by Abundance Investment, with resident and general public investors purchasing the bonds. Section 6 also includes a case study highlighting other Warrington Borough Council renewable energy investments.

Abundance Investment is particularly active in this sector and has indicated through research that CMIs have the potential to unlock a multi-billion market of retail investment money that could be directed into local authority funding via the Community Municipal Bond approach. Furthermore, the research outlined that investment-based crowdfunding had the potential to provide capital on terms which are similar to or better than the PWLB and through a process that emulates the ease of use of PWLB, while also offering the potential to deliver significant wider benefits to local communities. You can learn more by reading the Financing for Society report.

Case Study 2: West Berkshire Council – Community Municipal Bond

UK's first local authority green bond

West Berkshire Council has looked to tackle the climate emergency by investing in its first Community Municipal Investment (CMIs). The Council unanimously declared a climate emergency in July 2019 and approved an environment strategy to take action. The Council offered residents and community groups an opportunity to invest directly with them to help build a greener future for the district.

The Council was seeking to raise £1 million to fund new rooftop solar power on Council-owned buildings around West Berkshire and to help deliver its ambitious target of making the district carbon neutral by 2030. The sites included:

- a storage building at Greenham Common, an important open space for local people

- the Council’s headquarters at Market Street in Newbury

- the Phoenix Resource Centre in Newbury, which provides services for adults with learning disabilities, physical disabilities, frailty and dementia

- schools in Aldermaston and Burghfield Common

- the Willink Leisure Centre at Burghfield Common.

About the CMI

Individuals both in and outside of West Berkshire were able to invest from as little as £5 to support specific projects that align with the Council's declaration of a climate emergency. The investment is a CMI which is a UK first. A CMI is a bond or loan mechanism issued by a council directly to the public. The bond was issued in partnership with the online crowdfunding platform Abundance Investment, which is regulated by the Financial Conduct Authority. CMIs can be used to supplement, diversify or replace sources of borrowing to fund specific infrastructure projects, or to refinance existing debt.